Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the contextual dynamic pricing problem where a firm sells products to $T$ sequentially arriving consumers that behave according to an unknown demand model. The firm aims to maximize its rev...

We provide a new estimation method for conditional moment models via the martingale difference divergence (MDD).Our MDD-based estimation method is formed in the framework of a continuum of unconditi...

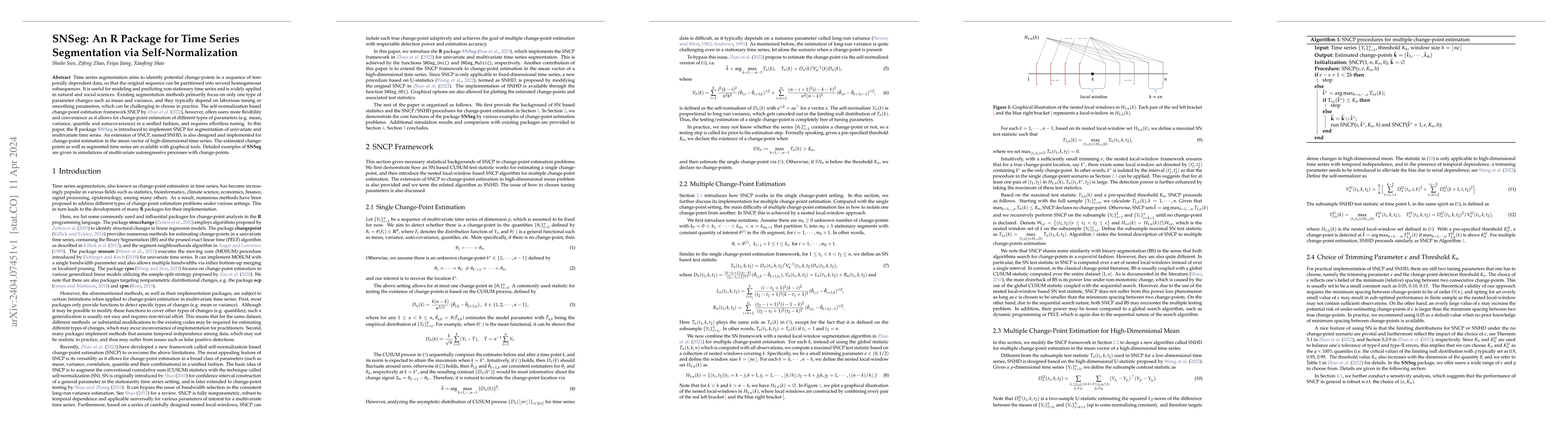

Time series segmentation aims to identify potential change-points in a sequence of temporally dependent data, so that the original sequence can be partitioned into several homogeneous subsequences. ...

In contemporary data analysis, it is increasingly common to work with non-stationary complex datasets. These datasets typically extend beyond the classical low-dimensional Euclidean space, making it...

Data objects taking value in a general metric space have become increasingly common in modern data analysis. In this paper, we study two important statistical inference problems, namely, two-sample ...

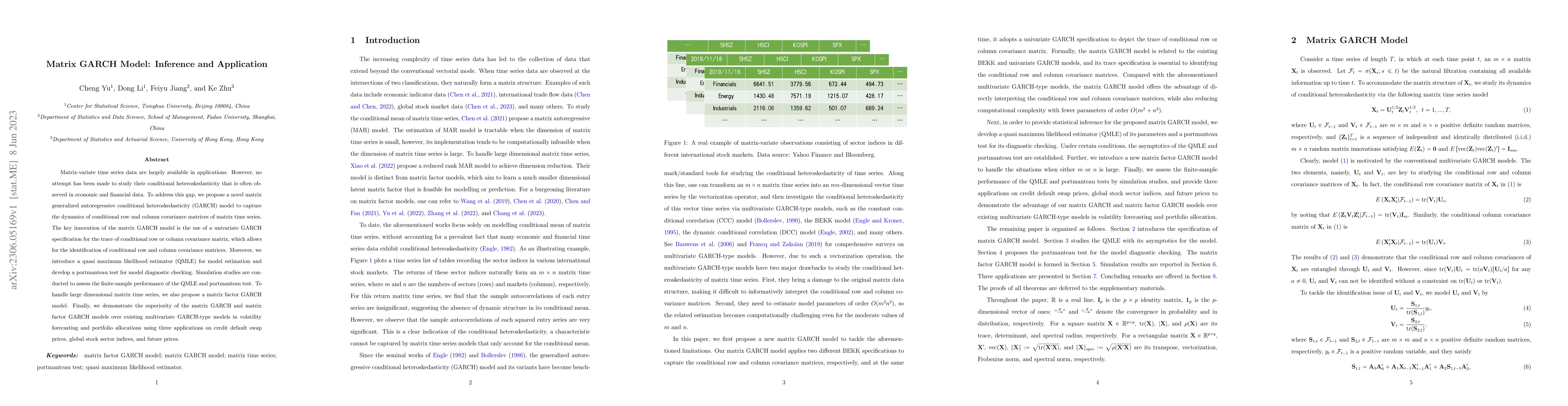

Matrix-variate time series data are largely available in applications. However, no attempt has been made to study their conditional heteroskedasticity that is often observed in economic and financia...

We consider a high-dimensional dynamic pricing problem under non-stationarity, where a firm sells products to $T$ sequentially arriving consumers that behave according to an unknown demand model wit...

We propose a novel method for testing serial independence of object-valued time series in metric spaces, which is more general than Euclidean or Hilbert spaces. The proposed method is fully nonparam...

This paper proposes a new test for a change point in the mean of high-dimensional data based on the spatial sign and self-normalization. The test is easy to implement with no tuning parameters, robu...

We propose a novel and unified framework for change-point estimation in multivariate time series. The proposed method is fully nonparametric, enjoys effortless tuning and is robust to temporal depen...

In this paper, we model the trajectory of the cumulative confirmed cases and deaths of COVID-19 (in log scale) via a piecewise linear trend model. The model naturally captures the phase transitions ...

Dynamic pricing strategies are crucial for firms to maximize revenue by adjusting prices based on market conditions and customer characteristics. However, designing optimal pricing strategies becomes ...

Motivated by privacy concerns in sequential decision-making on sensitive data, we address the challenge of nonparametric contextual multi-armed bandits (MAB) under local differential privacy (LDP). We...

Wasserstein autoregression provides a robust framework for modeling serial dependence among probability distributions, with wide-ranging applications in economics, finance, and climate science. In thi...

Residual-based goodness-of-fit tests for parametric time-series models are often complicated by parameter-estimation effects, which can alter the limiting behavior of diagnostic statistics. We propose...