Academic Profile

Statistics

Similar Authors

Papers on arXiv

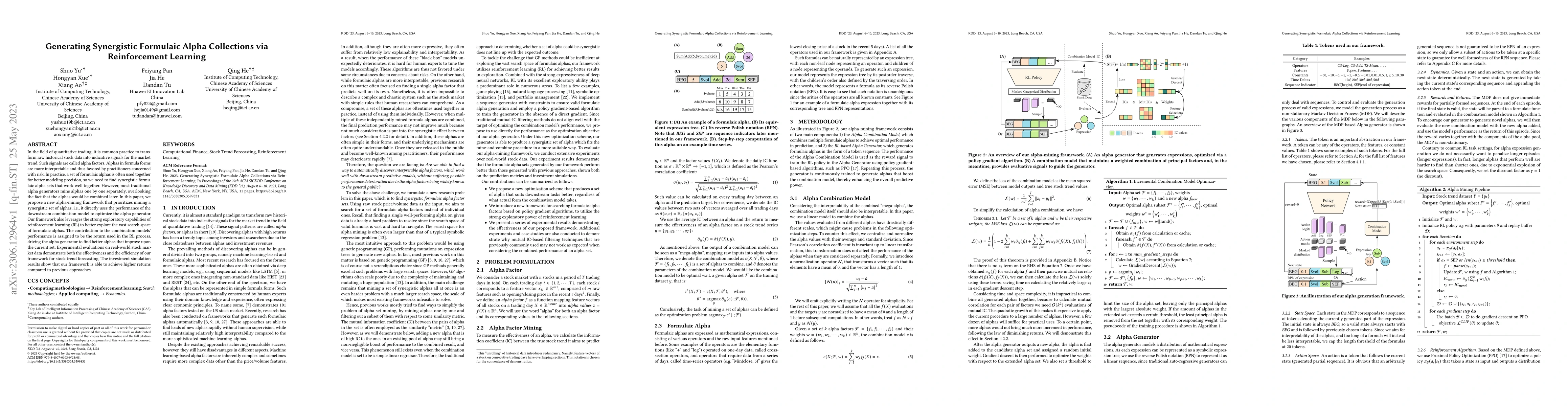

In the field of quantitative trading, it is common practice to transform raw historical stock data into indicative signals for the market trend. Such signals are called alpha factors. Alphas in form...

