Academic Profile

Statistics

Similar Authors

Papers on arXiv

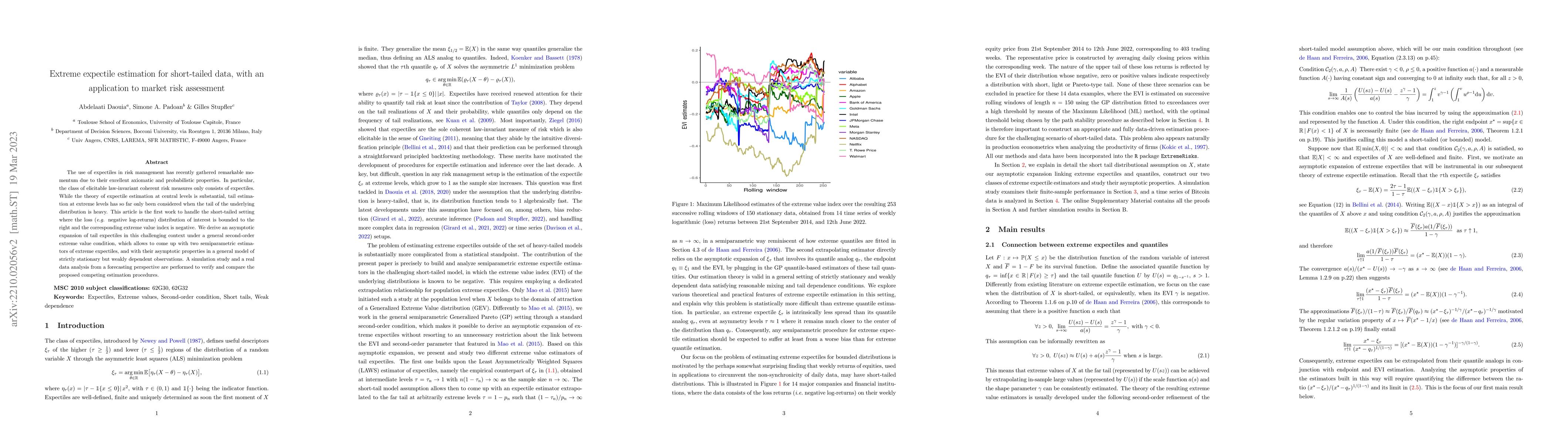

The use of expectiles in risk management has recently gathered remarkable momentum due to their excellent axiomatic and probabilistic properties. In particular, the class of elicitable law-invariant...

This paper investigates pooling strategies for tail index and extreme quantile estimation from heavy-tailed data. To fully exploit the information contained in several samples, we present general we...

The Value-at-Risk (VaR) is a widely used instrument in financial risk management. The question of estimating the VaR of loss return distributions at extreme levels is an important question in financ...

The notion of expectiles, originally introduced in the context of testing for homoscedasticity and conditional symmetry of the error distribution in linear regression, induces a law-invariant, coher...

Expectiles define the only law-invariant, coherent and elicitable risk measure apart from the expectation. The popularity of expectile-based risk measures is steadily growing and their properties ha...

We study a general risk measure called the generalized shortfall risk measure, which was first introduced in Mao and Cai (2018). It is proposed under the rank-dependent expected utility framework, or ...

Sufficient dimension reduction has received much interest over the past 30 years. Most existing approaches focus on statistical models linking the response to the covariate through a regression equati...

Over the last 30 years, extensive work has been devoted to developing central limit theory for partial sums of subordinated long memory linear time series. A much less studied problem, motivated by qu...

Synthetic oversampling of minority examples using SMOTE and its variants is a leading strategy for addressing imbalanced classification problems. Despite the success of this approach in practice, its ...

Geometric quantiles are popular location functionals to build rank-based statistical procedures in multivariate settings. They are obtained through the minimization of a non-smooth convex objective fu...