Academic Profile

Statistics

Similar Authors

Papers on arXiv

Building on the one-to-one relationship between generalized FGM copulas and multivariate Bernoulli distributions, we prove that the class of multivariate distributions with generalized FGM copulas i...

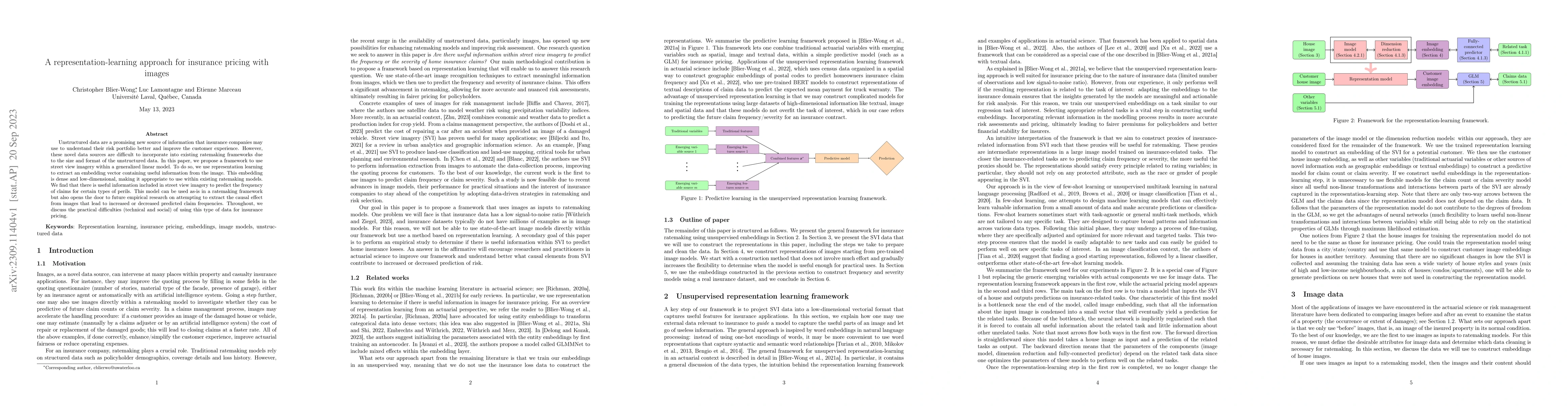

Unstructured data are a promising new source of information that insurance companies may use to understand their risk portfolio better and improve the customer experience. However, these novel data ...

We propose an approach to construct a new family of generalized Farlie-Gumbel-Morgenstern (GFGM) copulas that naturally scales to high dimensions. A GFGM copula can model moderate positive and negat...

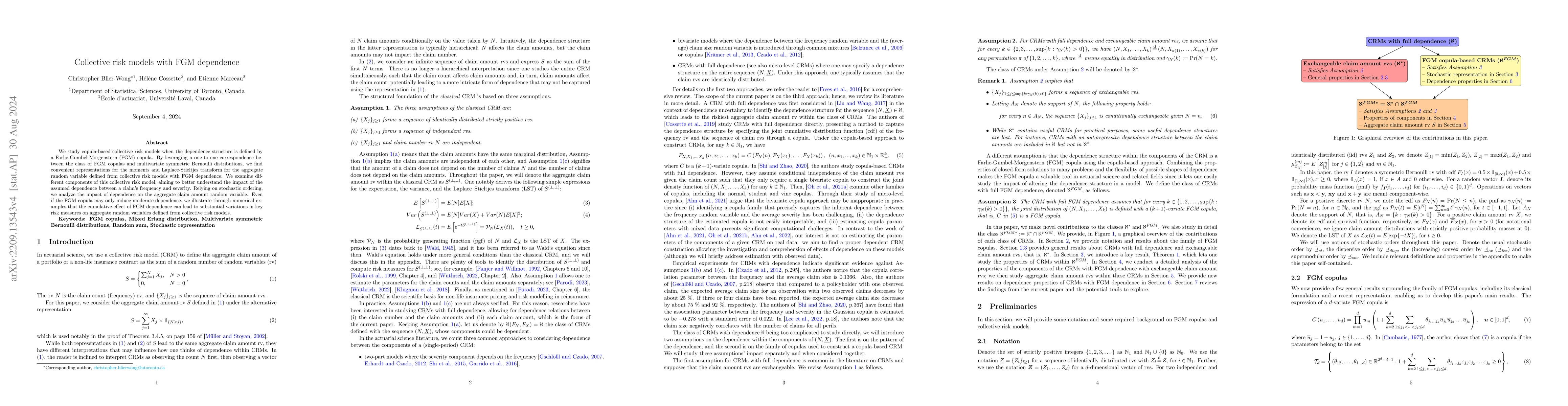

We study copula-based collective risk models when the dependence structure is defined by a Farlie-Gumbel-Morgenstern (FGM) copula. By leveraging a one-to-one correspondence between the class of FGM ...

