Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper we introduce a general stochastic representation for an important class of processes with resetting. It allows to describe any stochastic process intermittently terminated and restarte...

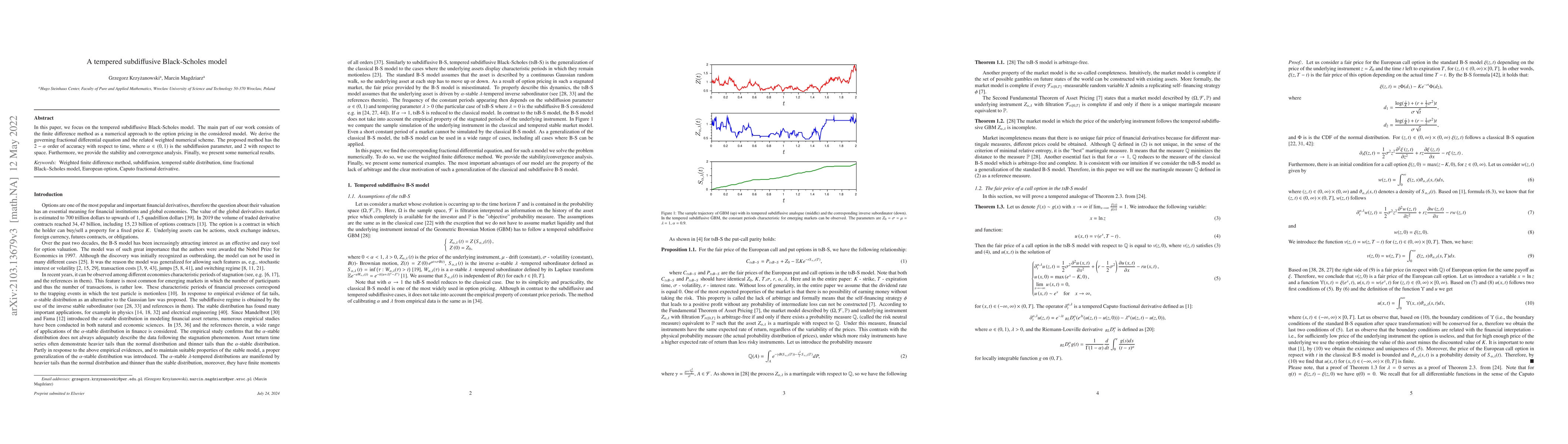

In this paper, we focus on the tempered subdiffusive Black-Scholes model. The main part of our work consists of the finite difference method as a numerical approach to the option pricing in the cons...

