Academic Profile

Statistics

Similar Authors

Papers on arXiv

We address the curse of dimensionality in dynamic covariance estimation by modeling the underlying co-volatility dynamics of a time series vector through latent time-varying stochastic factors. The ...

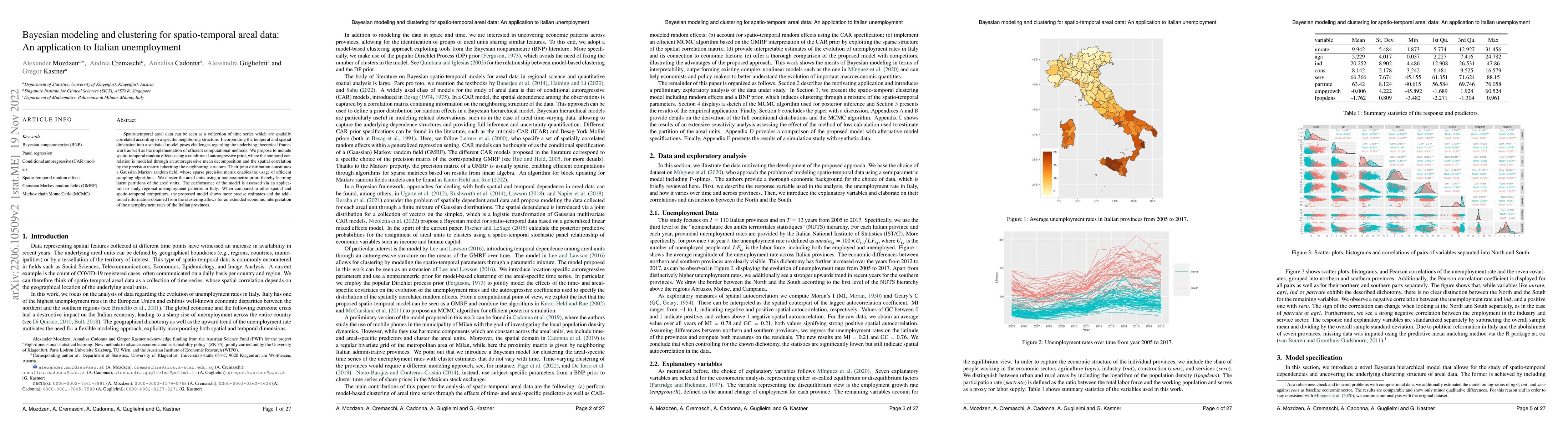

Spatio-temporal areal data can be seen as a collection of time series which are spatially correlated according to a specific neighboring structure. Incorporating the temporal and spatial dimension i...

Vectorautogressions (VARs) are widely applied when it comes to modeling and forecasting macroeconomic variables. In high dimensions, however, they are prone to overfitting. Bayesian methods, more co...

We propose an interdisciplinary framework that combines Bayesian predictive inference, a well-established tool in Machine Learning, with Formal Methods rooted in the computer science community. Baye...

The present study investigates the price (co)volatility of four dairy commodities -- skim milk powder, whole milk powder, butter and cheddar cheese -- in three major dairy markets. It uses a multiva...

The R package stochvol provides a fully Bayesian implementation of heteroskedasticity modeling within the framework of stochastic volatility. It utilizes Markov chain Monte Carlo (MCMC) samplers to ...

Stochastic volatility (SV) models are nonlinear state-space models that enjoy increasing popularity for fitting and predicting heteroskedastic time series. However, due to the large number of latent...

We forecast S&P 500 excess returns using a flexible Bayesian econometric state space model with non-Gaussian features at several levels. More precisely, we control for overparameterization via novel...

We assess the relationship between model size and complexity in the time-varying parameter VAR framework via thorough predictive exercises for the Euro Area, the United Kingdom and the United States...

We develop a Bayesian vector autoregressive (VAR) model with multivariate stochastic volatility that is capable of handling vast dimensional information sets. Three features are introduced to permit...

The global climate has underscored the need for effective policies to reduce greenhouse gas emissions from all sources, including those resulting from agricultural expansion, which is regulated by the...

Bhattacharya et al. (2015, Journal of the American Statistical Association 110(512): 1479-1490) introduce a novel prior, the Dirichlet-Laplace (DL) prior, and propose a Markov chain Monte Carlo (MCMC)...

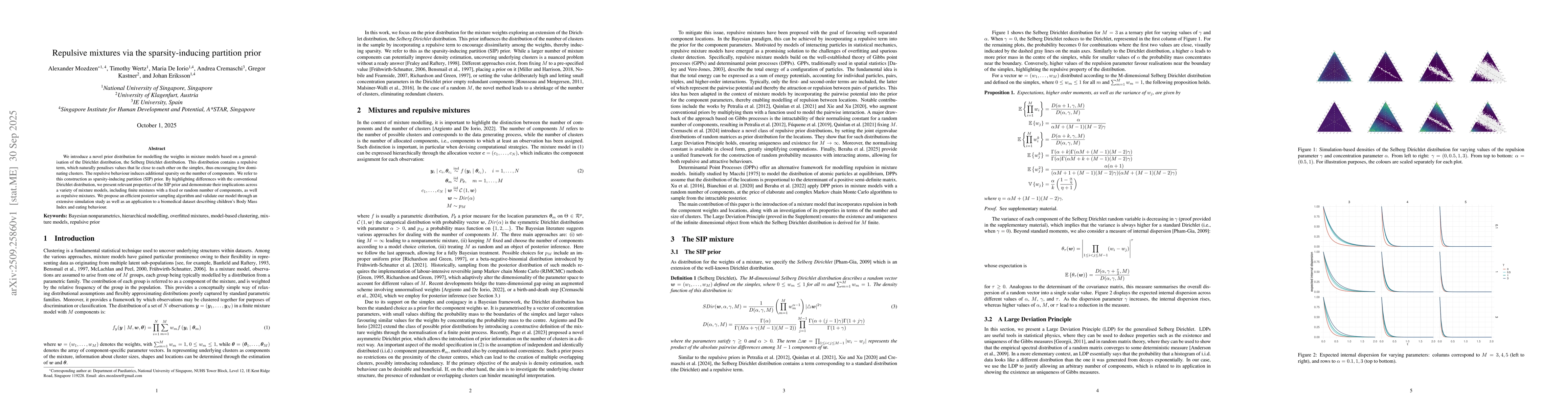

We introduce a novel prior distribution for modelling the weights in mixture models based on a generalisation of the Dirichlet distribution, the Selberg Dirichlet distribution. This distribution conta...