Academic Profile

Statistics

Similar Authors

Papers on arXiv

Identification of market abuse is an extremely complicated activity that requires the analysis of large and complex datasets. We propose an unsupervised machine learning method for contextual anomal...

Identifying market abuse activity from data on investors' trading activity is very challenging both for the data volume and for the low signal to noise ratio. Here we propose two complementary unsup...

This paper investigates how Covid mobility restrictions impacted the population of investors of the Italian stock market. The analysis tracks the trading activity of individual investors in Italian ...

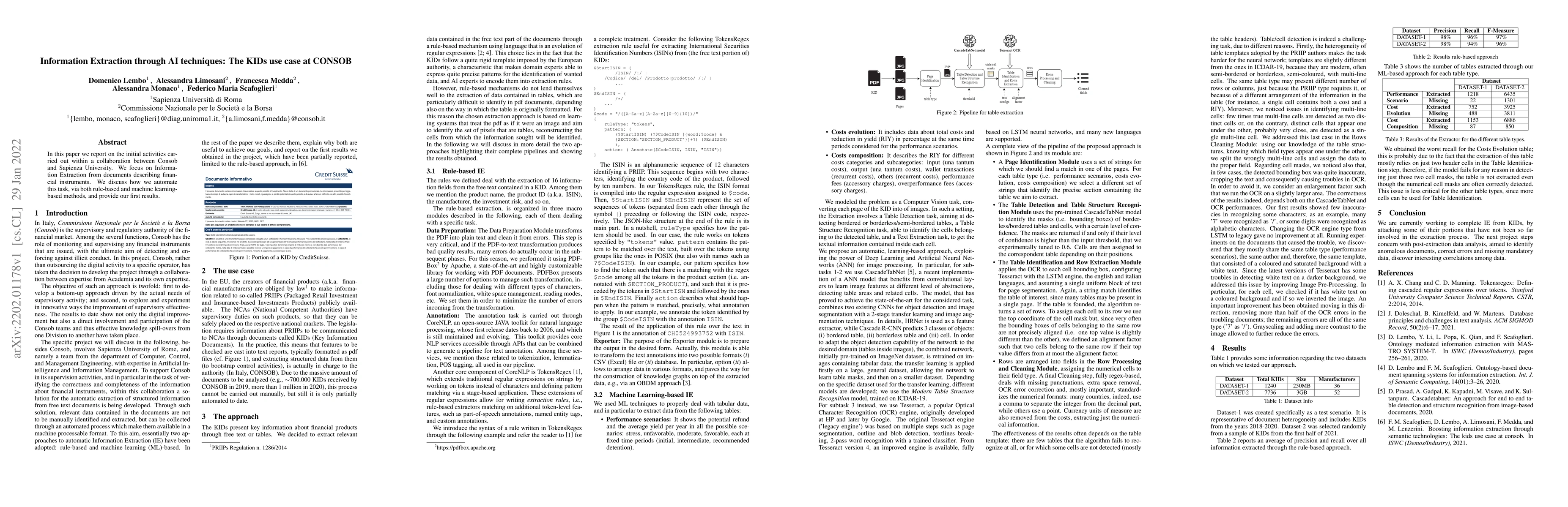

In this paper we report on the initial activities carried out within a collaboration between Consob and Sapienza University. We focus on Information Extraction from documents describing financial in...

Deep neural networks have gained momentum based on their accuracy, but their interpretability is often criticised. As a result, they are labelled as black boxes. In response, several methods have be...

In this paper, we introduce the Dynamic Modularity-Spectral Algorithm (DynMSA), a novel approach to identify clusters of stocks with high intra-cluster correlations and low inter-cluster correlations ...

Classical correlation matrices capture only linear and pairwise co-movements, leaving higher-order, nonlinear, and state-dependent interactions of financial markets unrepresented. This paper introduce...

Binary Shariah screens vary across standards and apply hard thresholds that create discontinuous classifications. We construct a Continuous Shariah Compliance Index (CSCI) in $[0,1]$ by mapping standa...

This paper re-examines the empirical Phillips curve (PC) model and its usefulness in the context of medium-term inflation forecasting. A latent variable Phillips curve hypothesis is formulated and tes...

Quantum computing is becoming strategically relevant to finance because several core financial bottlenecks are already defined by combinatorial search, expectation estimation, rare-event analysis, rep...