Academic Profile

Statistics

Similar Authors

Papers on arXiv

We generalize the characterization theorem going back to Mercer and Young, which states that a symmetric and continuous kernel is positive definite if and only if it is integrally positive definite....

We consider a class of optimal portfolio choice problems in continuous time where the agent's transactions create both transient cross-impact driven by a matrix-valued Volterra propagator, as well a...

We consider an offline learning problem for an agent who first estimates an unknown price impact kernel from a static dataset, and then designs strategies to liquidate a risky asset while creating t...

We consider a general class of finite-player stochastic games with mean-field interaction, in which the linear-quadratic cost functional includes linear operators acting on controls in $L^2$. We pro...

We study the effective radius of weakly self-avoiding star polymers in one, two, and three dimensions. Our model includes $N$ Brownian motions up to time $T$, started at the origin and subject to ex...

We consider a class of learning problems in which an agent liquidates a risky asset while creating both transient price impact driven by an unknown convolution propagator and linear temporary price ...

We consider a class of optimal liquidation problems where the agent's transactions create transient price impact driven by a Volterra-type propagator along with temporary price impact. We formulate ...

We consider a stochastic game between a slow institutional investor and a high-frequency trader who are trading a risky asset and their aggregated order-flow impacts the asset price. We model this s...

We consider self-repelling elastic manifolds with a domain $[-N,N]^d \cap \mathbb{Z}^d$, that take values in $\mathbb{R}^D$. Our main result states that when the dimension of the domain is $d=2$ and...

We study elastic manifolds with self-repelling terms and estimate their effective radius. This class of manifolds is modelled by a self-repelling vector-valued Gaussian free field with Neumann bound...

We study a multi-player stochastic differential game, where agents interact through their joint price impact on an asset that they trade to exploit a common trading signal. In this context, we prove...

We formulate and solve a multi-player stochastic differential game between financial agents who seek to cost-efficiently liquidate their position in a risky asset in the presence of jointly aggregat...

We consider a stochastic game between three types of players: an inside trader, noise traders and a market maker. In a similar fashion to Kyle's model, we assume that the insider first chooses the s...

We introduce a first theory of price impact in presence of an interest-rates term structure. We explain how one can formulate instantaneous and transient price impact on bonds with different maturit...

We consider a family of fractional Brownian fields $\{B^{H}\}_{H\in (0,1)}$ on $\mathbb{R}^{d}$, where $H$ denotes their Hurst parameter. We first define a rich class of normalizing kernels $\psi$ s...