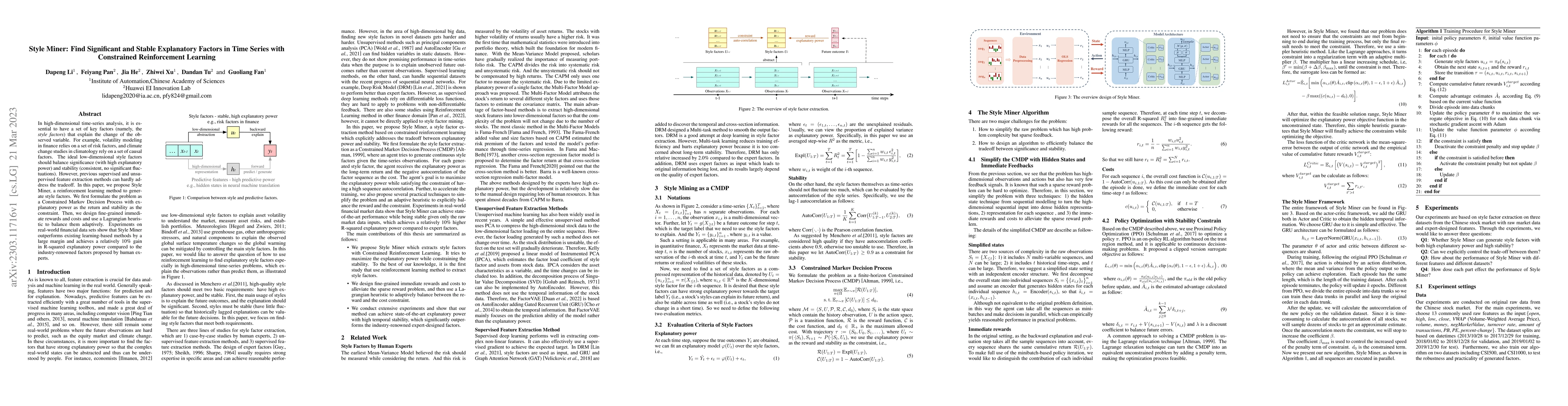

In high-dimensional time-series analysis, it is essential to have a set of key factors (namely, the style factors) that explain the change of the observed variable. For example, volatility modeling ...

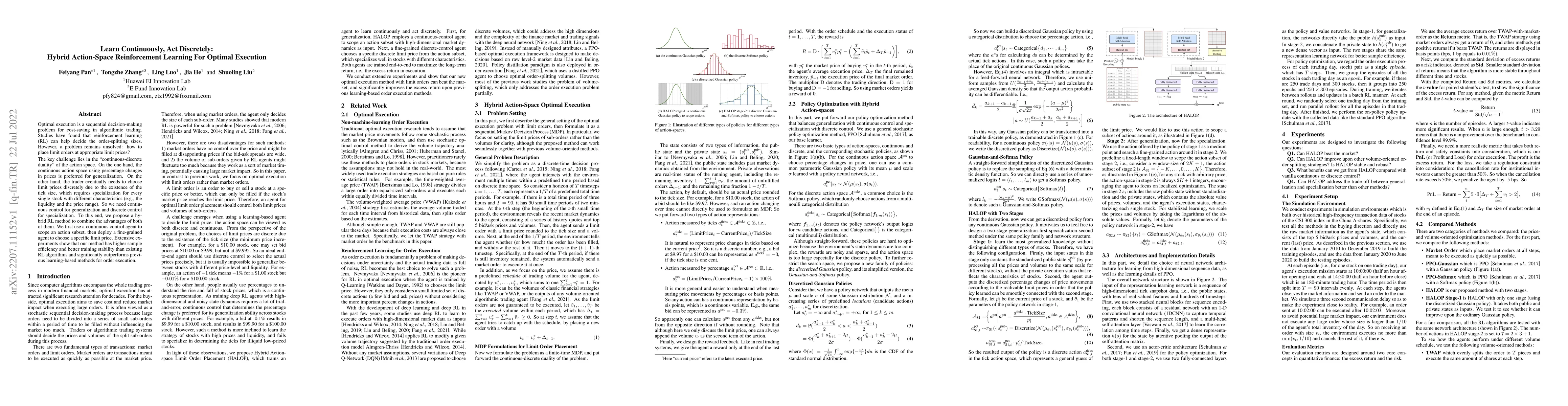

Optimal execution is a sequential decision-making problem for cost-saving in algorithmic trading. Studies have found that reinforcement learning (RL) can help decide the order-splitting sizes. Howev...

