Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study a model of irreversible investment for a decision-maker who has the possibility to gradually invest in a project with unknown value. In this setting, we introduce and explore a feature of "...

In this paper, we study a pricing problem of the multiple reset put option, which allows the holder to reset several times a current strike price to obtain an at-the-money European put option. We fo...

We analyze recently proposed mortgage contracts that aim to eliminate selective borrower default when the loan balance exceeds the house price (the ``underwater'' effect). We show contracts that aut...

We present three models of stock price with time-dependent interest rate, dividend yield, and volatility, respectively, that allow for explicit forms of the optimal exercise boundary of the finite m...

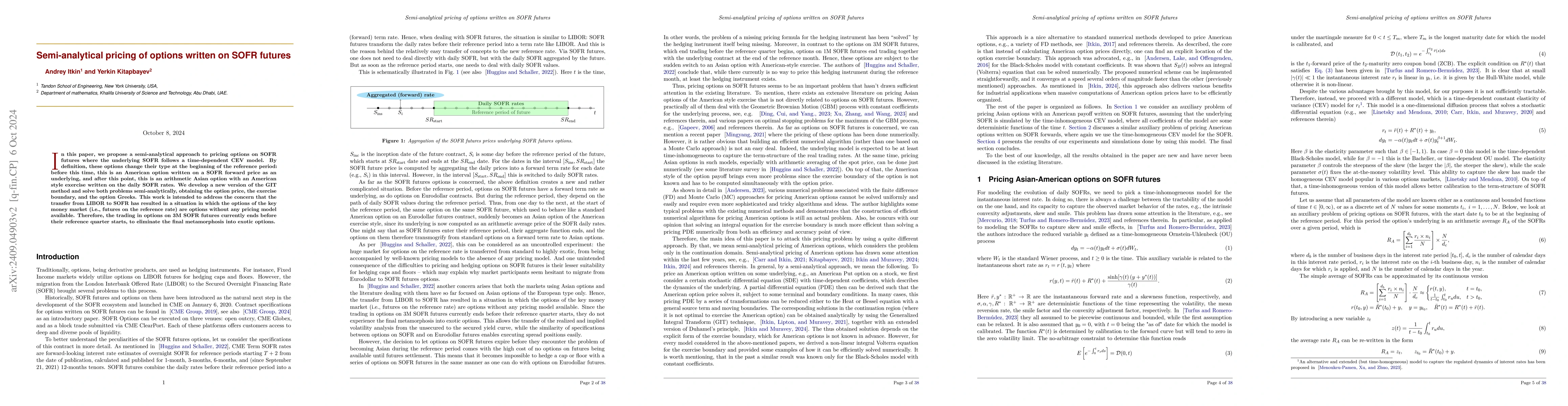

In this paper, we propose a semi-analytical approach to pricing options on SOFR futures where the underlying SOFR follows a time-dependent CEV model. By definition, these options change their type at ...

This paper examines a semi-analytical approach for pricing American options in time-inhomogeneous models characterized by negative interest rates (for equity, FX) or negative convenience yields (for c...