Academic Profile

Statistics

Similar Authors

Papers on arXiv

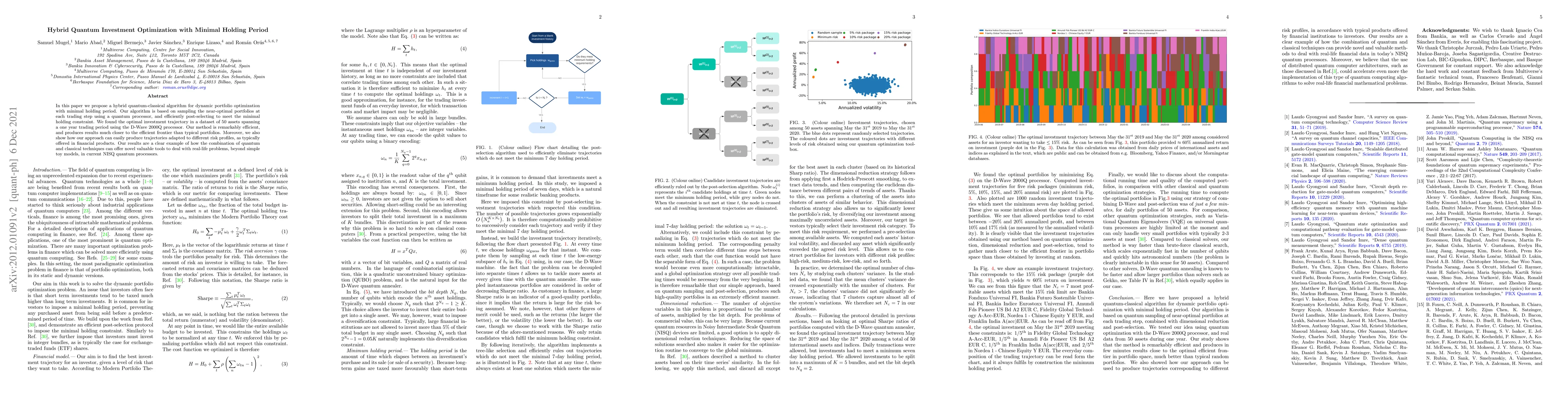

In this paper we propose a hybrid quantum-classical algorithm for dynamic portfolio optimization with minimal holding period. Our algorithm is based on sampling the near-optimal portfolios at each t...

In this paper we briefly review two recent use-cases of quantum optimization algorithms applied to hard problems in finance and economy. Specifically, we discuss the prediction of financial crashes ...

In this paper we tackle the problem of dynamic portfolio optimization, i.e., determining the optimal trading trajectory for an investment portfolio of assets over a period of time, taking into accou...

Prediction of financial crashes in a complex financial network is known to be an NP-hard problem, which means that no known algorithm can guarantee to find optimal solutions efficiently. We experime...

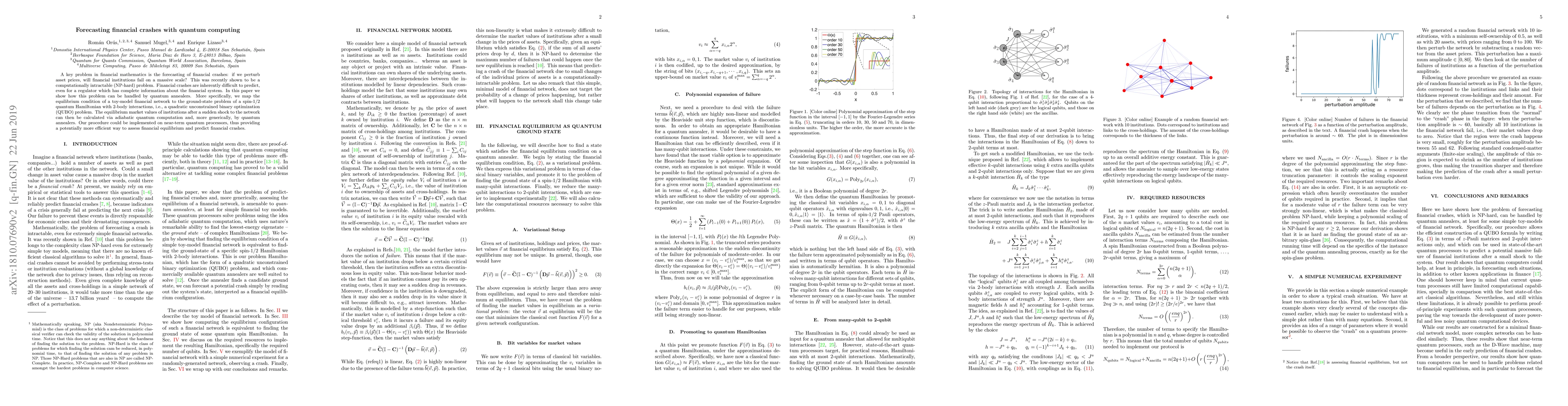

A key problem in financial mathematics is the forecasting of financial crashes: if we perturb asset prices, will financial institutions fail on a massive scale? This was recently shown to be a compu...