Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, a new way to integrate volatility information for estimating value at risk (VaR) and conditional value at risk (CVaR) of a portfolio is suggested. The new method is developed from the...

In this paper we construct a shrinkage estimator of the global minimum variance (GMV) portfolio by a combination of two techniques: Tikhonov regularization and direct shrinkage of portfolio weights....

The main contribution of this paper is the derivation of the asymptotic behaviour of the out-of-sample variance, the out-of-sample relative loss, and of their empirical counterparts in the high-dime...

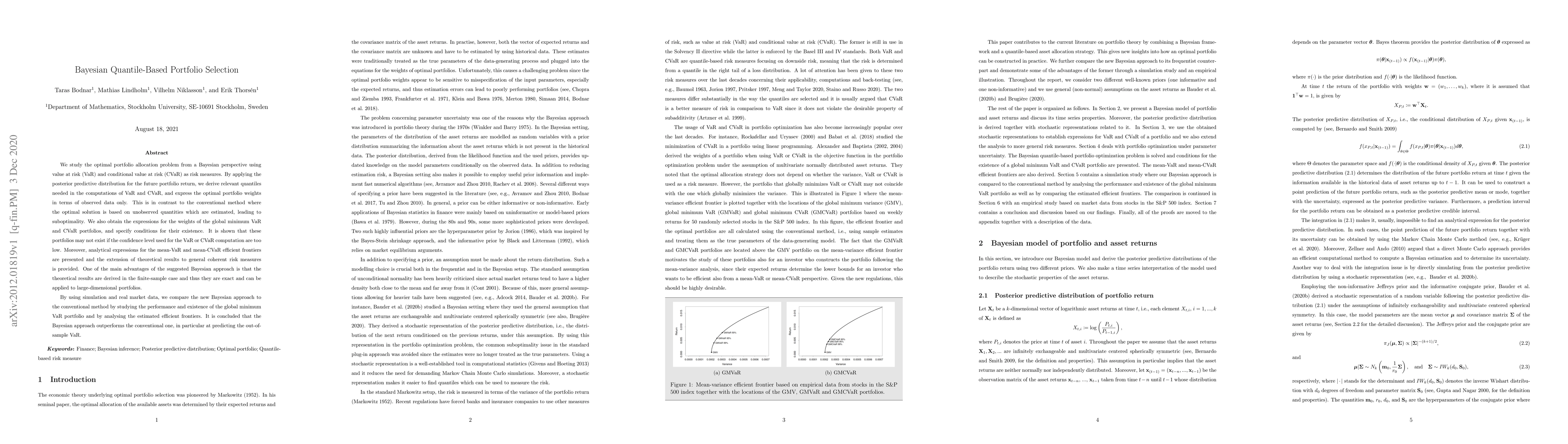

We study the optimal portfolio allocation problem from a Bayesian perspective using value at risk (VaR) and conditional value at risk (CVaR) as risk measures. By applying the posterior predictive di...

Optimal portfolio selection problems are determined by the (unknown) parameters of the data generating process. If an investor wants to realise the position suggested by the optimal portfolios, he/s...