Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a general model for the balance-sheet consistent valuation of interbank claims within an interconnected financial system. Our model represents an extension of clearing models of interde...

We introduce a new numerical approximation method for functionals of factor credit portfolio models based on the theory of mod-$\phi$ convergence and mod-$\phi$ approximation schemes. The method can...

In this article, we provide an extension of the Chen-Stein inequality for Poisson approximation in the total variation distance for sums of independent Bernoulli random variables in two ways. We pro...

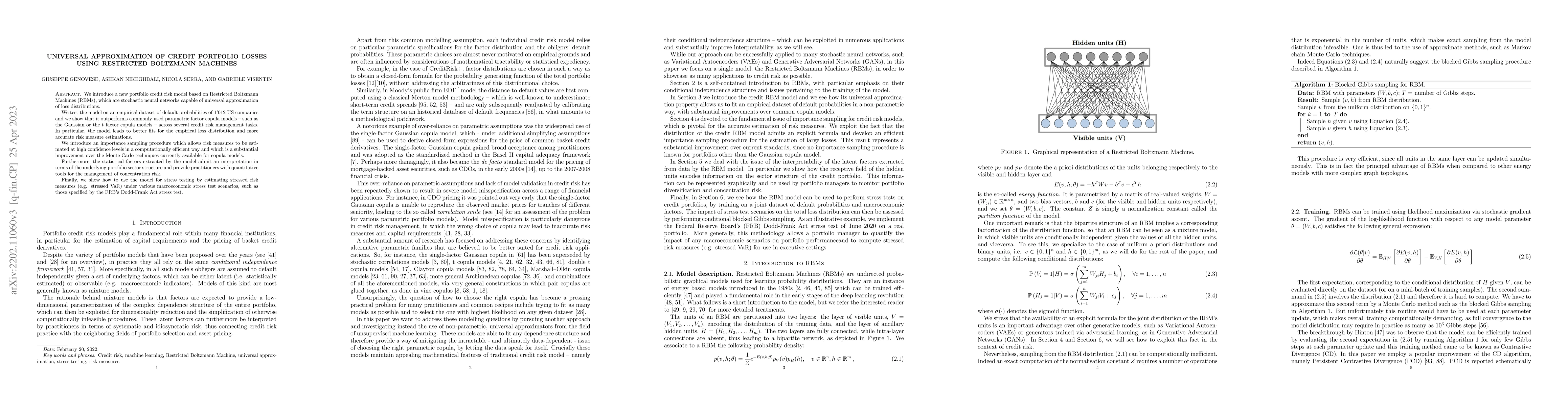

We introduce a new portfolio credit risk model based on Restricted Boltzmann Machines (RBMs), which are stochastic neural networks capable of universal approximation of loss distributions. We test t...

In classical contagion models, default systems are Markovian conditionally on the observation of their stochastic environment, with interacting intensities. This necessitates that the environment ev...

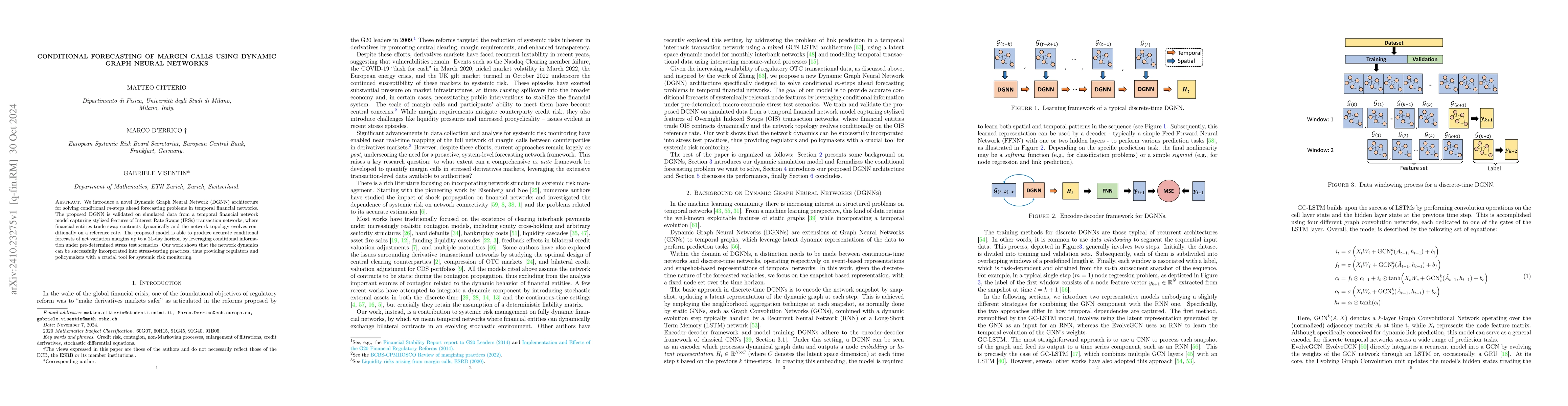

We introduce a novel Dynamic Graph Neural Network (DGNN) architecture for solving conditional $m$-steps ahead forecasting problems in temporal financial networks. The proposed DGNN is validated on sim...

We present a novel method for efficiently computing optimal transport maps and Wasserstein barycenters in high-dimensional spaces. Our approach uses conditional normalizing flows to approximate the in...

In this paper, we show that interventionally robust optimization problems in causal models are continuous under the $G$-causal Wasserstein distance, but may be discontinuous under the standard Wassers...