Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper tackles the problem of mitigating catastrophic risk (which is risk with very low frequency but very high severity) in the context of a sequential decision making process. This problem is pa...

Dynamic hedging is the practice of periodically transacting financial instruments to offset the risk caused by an investment or a liability. Dynamic hedging optimization can be framed as a sequentia...

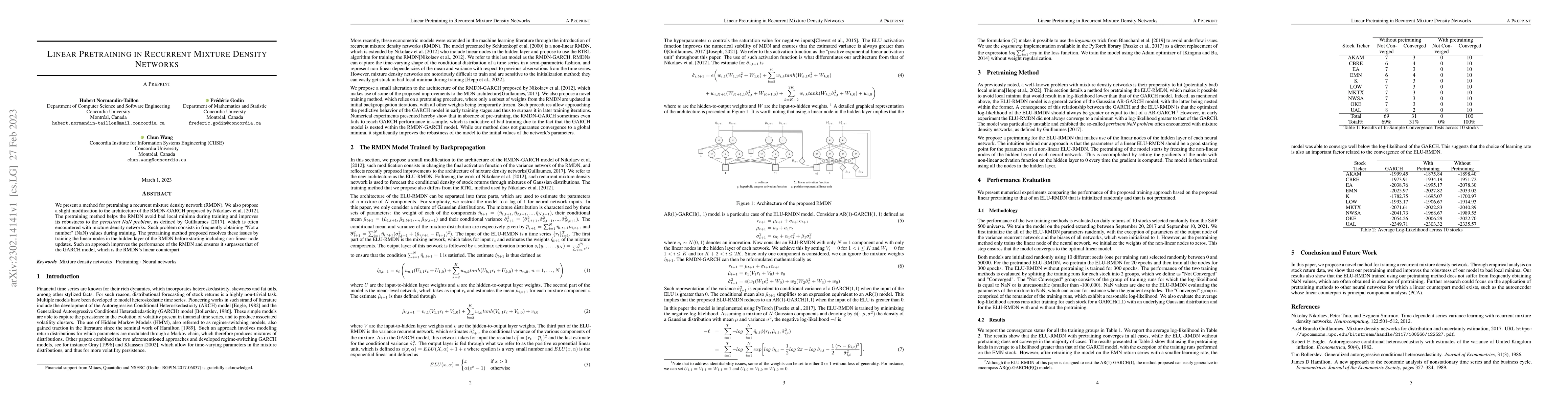

We present a method for pretraining a recurrent mixture density network (RMDN). We also propose a slight modification to the architecture of the RMDN-GARCH proposed by Nikolaev et al. [2012]. The pr...

This paper tackles the risk averse multi-armed bandits problem when incurred losses are non-stationary. The conditional value-at-risk (CVaR) is used as the objective function. Two estimation methods...

The use of non-translation invariant risk measures within the equal risk pricing (ERP) methodology for the valuation of financial derivatives is investigated. The ability to move beyond the class of...

The conditional value-at-risk (CVaR) is a useful risk measure in fields such as machine learning, finance, insurance, energy, etc. When measuring very extreme risk, the commonly used CVaR estimation...

This paper studies the equal risk pricing (ERP) framework for the valuation of European financial derivatives. This option pricing approach is consistent with global trading strategies by setting th...

We propose a stochastic model allowing property and casualty insurers with multiple business lines to measure their liabilities for incurred claims risk and calculate associated capital requirements...

This article presents a deep reinforcement learning approach to price and hedge financial derivatives. This approach extends the work of Guo and Zhu (2017) who recently introduced the equal risk pri...

We present a dynamic hedging scheme for S&P 500 options, where rebalancing decisions are enhanced by integrating information about the implied volatility surface dynamics. The optimal hedging strategy...

The recent work of Horikawa and Nakagawa (2024) claims that under a complete market admitting statistical arbitrage, the difference between the hedging position provided by deep hedging and that of th...

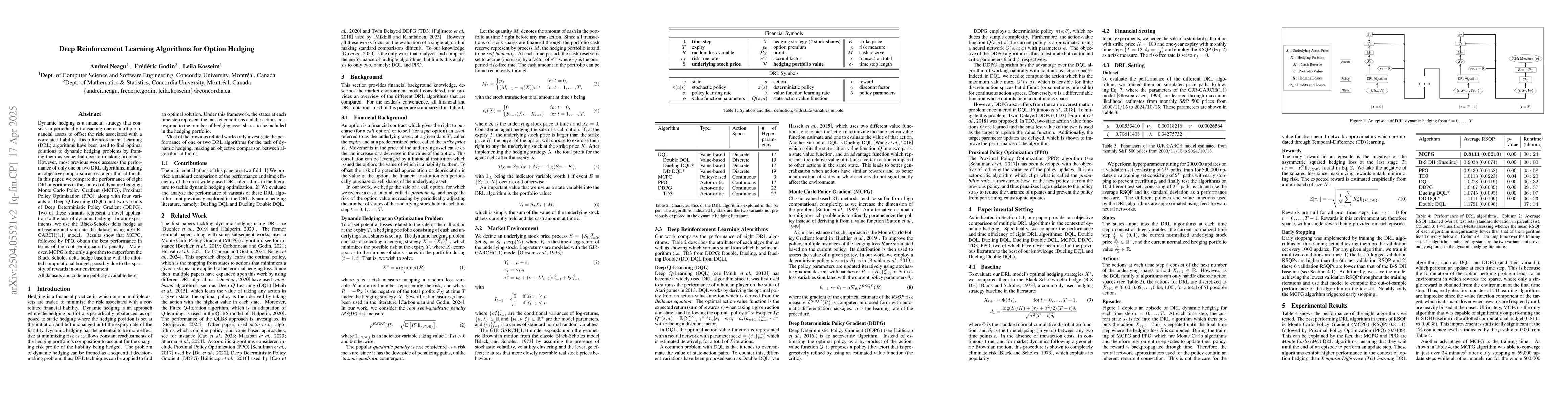

Dynamic hedging is a financial strategy that consists in periodically transacting one or multiple financial assets to offset the risk associated with a correlated liability. Deep Reinforcement Learnin...

We propose an enhanced deep hedging framework for index option portfolios, grounded in a realistic market simulator that captures the joint dynamics of S&P 500 returns and the full implied volatility ...

This paper investigates the deep hedging framework, based on reinforcement learning (RL), for the dynamic hedging of swaptions, contrasting its performance with traditional sensitivity-based rho-hedgi...