We offer a new perspective on risk aggregation with FGM copulas. Along the way, we discover new results and revisit existing ones, providing simpler formulas than one can find in the existing litera...

Consider a risk portfolio with aggregate loss random variable $S=X_1+\dots +X_n$ defined as the sum of the $n$ individual losses $X_1, \dots, X_n$. The expected allocation, $E[X_i \times 1_{\{S = k\...

Copulas are a powerful tool to model dependence between the components of a random vector. One well-known class of copulas when working in two dimensions is the Farlie-GumbelMorgenstern (FGM) copula...

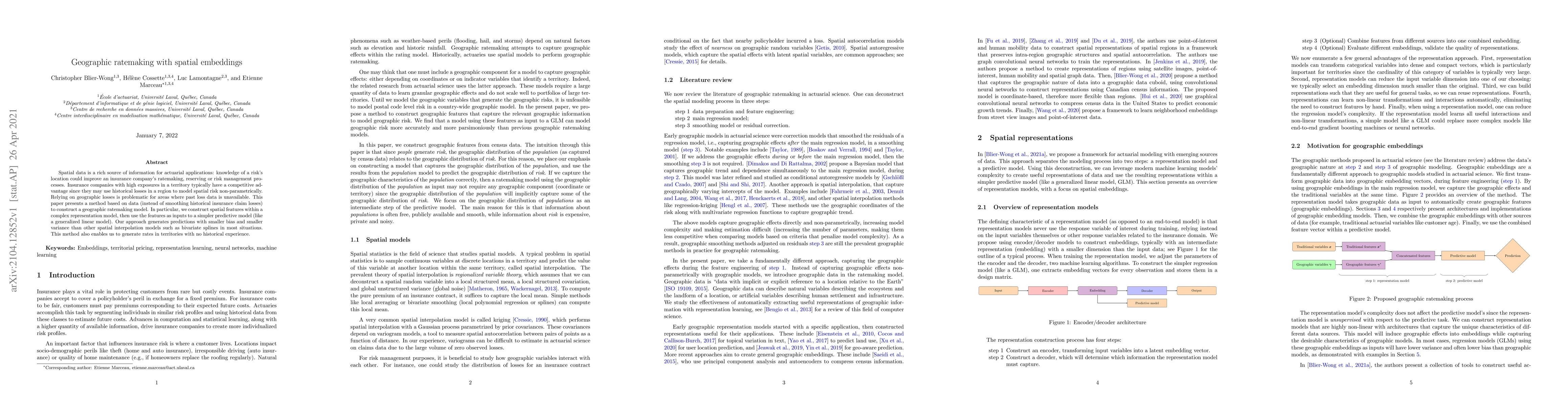

Spatial data is a rich source of information for actuarial applications: knowledge of a risk's location could improve an insurance company's ratemaking, reserving or risk management processes. Insur...

