Academic Profile

Statistics

Similar Authors

Papers on arXiv

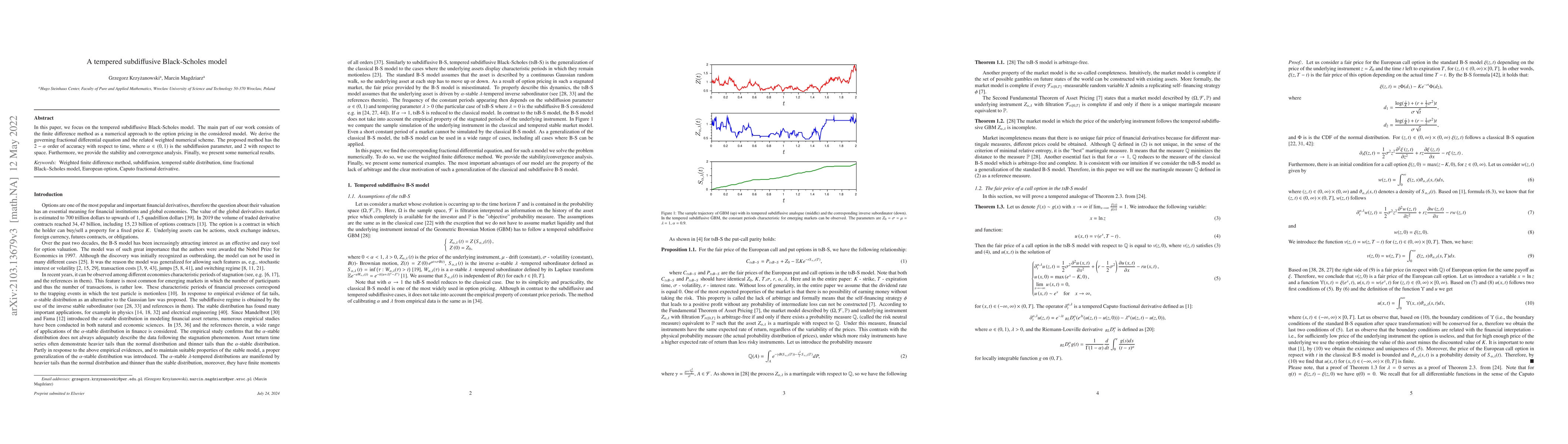

In this paper, we focus on the tempered subdiffusive Black-Scholes model. The main part of our work consists of the finite difference method as a numerical approach to the option pricing in the cons...

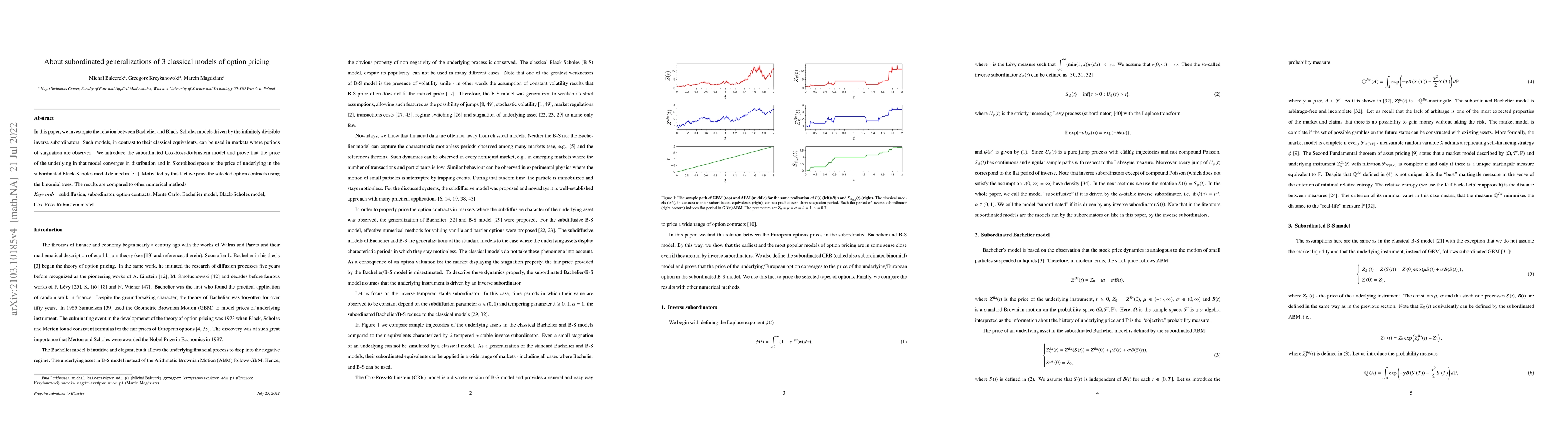

In this paper, we investigate the relation between Bachelier and Black-Scholes models driven by the infinitely divisible inverse subordinators. Such models, in contrast to their classical equivalent...