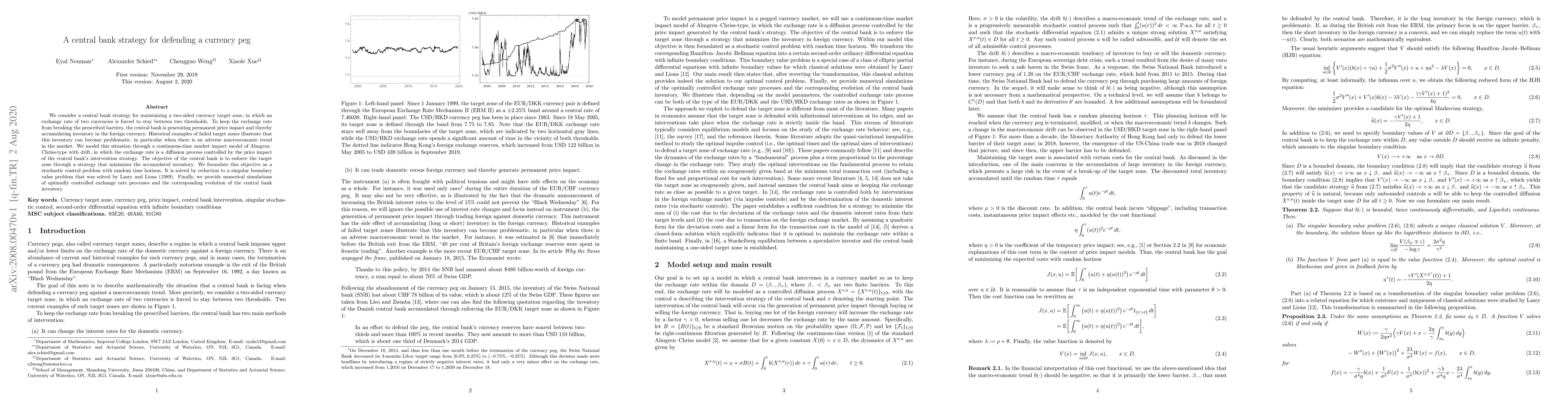

We consider a central bank strategy for maintaining a two-sided currency target zone, in which an exchange rate of two currencies is forced to stay between two thresholds. To keep the exchange rate ...

We develop a methodology which replicates in great accuracy the FTSE Russell indexes reconstitutions, including the quarterly rebalancings due to new initial public offerings (IPOs). While using onl...

We set up an SPDE model for a moving, weakly self-avoiding polymer with intrinsic length $J$ taking values in $(0,\infty)$. Our main result states that the effective radius of the polymer is approxi...

We study optimal liquidation in the presence of linear temporary and transient price impact along with taking into account a general price predicting finite-variation signal. We formulate this probl...

We consider a branching random walk on $\mathbb{Z}$ started by $n$ particles at the origin, where each particle disperses according to a mean-zero random walk with bounded support and reproduces wit...

We compare optimal static and dynamic solutions in trade execution. An optimal trade execution problem is considered where a trader is looking at a short-term price predictive signal while trading. ...

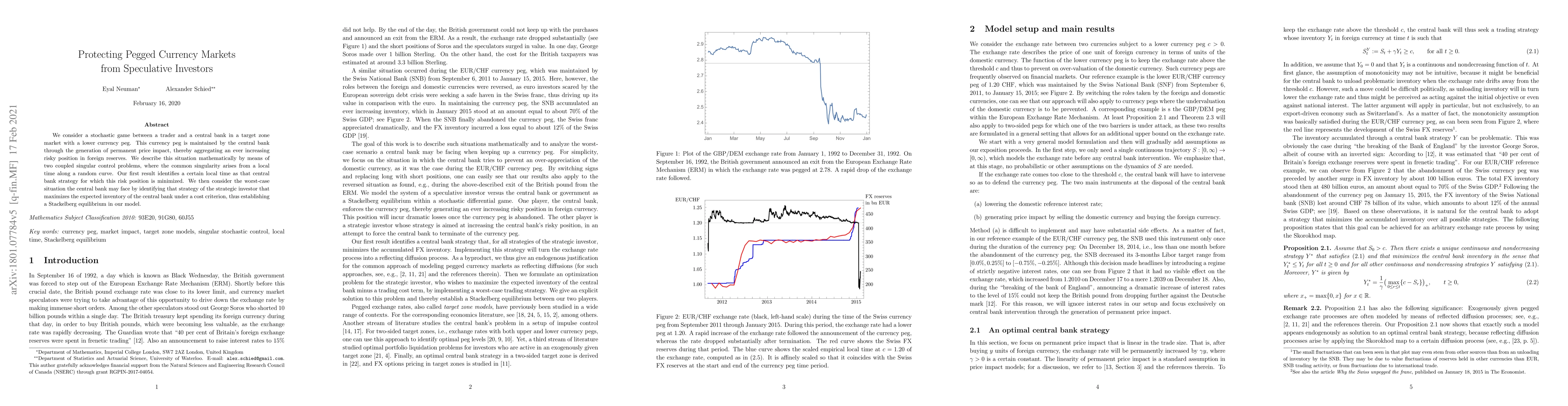

We consider a stochastic game between a trader and a central bank in a target zone market with a lower currency peg. This currency peg is maintained by the central bank through the generation of per...