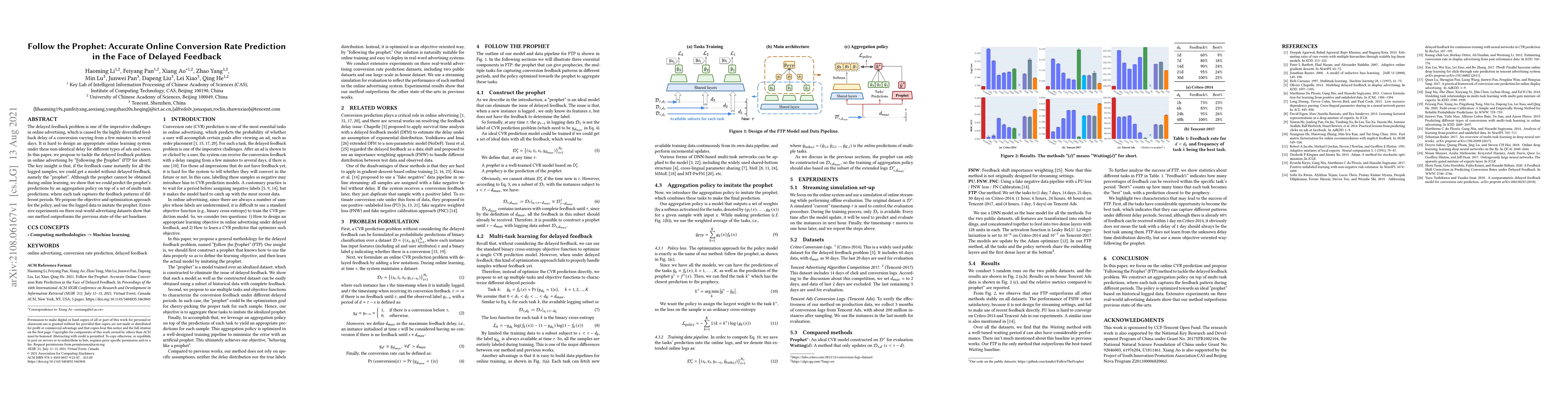

The delayed feedback problem is one of the imperative challenges in online advertising, which is caused by the highly diversified feedback delay of a conversion varying from a few minutes to several...

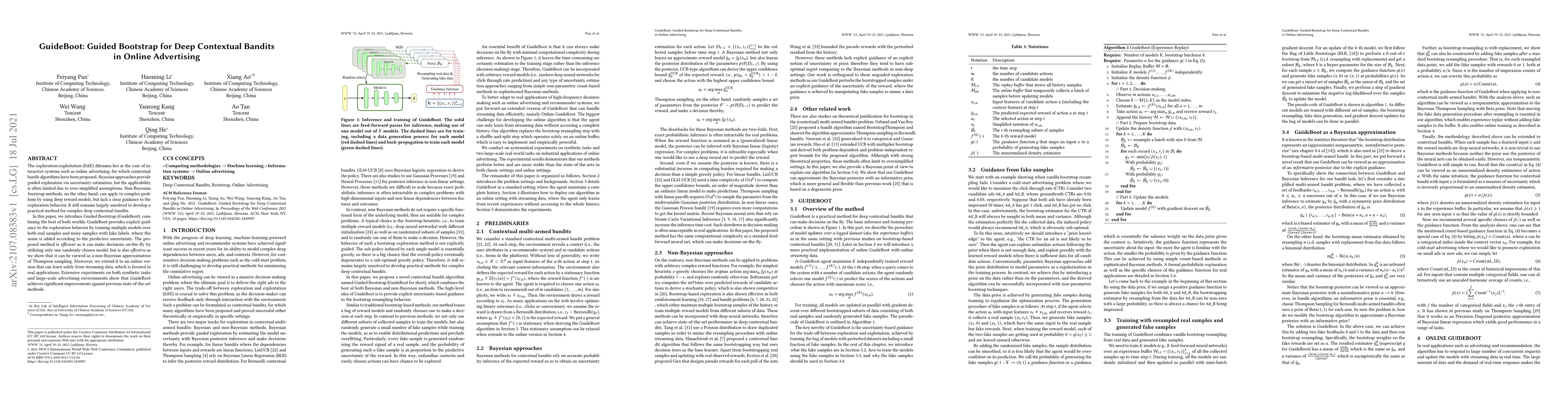

The exploration/exploitation (E&E) dilemma lies at the core of interactive systems such as online advertising, for which contextual bandit algorithms have been proposed. Bayesian approaches provide ...

It is a popular belief that model-based Reinforcement Learning (RL) is more sample efficient than model-free RL, but in practice, it is not always true due to overweighed model errors. In complex an...