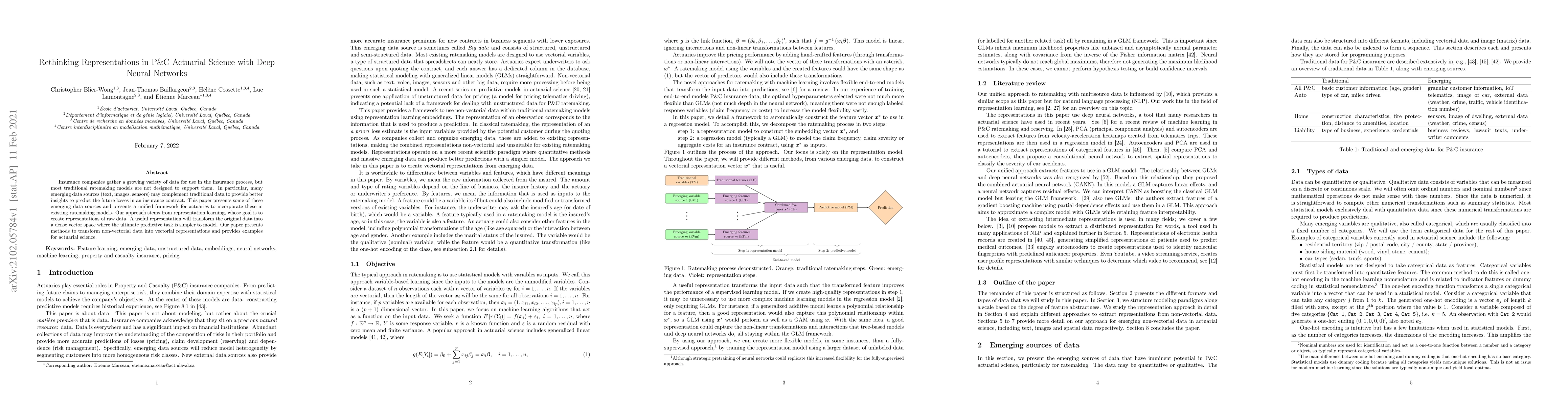

Insurance companies gather a growing variety of data for use in the insurance process, but most traditional ratemaking models are not designed to support them. In particular, many emerging data sour...

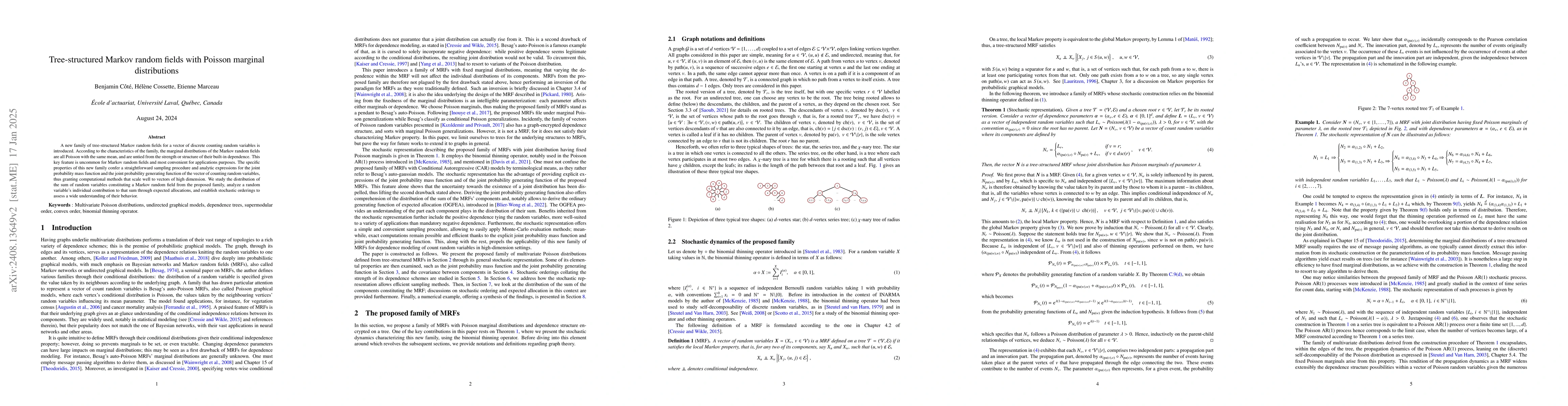

A new family of tree-structured Markov random fields for a vector of discrete counting random variables is introduced. According to the characteristics of the family, the marginal distributions of the...

