Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a new theoretical framework that exploits convolution kernels to transform a Volterra path-dependent (non-Markovian) stochastic process into a standard (Markovian) diffusion process. This...

We investigate the optimal reinsurance problem when the loss process exhibits jump clustering features and the insurance company has restricted information about the loss process. We maximize expect...

We propose a model where a producer and a consumer can affect the price dynamics of some commodity controlling drift and volatility of, respectively, the production rate and the consumption rate. We...

We propose a quantization-based numerical scheme for a family of decoupled FBSDEs. We simplify the scheme for the control in Pag\`es and Sagna (2018) so that our approach is fully based on recursive...

We develop a product functional quantization of rough volatility. Since the quantizers can be computed offline, this new technique, built on the insightful works by Luschgy and Pages, becomes a stro...

We propose and investigate two model classes for forward power price dynamics, based on continuous branching processes with immigration, and on Hawkes processes with exponential kernel, respectively...

We design three continuous--time models in finite horizon of a commodity price, whose dynamics can be affected by the actions of a representative risk--neutral producer and a representative risk--ne...

Quantization algorithms have been successfully adopted to option pricing in finance thanks to the high convergence rate of the numerical approximation. In particular, very recently, recursive margin...

We frame dynamic persuasion in a partial observation stochastic control Leader-Follower game with an ergodic criterion. The Receiver controls the dynamics of a multidimensional unobserved state proces...

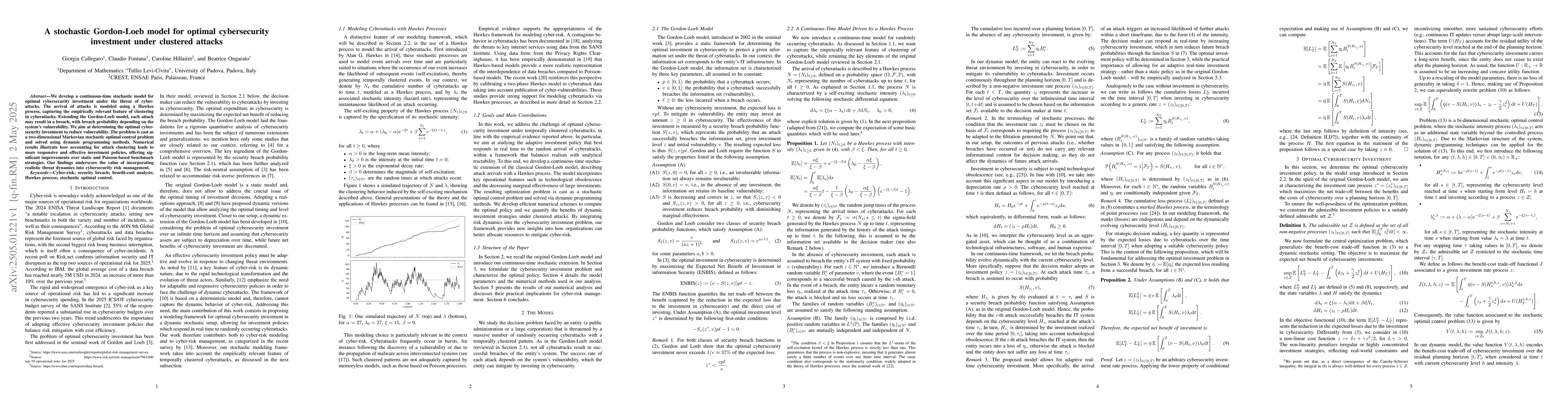

We develop a continuous-time stochastic model for optimal cybersecurity investment under the threat of cyberattacks. The arrival of attacks is modeled using a Hawkes process, capturing the empirically...