1

arXiv Papers

1

Total Publications

Profile

Academic Profile

Metrics

Statistics

1

arXiv Papers

1

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Bridging Econometrics and AI: VaR Estimation via Reinforcement Learning

and GARCH Models

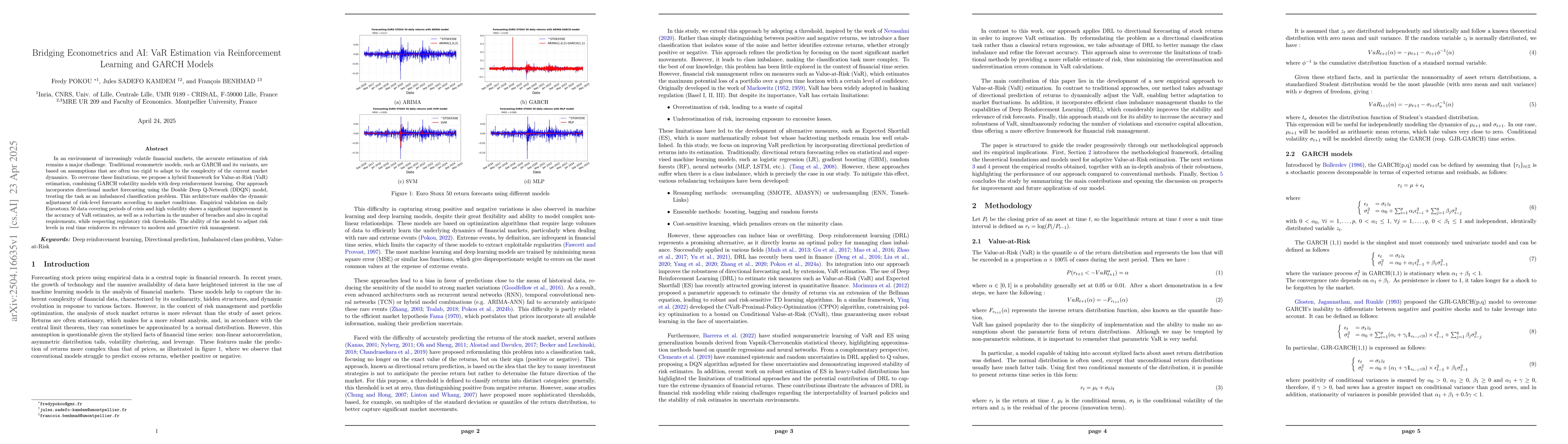

In an environment of increasingly volatile financial markets, the accurate estimation of risk remains a major challenge. Traditional econometric models, such as GARCH and its variants, are based on as...