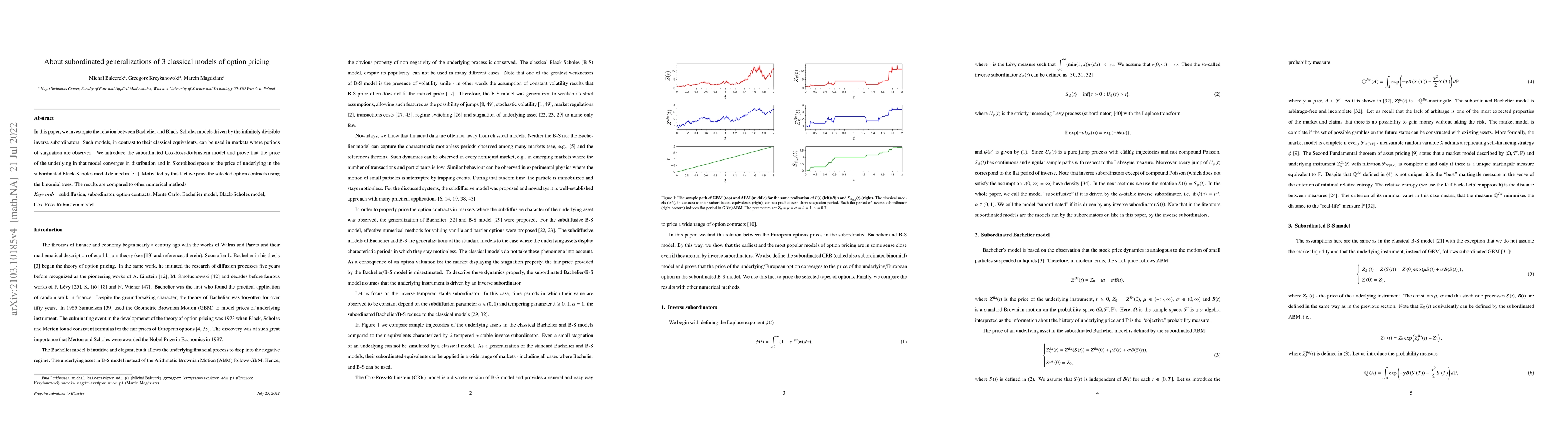

In this paper, we investigate the relation between Bachelier and Black-Scholes models driven by the infinitely divisible inverse subordinators. Such models, in contrast to their classical equivalent...

We investigate the first-passage dynamics of symmetric and asymmetric L\'evy flights in a semi-infinite and bounded intervals. By solving the space-fractional diffusion equation, we analyse the frac...

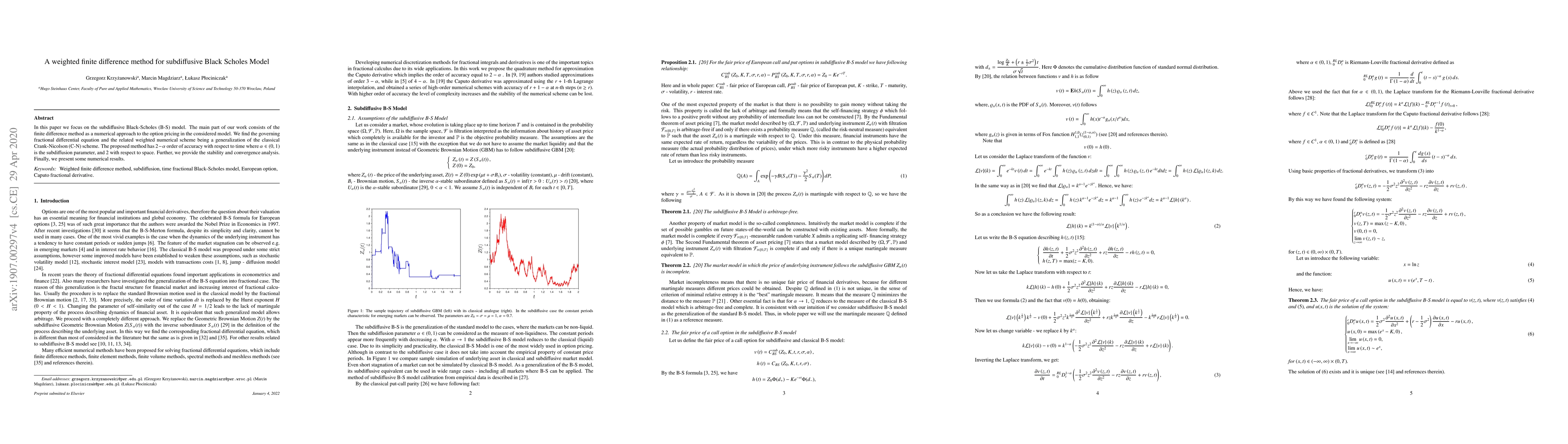

In this paper we focus on the subdiffusive Black Scholes model. The main part of our work consists of the finite difference method as a numerical approach to the option pricing in the considered mod...

We show that the codifference is a useful tool in studying the ergodicity breaking and non-Gaussianity properties of stochastic time series. While the codifference is a measure of dependence that wa...