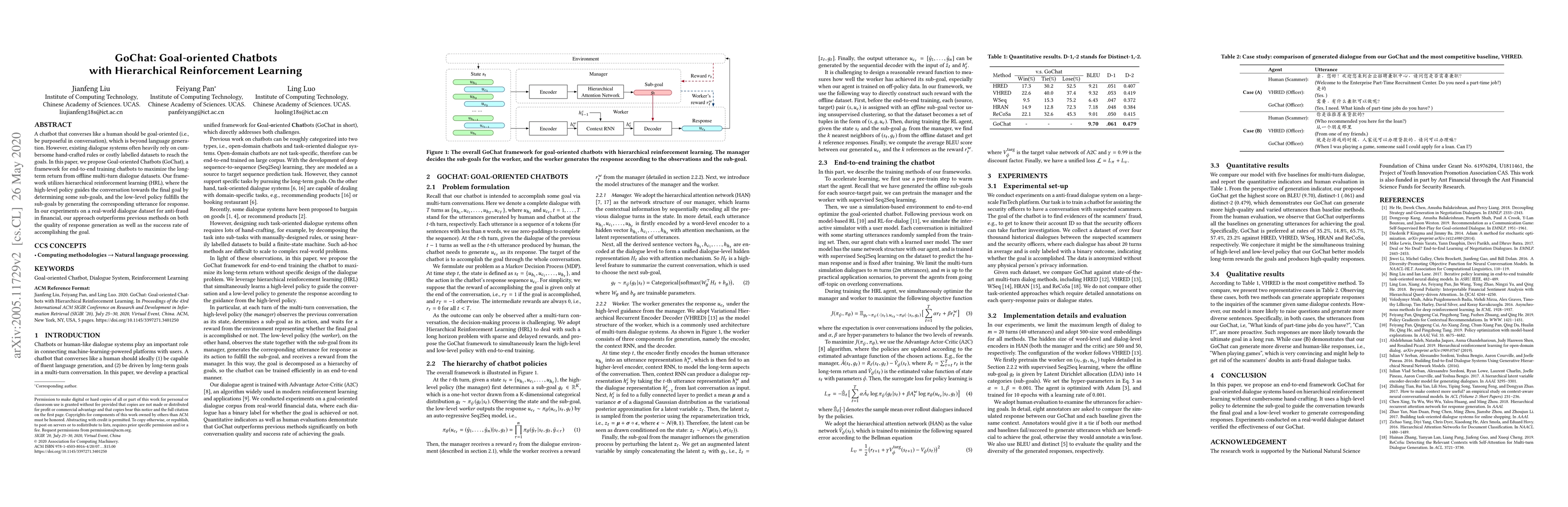

A chatbot that converses like a human should be goal-oriented (i.e., be purposeful in conversation), which is beyond language generation. However, existing dialogue systems often heavily rely on cum...

Distilling reasoning paths from teacher to student models via supervised fine-tuning (SFT) provides a shortcut for improving the reasoning ability of smaller Large Language Models (LLMs). However, the...

MEMS gyroscopes play a critical role in inertial navigation and motion control applications but typically suffer from a fundamental trade-off between measurement range and noise performance. Existing ...

