Academic Profile

Statistics

Similar Authors

Papers on arXiv

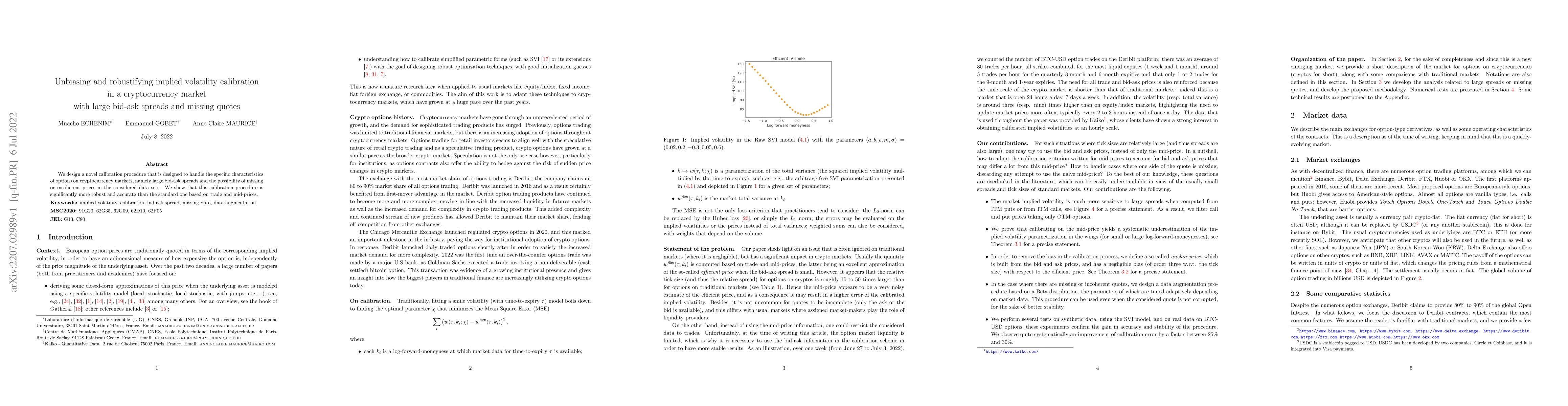

We design a novel calibration procedure that is designed to handle the specific characteristics of options on cryptocurrency markets, namely large bid-ask spreads and the possibility of missing or i...

We provide explicit approximation formulas for VIX futures and options in forward variance models, with particular emphasis on the family of so-called Bergomi models: the one-factor Bergomi model [B...

In this paper we present a series of results that permit to extend in a direct manner uniform deviation inequalities of the empirical process from the independent to the dependent case characterizin...

In this work we study the numerical approximation of a class of ergodic Backward Stochastic Differential Equations. These equations are formulated in an infinite horizon framework and provide a probab...

We study backward stochastic differential equations (BSDEs) in infinite horizon and design efficient numerical schemes for solving them. We establish a probabilistic representation of the solution of ...