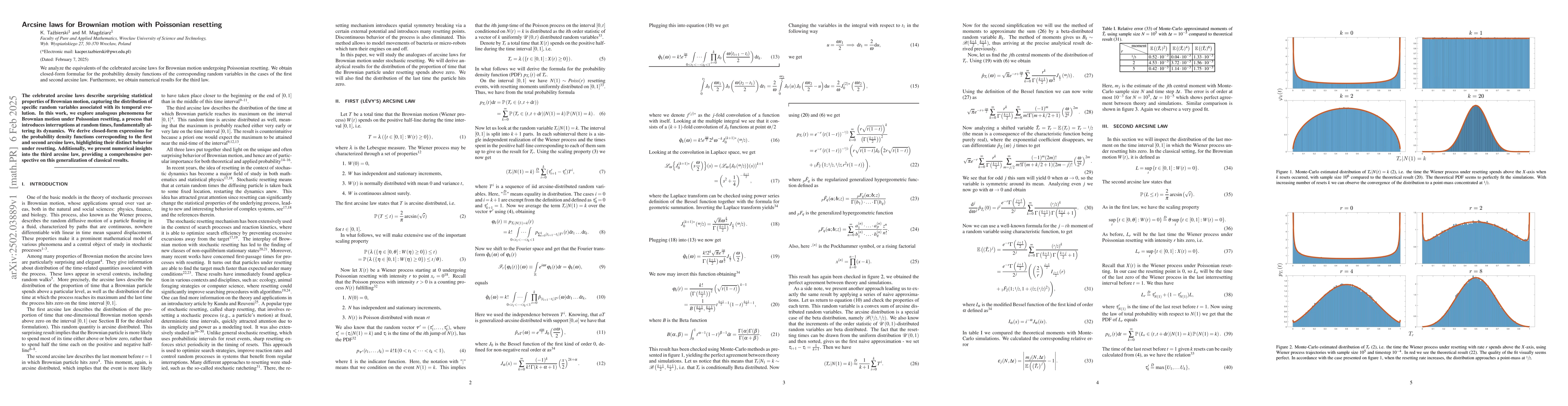

We analyze the equivalents of the celebrated arcsine laws for Brownian motion undergoing Poissonian resetting. We obtain closed-form formulae for the probability density functions of the corresponding...

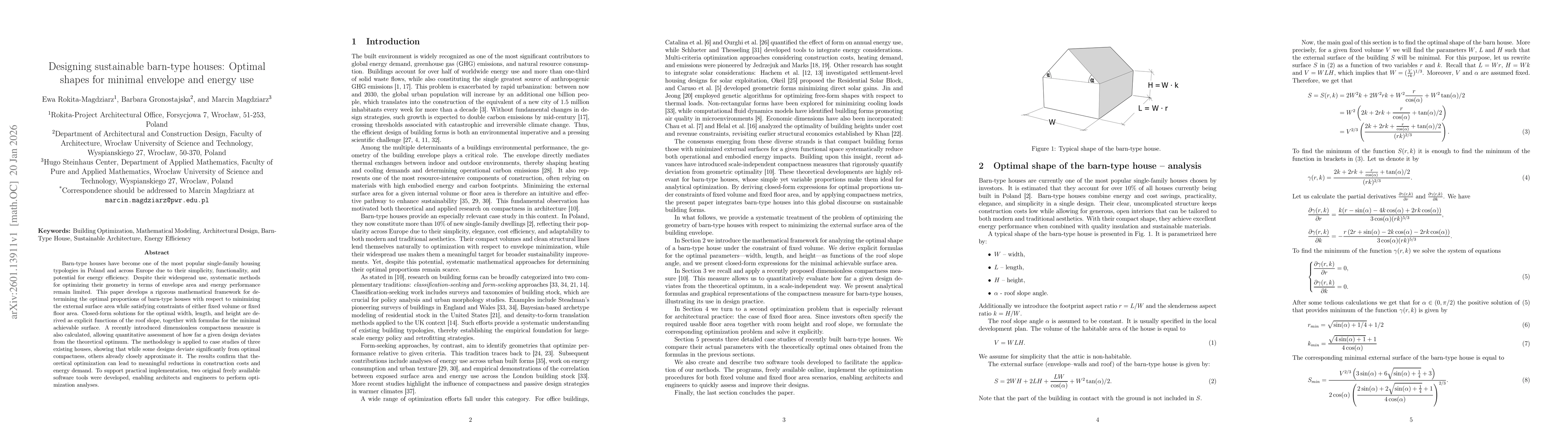

Barn-type houses have become one of the most popular single-family housing typologies in Poland and across Europe due to their simplicity, functionality, and potential for energy efficiency. Despite t...

