Academic Profile

Statistics

Similar Authors

Papers on arXiv

Based on supermodularity ordering properties, we show that convex risk measures of credit losses are nondecreasing w.r.t. credit-credit and, in a wrong-way risk setup, credit-market, covariances of ...

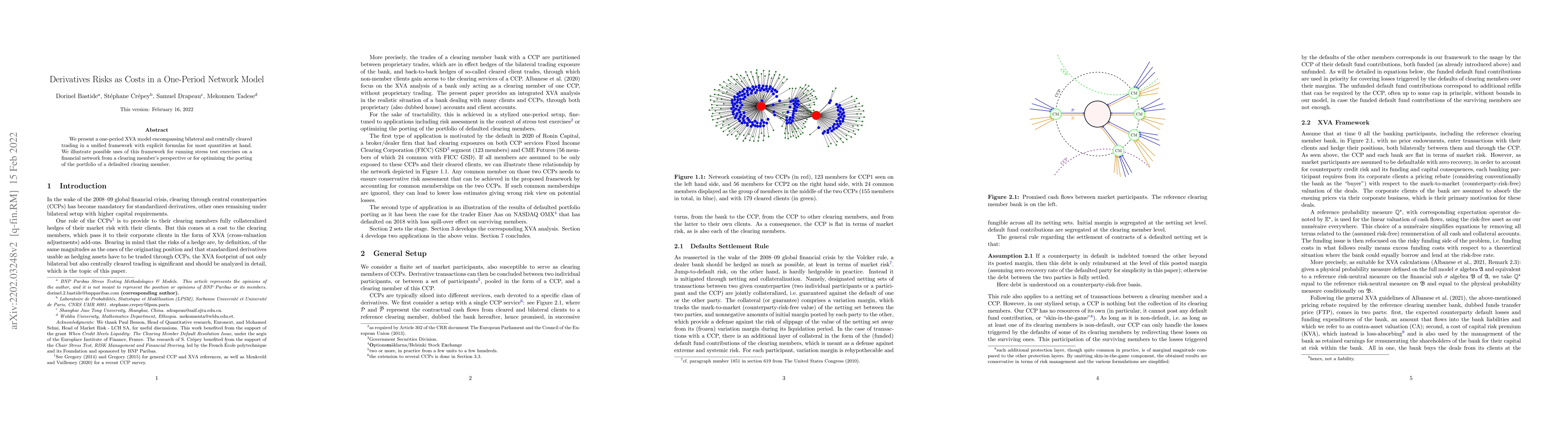

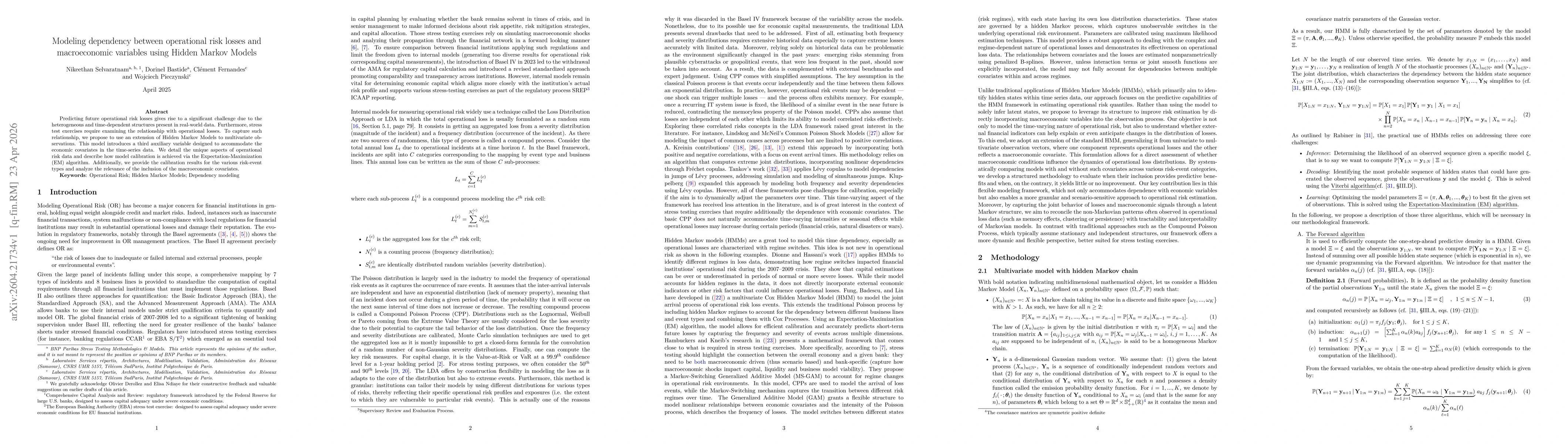

For vanilla derivatives that constitute the bulk of investment banks' hedging portfolios, central clearing through central counterparties (CCPs) has become hegemonic. A key mandate of a CCP is to pr...

We present a one-period XVA model encompassing bilateral and centrally cleared trading in a unified framework with explicit formulas for most quantities at hand. We illustrate possible uses of this ...

Predicting future operational risk losses gives rise to a significant challenge due to the heterogeneous and time-dependent structures present in real-world data. Furthermore, stress test exercises re...