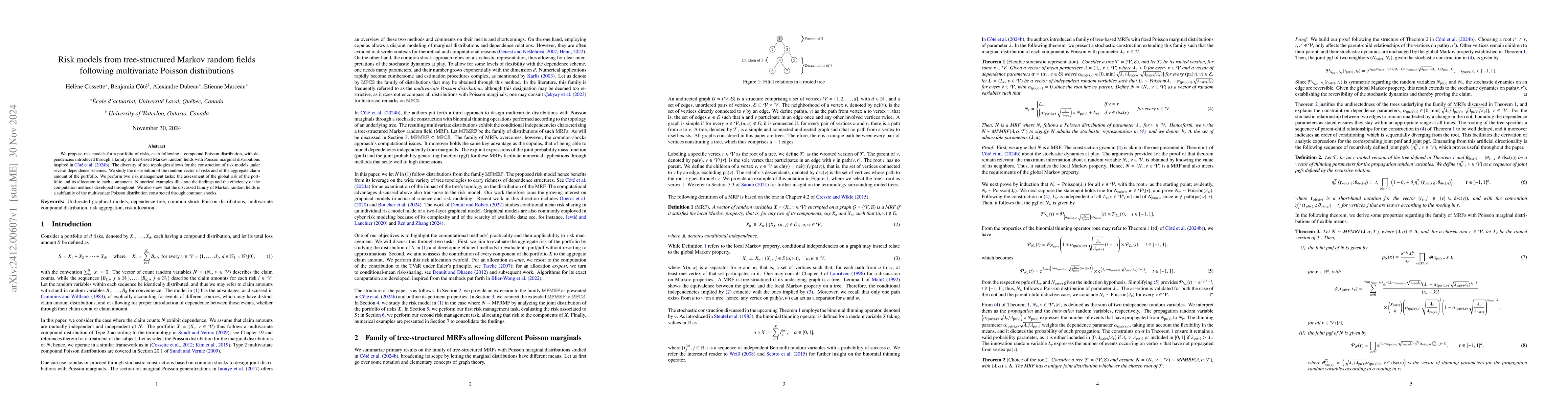

We propose risk models for a portfolio of risks, each following a compound Poisson distribution, with dependencies introduced through a family of tree-based Markov random fields with Poisson marginal ...

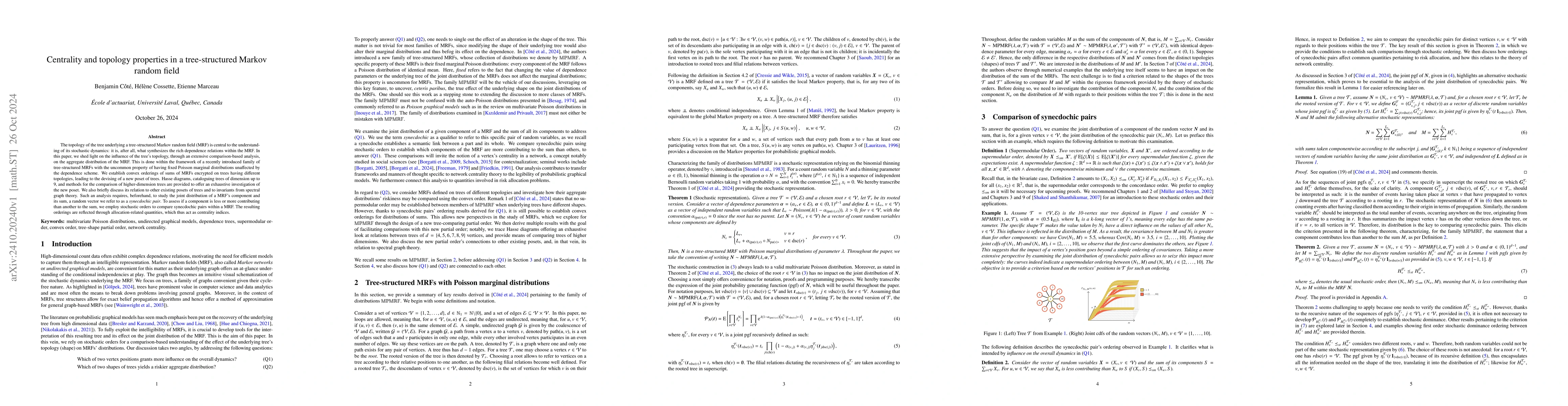

The topology of the tree underlying a tree-structured Markov random field (MRF) is central to the understanding of its stochastic dynamics: it is, after all, what synthesizes the rich dependence relat...

We provide a geometrical characterization of extremal negative dependence as a convex polytope in the simplex of multidimensional Bernoulli distributions, and we prove that it is an antichain that sat...

We assess advantages of expressing tree-structured Ising models via their mean parameterization rather than their commonly chosen canonical parameterization. This includes fixedness of marginal distri...

We investigate the Conway--Maxwell multivariate Bernoulli distributions, a family of multivariate Bernoulli distributions derived from the Conway--Maxwell-binomial distribution. We show that it is pos...