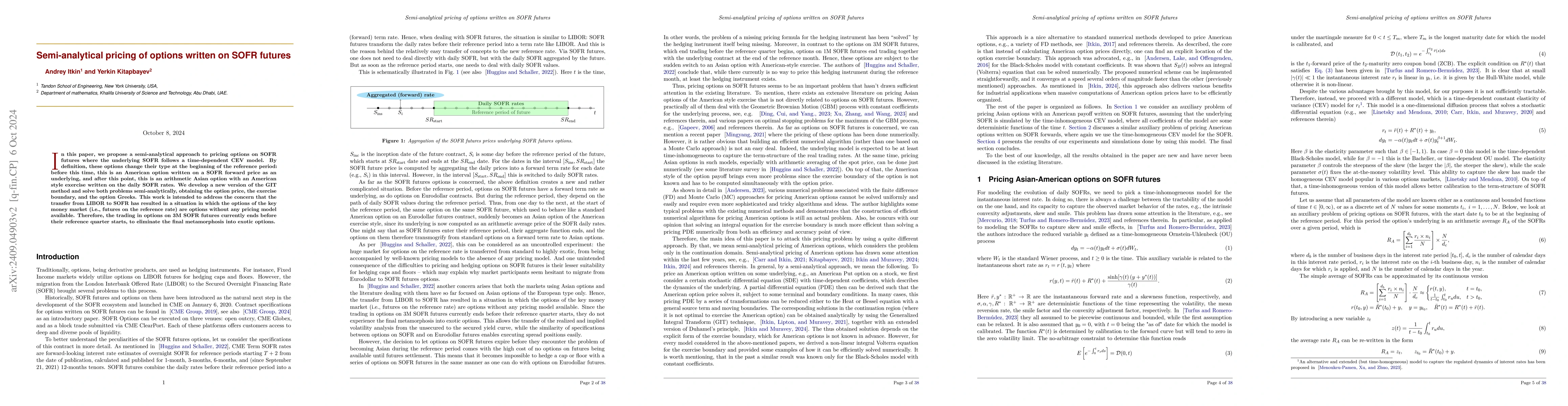

In this paper, we propose a semi-analytical approach to pricing options on

SOFR futures where the underlying SOFR follows a time-dependent CEV model. By

definition, these options change their type at the beginning of the reference

period: before this time, this is an American option written on a SOFR forward

price as an underlying, and after this point, this is an arithmetic Asian

option with an American style exercise written on the daily SOFR rates. We

develop a new version of the GIT method and solve both problems

semi-analytically, obtaining the option price, the exercise boundary, and the

option Greeks. This work is intended to address the concern that the transfer

from LIBOR to SOFR has resulted in a situation in which the options of the key

money market (i.e., futures on the reference rate) are options without any

pricing model available. Therefore, the trading in options on 3M SOFR futures

currently ends before their reference quarter starts, to eliminate the final

metamorphosis into exotic options.

Discussion 0