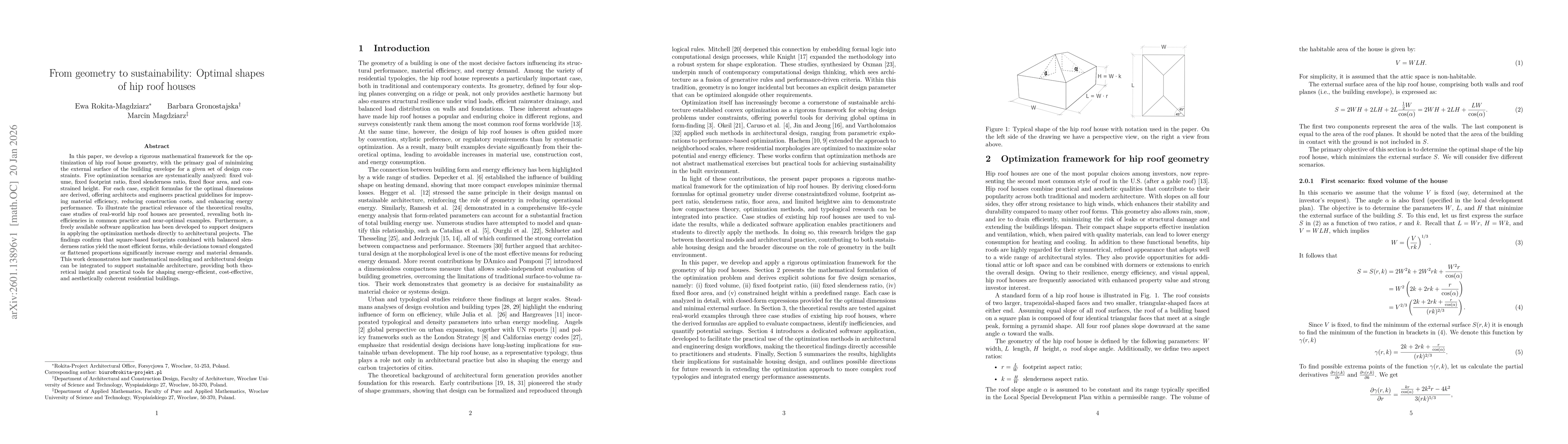

In this paper, we develop a rigorous mathematical framework for the optimization of hip roof house geometry, with the primary goal of minimizing the external surface of the building envelope for a giv...

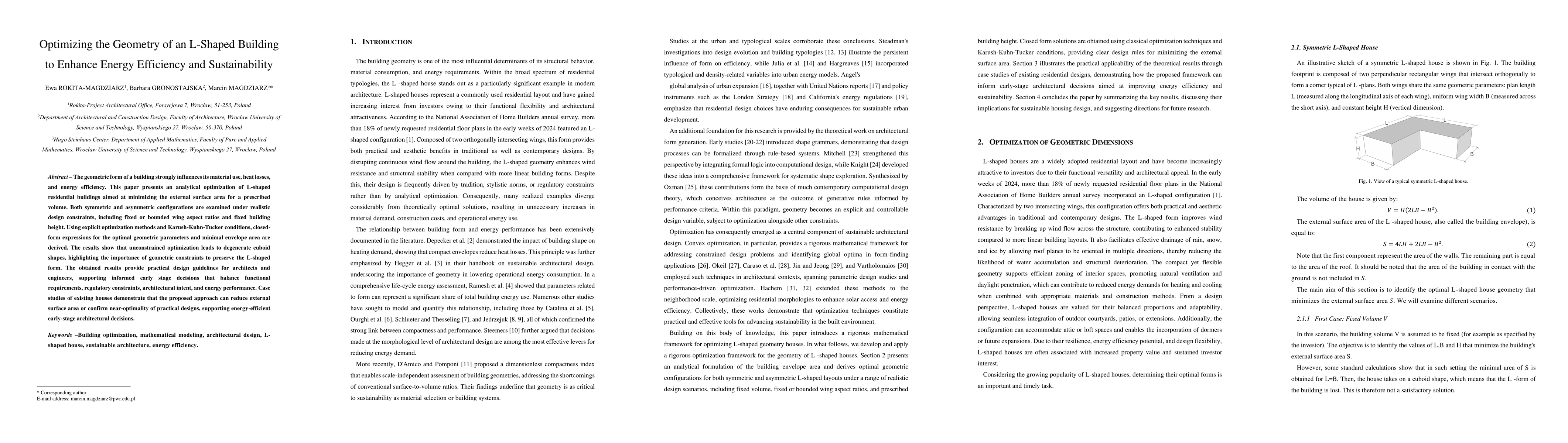

The geometric form of a building strongly influences its material use, heat losses, and energy efficiency. This paper presents an analytical optimization of L-shaped residential buildings aimed at min...