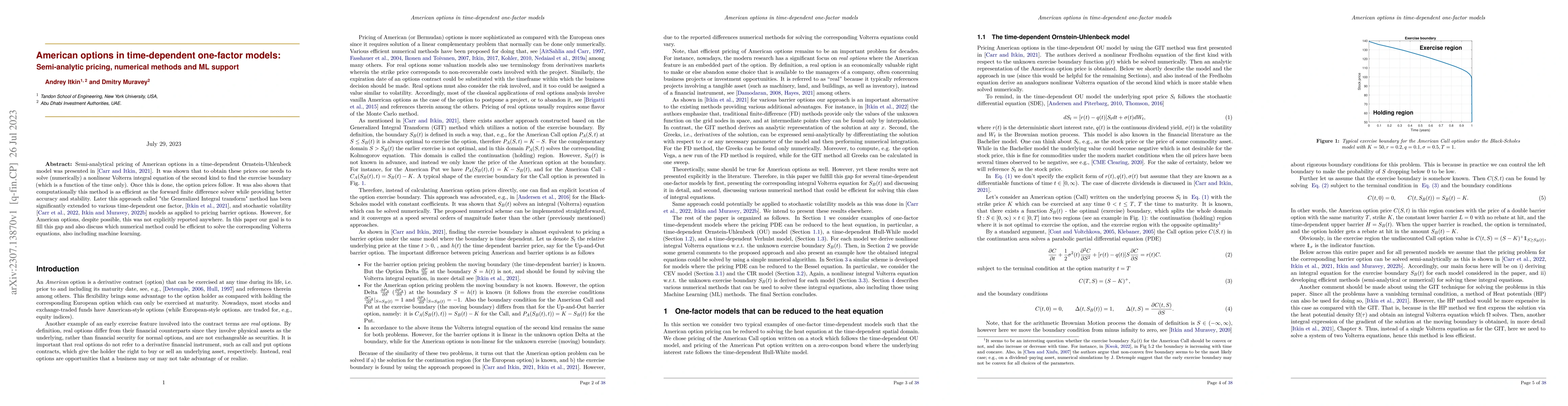

American options in time-dependent one-factor models: Semi-analytic pricing, numerical methods and ML support

Publication

Metrics

AI Quick Summary

This paper extends the semi-analytical pricing method for American options in time-dependent one-factor models, solving a nonlinear Volterra integral equation to determine the exercise boundary. It explores efficient numerical methods, including machine learning approaches, for solving these equations.

Paper Preview

Abstract

Semi-analytical pricing of American options in a time-dependent Ornstein-Uhlenbeck model was presented in [Carr, Itkin, 2020]. It was shown that to obtain these prices one needs to solve (numerically) a nonlinear Volterra integral equation of the second kind to find the exercise boundary (which is a function of the time only). Once this is done, the option prices follow. It was also shown that computationally this method is as efficient as the forward finite difference solver while providing better accuracy and stability. Later this approach called "the Generalized Integral transform" method has been significantly extended by the authors (also, in cooperation with Peter Carr and Alex Lipton) to various time-dependent one factor, and stochastic volatility models as applied to pricing barrier options. However, for American options, despite possible, this was not explicitly reported anywhere. In this paper our goal is to fill this gap and also discuss which numerical method (including those in machine learning) could be efficient to solve the corresponding Volterra integral equations.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0