Academic Profile

Statistics

Similar Authors

Papers on arXiv

We focus on the time-varying modeling of VaR at a given coverage $\tau$, assessing whether the quantiles of the distribution of the returns standardized by their conditional means and standard devia...

In December 2017, two leading derivative exchanges, CBOE and CME, introduced the first regulated Bitcoin futures. Our aim is estimating their causal impact on Bitcoin volatility and trading volume. ...

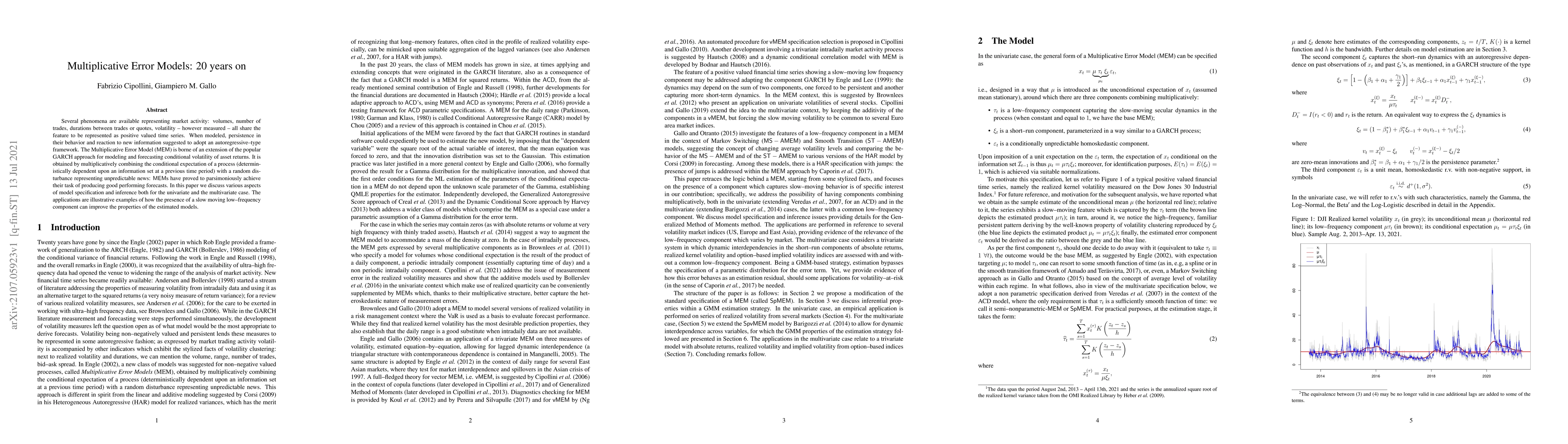

Several phenomena are available representing market activity: volumes, number of trades, durations between trades or quotes, volatility - however measured - all share the feature to be represented a...

We suggest the Doubly Multiplicative Error class of models (DMEM) for modeling and forecasting realized volatility, which combines two components accommodating low-, respectively, high-frequency fea...

We build the time series of optimal realized portfolio weights from high-frequency data and we suggest a novel Dynamic Conditional Weights (DCW) model for their dynamics. DCW is benchmarked against ...

VOLARE (VOLatility Archive for Realized Estimates - https://volare.unime.it) is an open research infrastructure providing standardized realized volatility and covariance measures constructed from ultr...