Academic Profile

Statistics

Similar Authors

Papers on arXiv

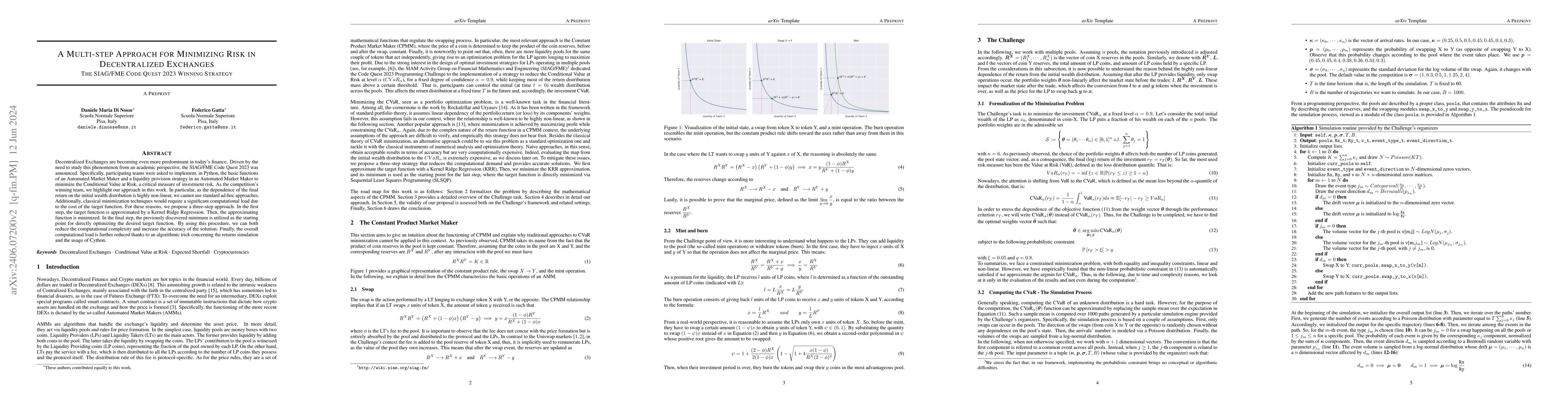

Decentralized Exchanges are becoming even more predominant in today's finance. Driven by the need to study this phenomenon from an academic perspective, the SIAG/FME Code Quest 2023 was announced. S...

In financial risk management, Value at Risk (VaR) is widely used to estimate potential portfolio losses. VaR's limitation is its inability to account for the magnitude of losses beyond a certain thres...

We propose a new approach, termed Realized Risk Measures (RRM), to estimate Value-at-Risk (VaR) and Expected Shortfall (ES) using high-frequency financial data. It extends the Realized Quantile (RQ) a...

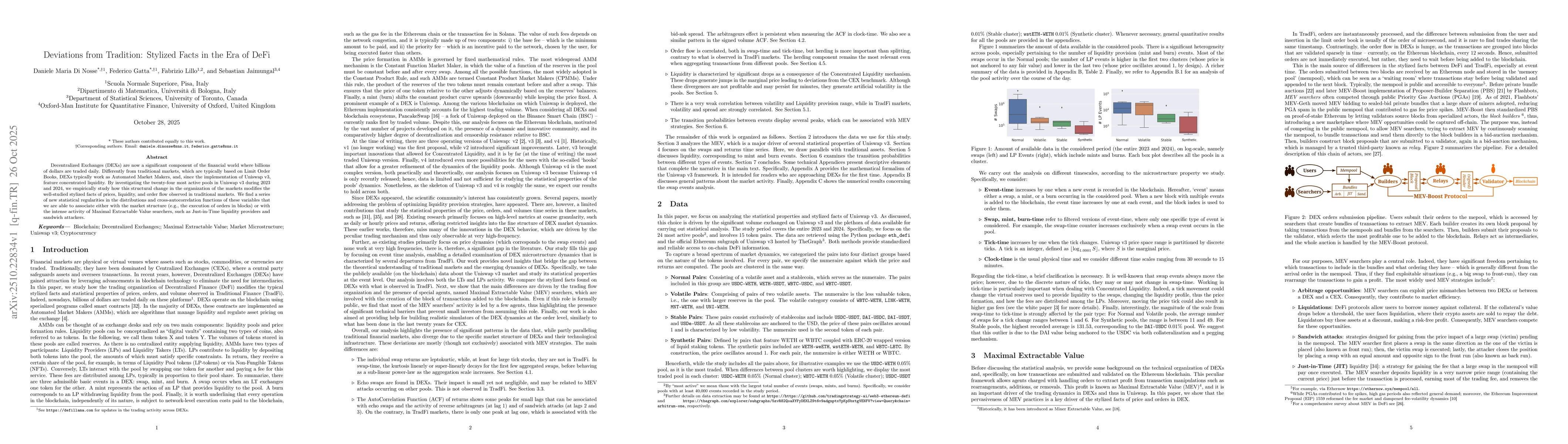

Decentralized Exchanges (DEXs) are now a significant component of the financial world where billions of dollars are traded daily. Differently from traditional markets, which are typically based on Lim...