We consider a central trading desk which aggregates the inflow of clients' orders with unobserved toxicity, i.e. persistent adverse directionality. The desk chooses either to internalise the inflow or...

Maglaras, Moallemi, and Zheng (2021) have introduced a flexible queueing model for fragmented limit-order markets, whose fluid limit remains remarkably tractable. In the present study we prove that, i...

We study finite-player dynamic stochastic games with heterogeneous interactions and non-Markovian linear-quadratic objective functionals. We derive the Nash equilibrium explicitly by converting the fi...

We formulate and solve an optimal trading problem with alpha signals, where transactions induce a nonlinear transient price impact described by a general propagator model, including power-law decay. U...

We consider a class of targeted intervention problems in dynamic network and graphon games. First, we study a general dynamic network game in which players interact over a graph and maximize their het...

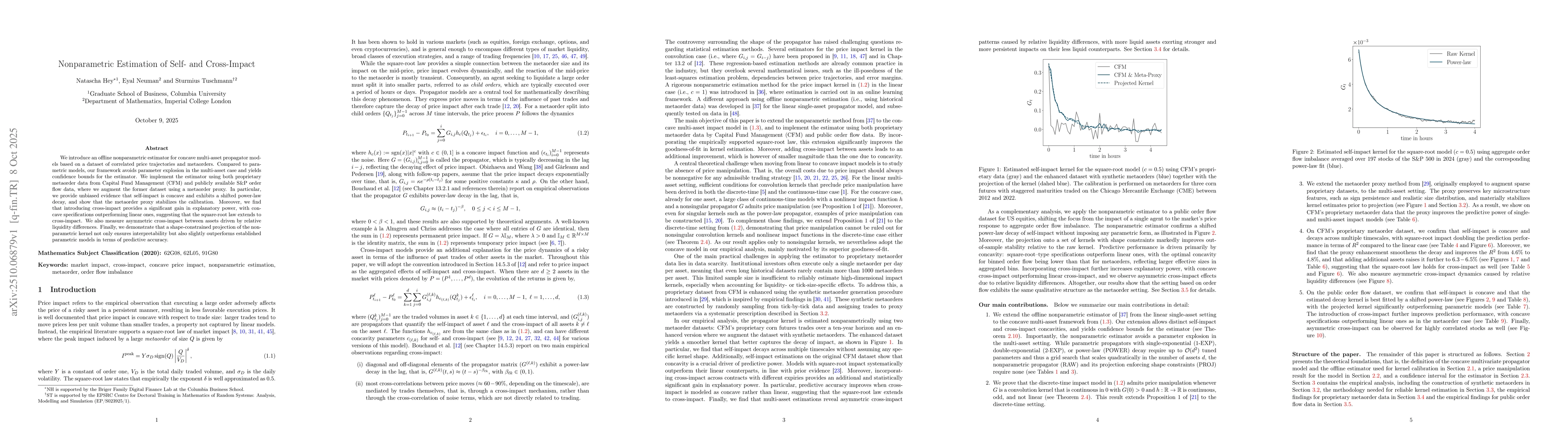

We introduce an offline nonparametric estimator for concave multi-asset propagator models based on a dataset of correlated price trajectories and metaorders. Compared to parametric models, our framewo...

As the FX markets continue to evolve, many institutions have started offering passive access to their internal liquidity pools. Market makers act as principal and have the opportunity to fill those or...

We introduce a framework for stochastic games on large sparse graphs, covering continuous-time and discrete-time dynamic games as well as static games. Players are indexed by the vertices of simple, l...

We study potential games on unimodular random graphs of bounded degree, where players interact through the underlying network. Using the unimodular measure, we define a well-posed global potential tha...

We model a market with multiple dealers who compete for client order flow by dynamically updating their bid and ask quotes for a risky asset. Dealers aim to maximise expected profits while controlling...