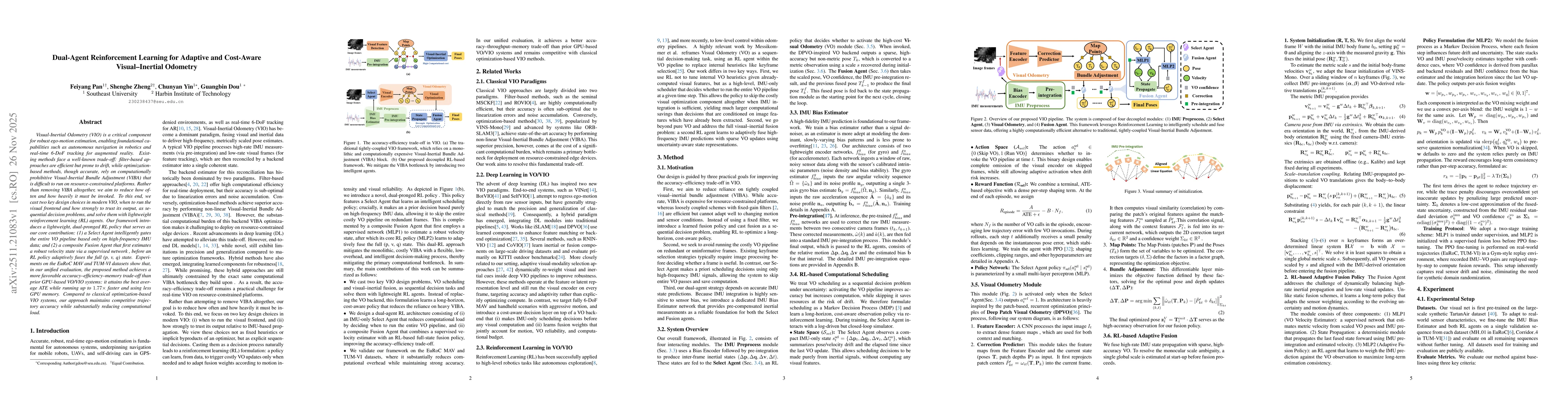

Visual-Inertial Odometry (VIO) is a critical component for robust ego-motion estimation, enabling foundational capabilities such as autonomous navigation in robotics and real-time 6-DoF tracking for a...

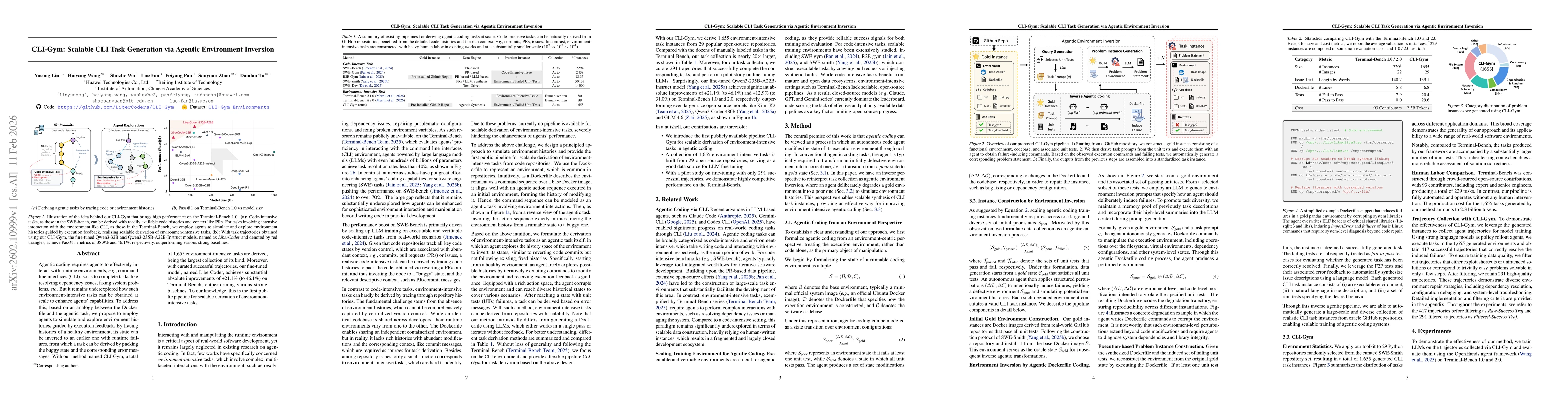

Agentic coding requires agents to effectively interact with runtime environments, e.g., command line interfaces (CLI), so as to complete tasks like resolving dependency issues, fixing system problems,...

Agents powered by large language models (LLMs) are increasingly adopted in the software industry, contributing code as collaborators or even autonomous developers. As their presence grows, it becomes ...

Large language model agents are increasingly envisioned as always-on personal assistants with access to anything relevant in the user's digital world. Yet current systems operate over only narrow slic...