Academic Profile

Statistics

Similar Authors

Papers on arXiv

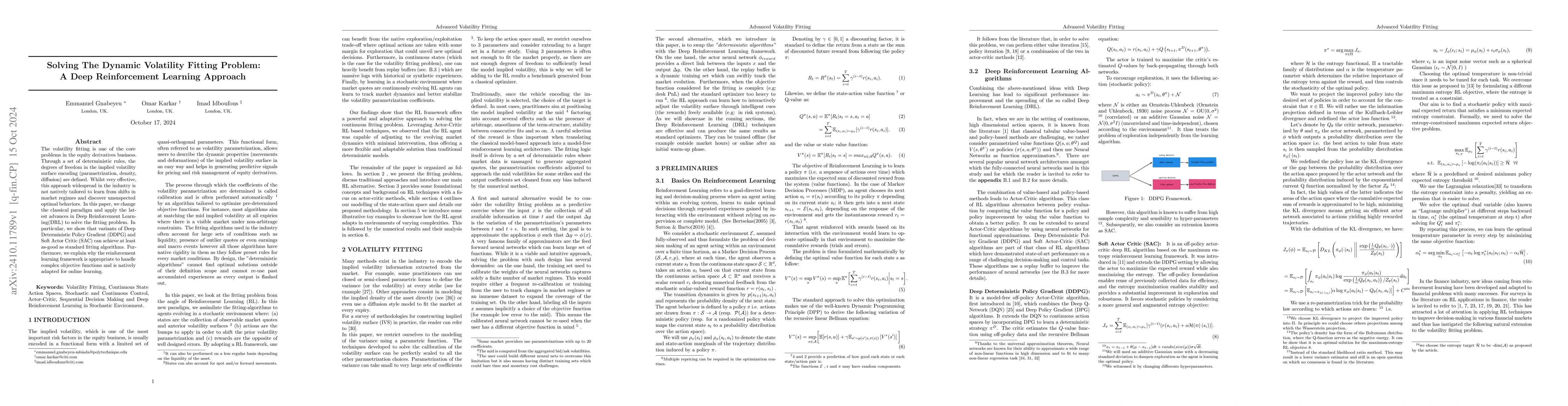

The volatility fitting is one of the core problems in the equity derivatives business. Through a set of deterministic rules, the degrees of freedom in the implied volatility surface encoding (parametr...

This paper provide a comprehensive analysis of the finite and long time behavior of continuous-time non-Markovian dynamical systems, with a focus on the forward Stochastic Volterra Integral Equations(...

True Volterra equations are inherently non stationary and therefore do not admit $\textit{genuine stationary regimes}$ over finite horizons. This motivates the study of the finite-time behavior of the...

This paper investigates the asymptotic behavior of suitably time-modulated Hawkes processes with heavy-tailed kernels in a nearly unstable regime. We show that, under appropriate scaling, both the int...

This paper is concerned with Merton's portfolio optimization problem in a Volterra stochastic environment described by a multivariate fake stationary Volterra--Heston model. Due to the non-Markovianit...

The aim of this paper is to provide a comprehensive analysis of the path-dependent Stochastic Volterra Integral Equations (SVIEs), in which both the drift and the diffusion coefficients are allowed to...

We investigate the continuous-time Markowitz mean-variance portfolio selection problem within a multivariate class of fake stationary affine Volterra models. In this non-Markovian and non-semimartinga...

This paper is concerned with portfolio selection for an investor with exponential, power, and logarithmic utility in multi-asset financial markets allowing jumps. We investigate the classical Merton's...