About subordinated generalizations of 3 classical models of option pricing

Publication

Metrics

AI Quick Summary

This paper explores the relationship between Bachelier and Black-Scholes models driven by inverse subordinators, introducing a subordinated Cox-Ross-Rubinstein model that accommodates market stagnation periods. It demonstrates the convergence of the underlying price in this model to the subordinated Black-Scholes model, and compares option pricing using binomial trees to other numerical methods.

Paper Preview

Abstract

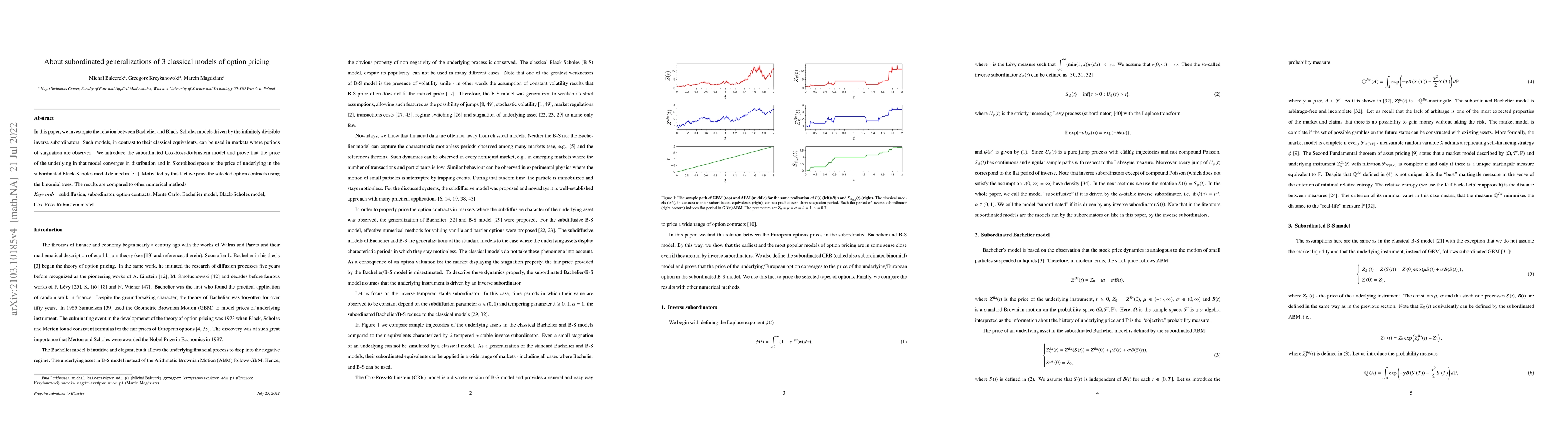

In this paper, we investigate the relation between Bachelier and Black-Scholes models driven by the infinitely divisible inverse subordinators. Such models, in contrast to their classical equivalents, can be used in markets where periods of stagnation are observed. We introduce the subordinated Cox-Ross-Rubinstein model and prove that the price of the underlying in that model converges in distribution and in Skorokhod space to the price of underlying in the subordinated Black-Scholes model defined in [31]. Motivated by this fact we price the selected option contracts using the binomial trees. The results are compared to other numerical methods.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0