Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper similar to [P. Carr, A. Itkin, 2019] we construct another Markovian approximation of the rough Heston-like volatility model - the ADO-Heston model. The characteristic function (CF) of ...

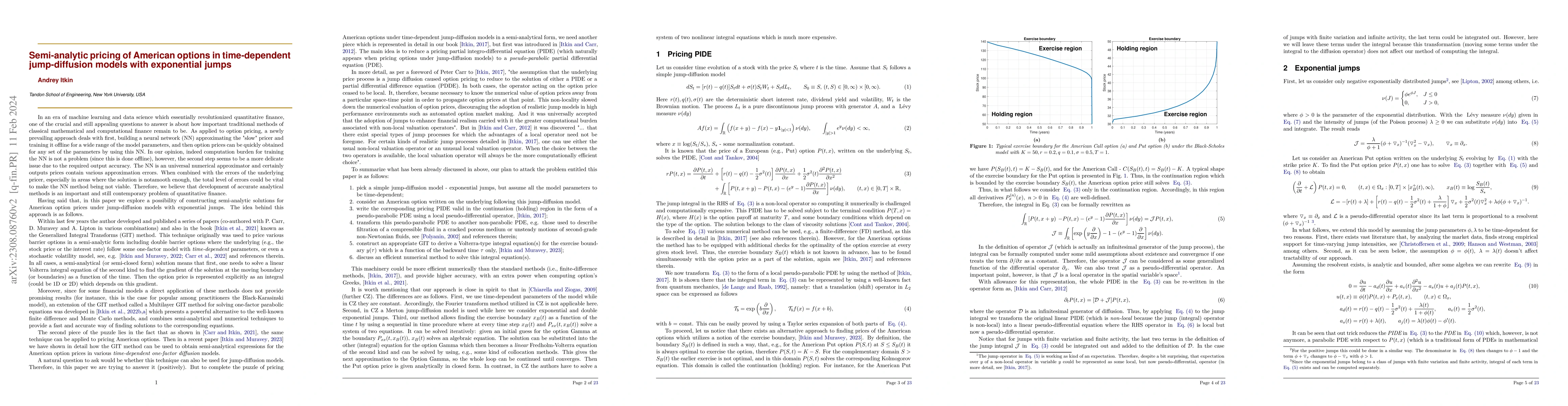

In this paper we propose a semi-analytic approach to pricing American options for time-dependent jump-diffusions models with exponential jumps The idea of the method is to further generalize our app...

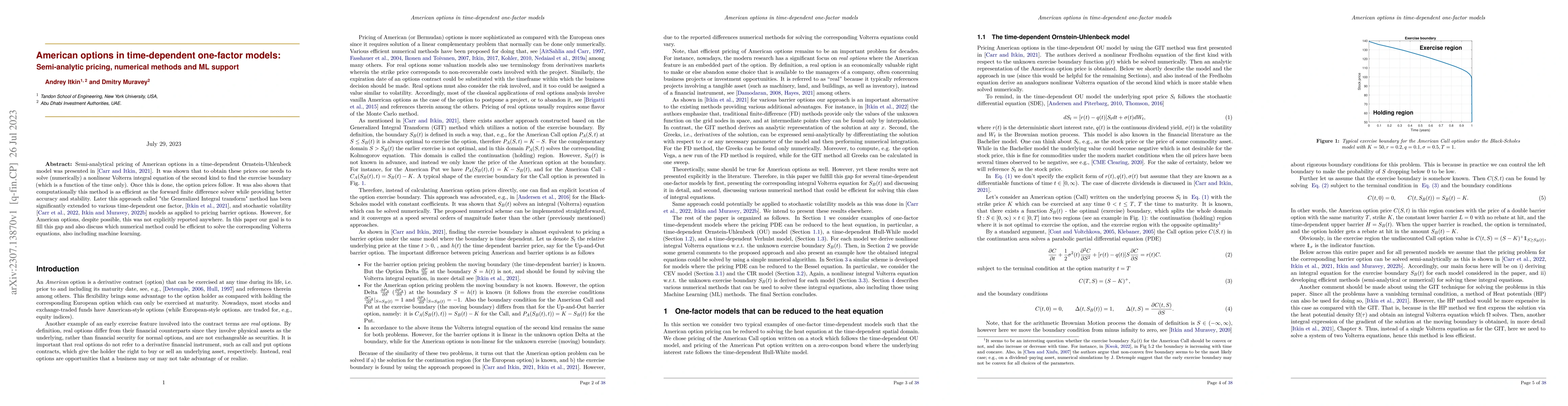

Semi-analytical pricing of American options in a time-dependent Ornstein-Uhlenbeck model was presented in [Carr, Itkin, 2020]. It was shown that to obtain these prices one needs to solve (numericall...

By expanding the Dirac delta function in terms of the eigenfunctions of the corresponding Sturm-Liouville problem, we construct some new (oscillating) integral transforms. These transforms are then ...

We extend the approach of Carr, Itkin and Muravey, 2021 for getting semi-analytical prices of barrier options for the time-dependent Heston model with time-dependent barriers by applying it to the s...

We continue a series of papers where prices of the barrier options written on the underlying, which dynamics follows some one factor stochastic model with time-dependent coefficients and the barrier...

In this paper we derive semi-closed form prices of barrier (perhaps, time-dependent) options for the Hull-White model, ie., where the underlying follows a time-dependent OU process with a mean-rever...

