Academic Profile

Statistics

Similar Authors

Papers on arXiv

This article studies inverse reinforcement learning (IRL) for the stochastic linear-quadratic optimal control problem, where two agents are considered. A learner agent does not know the expert agent...

With the outstanding performance of policy gradient (PG) method in the reinforcement learning field, the convergence theory of it has aroused more and more interest recently. Meanwhile, the signific...

In this article, we study a continuous-time stochastic $H_\infty$ control problem based on reinforcement learning (RL) techniques that can be viewed as solving a stochastic linear-quadratic two-pers...

We give an axiomatic framework for conditional generalized deviation measures. Under financially reasonable assumptions, we give the correspondence between conditional coherent risk measures and gen...

In this paper, we study general monetary risk measures (without any convexity or weak convexity). A monetary (respectively, positively homogeneous) risk measure can be characterized as the lower env...

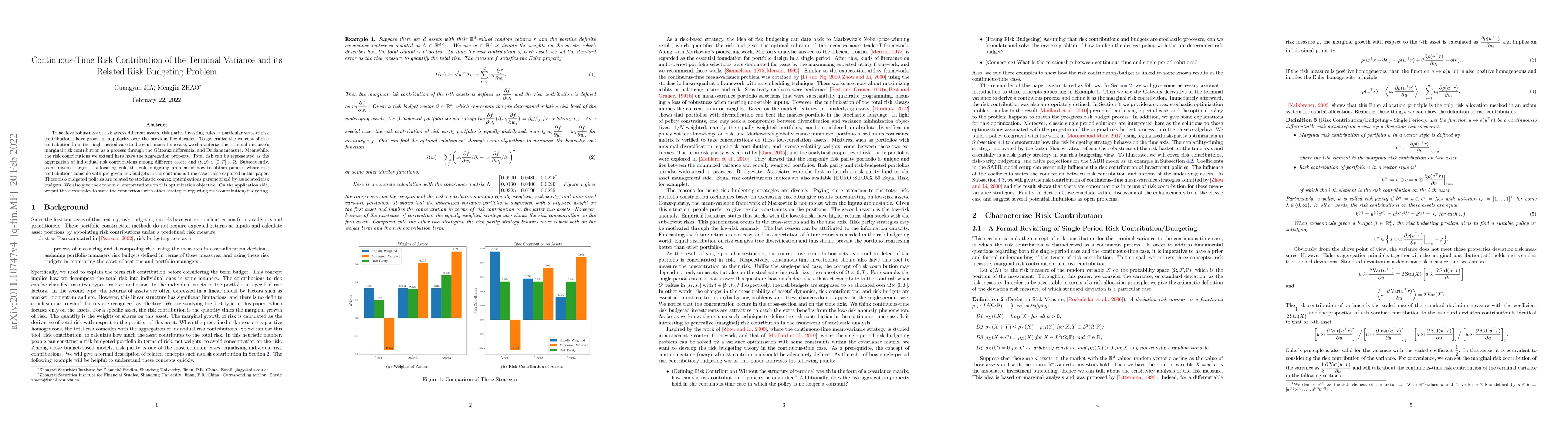

To achieve robustness of risk across different assets, risk parity investing rules, a particular state of risk contributions, have grown in popularity over the previous few decades. To generalize th...

We investigate a class of quadratic backward stochastic differential equations (BSDEs) with generators singular in $ y $. First, we establish the existence of solutions and a comparison theorem, there...

This paper investigate a class of multi-dimensional backward stochastic differential equations (BSDEs) with singualr generators exhibiting diagonally quadratic growth and unbounded terminal conditions...

In recent years, stabilizing unknown dynamical systems has became a critical problem in control systems engineering. Addressing this for linear time-invariant (LTI) systems is an essential fist step t...

This paper proposes a new second-order symmetric algorithm for solving decoupled forward-backward stochastic differential equations. Inspired by the alternating direction implicit splitting method for...

In this paper, we study the convergence rate between reflected backward stochastic differential equations with quadratic generators and their penalized BSDEs. Using techniques of BMO martingales, we p...