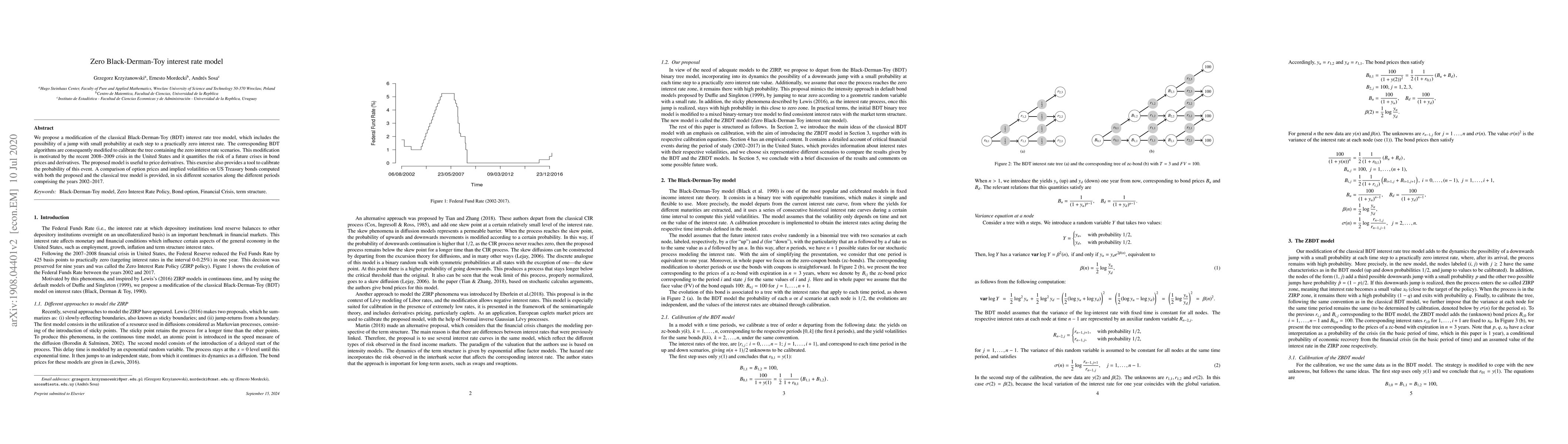

We propose a modification of the classical Black-Derman-Toy (BDT) interest rate tree model, which includes the possibility of a jump with small probability at each step to a practically zero interes...

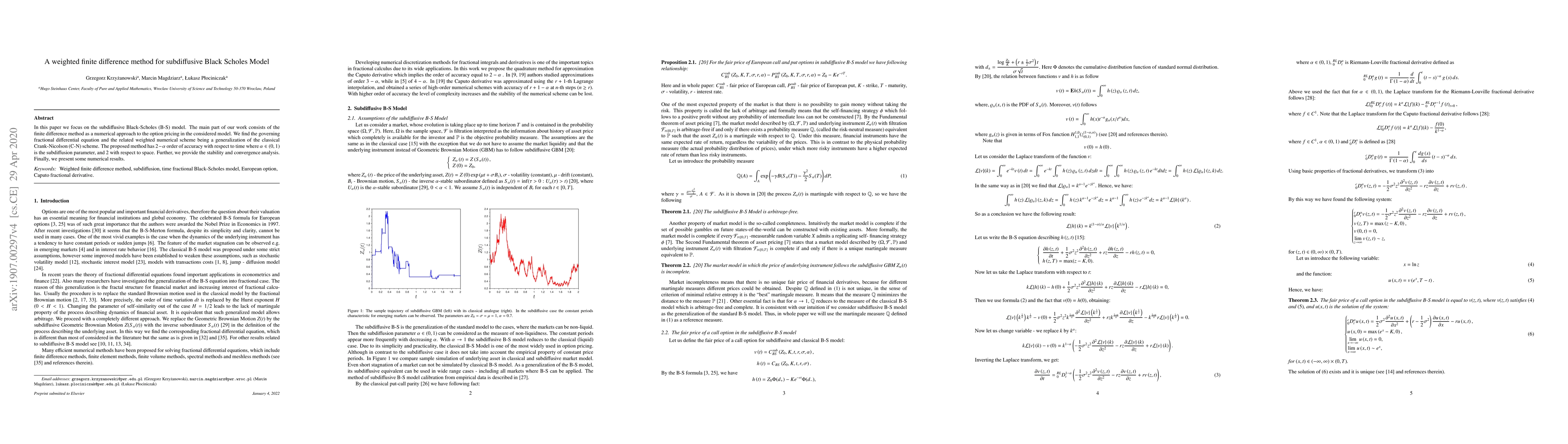

In this paper we focus on the subdiffusive Black Scholes model. The main part of our work consists of the finite difference method as a numerical approach to the option pricing in the considered mod...