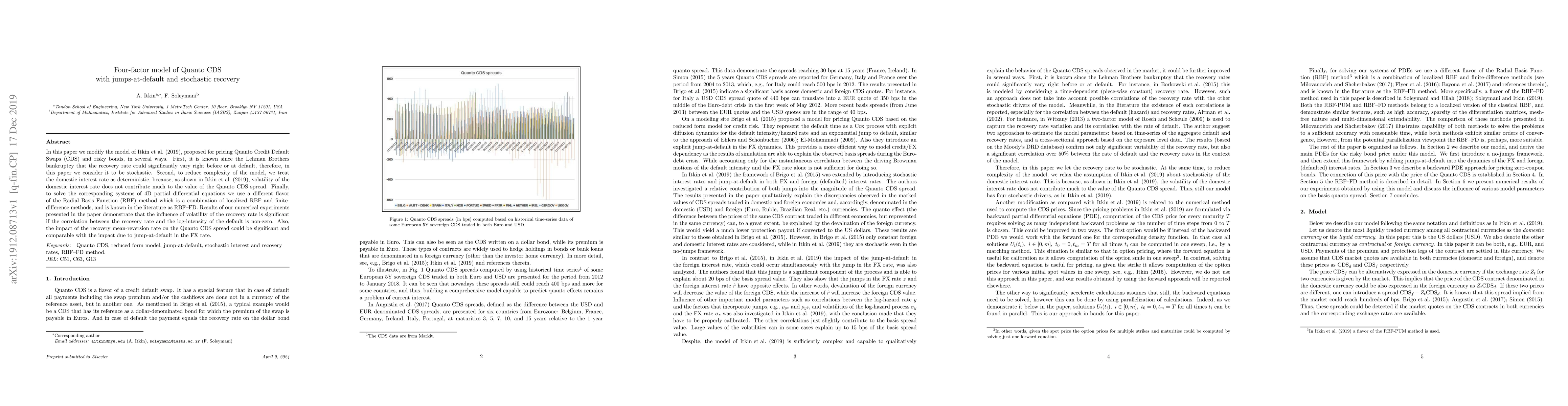

In this paper we modify the model of Itkin, Shcherbakov and Veygman, (2019) (ISV2019), proposed for pricing Quanto Credit Default Swaps (CDS) and risky bonds, in several ways. First, it is known sin...

We derive a backward and forward nonlinear PDEs that govern the implied volatility of a contingent claim whenever the latter is well-defined. This would include at least any contingent claim written...

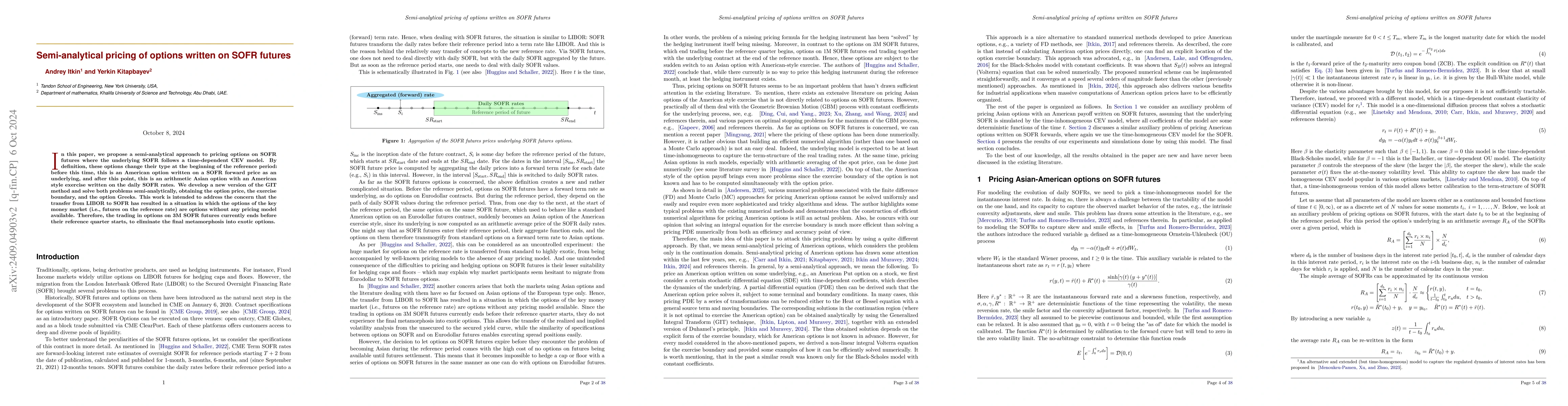

In this paper, we propose a semi-analytical approach to pricing options on SOFR futures where the underlying SOFR follows a time-dependent CEV model. By definition, these options change their type at ...

This paper examines a semi-analytical approach for pricing American options in time-inhomogeneous models characterized by negative interest rates (for equity, FX) or negative convenience yields (for c...

Despite significant advancements in machine learning for derivative pricing, the efficient and accurate valuation of American options remains a persistent challenge due to complex exercise boundaries,...

The Marketron model, introduced by [Halperin, Itkin, 2025], describes price formation in inelastic markets as the nonlinear diffusion of a quasiparticle (the marketron) in a multidimensional space com...

This paper introduces a semi-analytical method for pricing American options on assets (stocks, ETFs) that pay discrete and/or continuous dividends. The problem is notoriously complex because discrete ...

The Fokker-Planck equation is fundamental to statistical mechanics, yet in settings with multiple state variables, anisotropic (cross-) diffusion, and jumps, conventional discretizations frequently pr...

A flexible forward (FF) is a customized FX hedging instrument that guarantees a fixed exchange rate while letting the holder choose the delivery date within a pre-agreed window. It is therefore an Ame...