1

arXiv Papers

1

Total Publications

Profile

Academic Profile

Metrics

Statistics

1

arXiv Papers

1

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

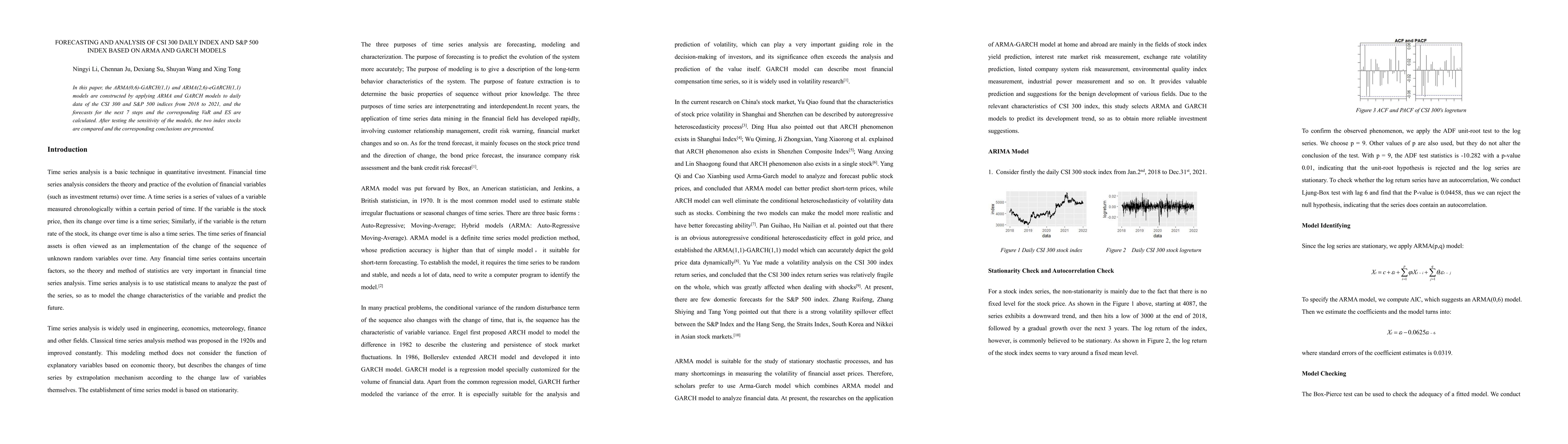

Forecasting and Analysis of CSI 300 Daily Index and S&P 500 Index Based

on ARMA and GARCH Models

In this paper, the ARMA(0,6)-GARCH(1,1) and ARMA(2,6)-eGARCH(1,1) models are constructed by applying ARMA and GARCH models to daily data of the CSI 300 and S&P 500 indices from 2018 to 2021, and the...