Academic Profile

Statistics

Similar Authors

Papers on arXiv

Semi-analytical pricing of American options in a time-dependent Ornstein-Uhlenbeck model was presented in [Carr, Itkin, 2020]. It was shown that to obtain these prices one needs to solve (numericall...

By expanding the Dirac delta function in terms of the eigenfunctions of the corresponding Sturm-Liouville problem, we construct some new (oscillating) integral transforms. These transforms are then ...

We extend the approach of Carr, Itkin and Muravey, 2021 for getting semi-analytical prices of barrier options for the time-dependent Heston model with time-dependent barriers by applying it to the s...

We continue a series of papers where prices of the barrier options written on the underlying, which dynamics follows some one factor stochastic model with time-dependent coefficients and the barrier...

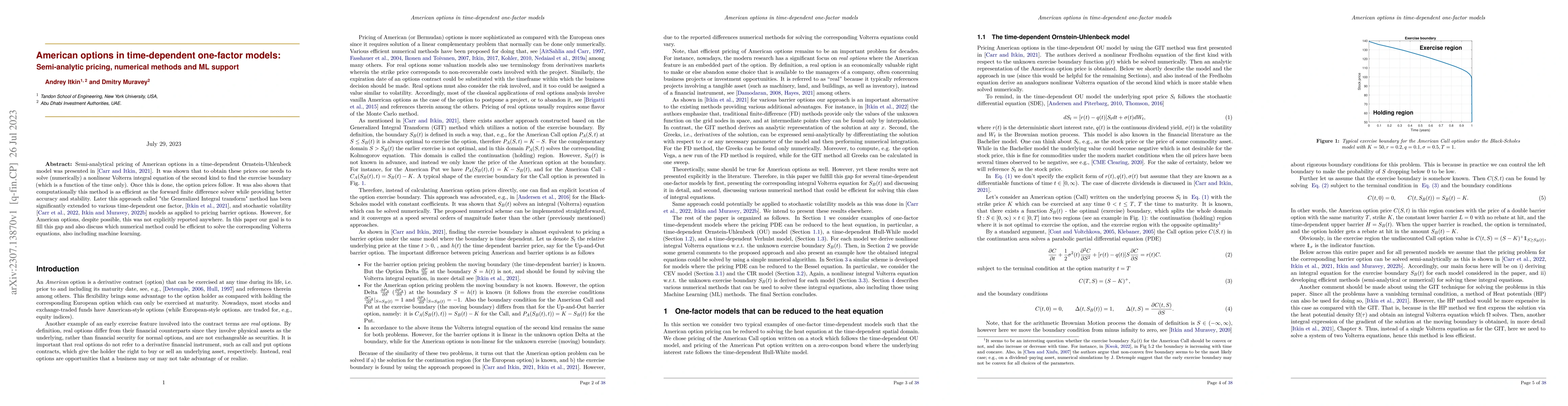

In this paper we derive semi-closed form prices of barrier (perhaps, time-dependent) options for the Hull-White model, ie., where the underlying follows a time-dependent OU process with a mean-rever...