Academic Profile

Statistics

Similar Authors

Papers on arXiv

Change of numeraire is a classical tool in mathematical finance. Campi-Laachir-Martini established its applicability to martingale optimal transport. We note that the results of Campi-Laachir-Martin...

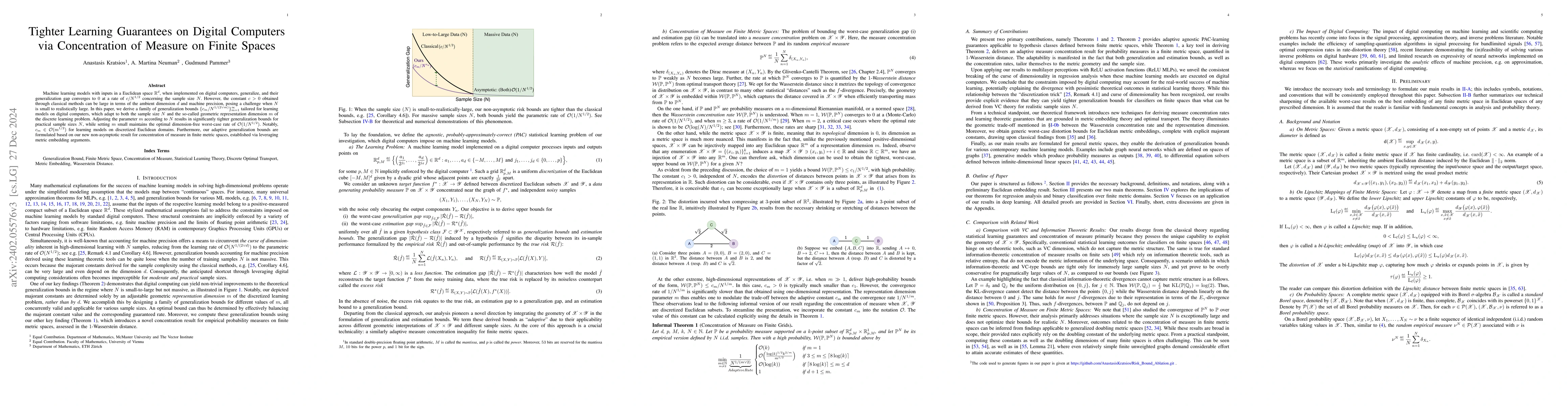

Machine learning models with inputs in a Euclidean space $\mathbb{R}^d$, when implemented on digital computers, generalize, and their {\it generalization gap} converges to $0$ at a rate of $c/N^{1/2...

Given a collection of probability measures, a practitioner sometimes needs to find an "average" distribution which adequately aggregates reference distributions. A theoretically appealing notion of ...

We introduce a multivariate version of adapted transport, which we name multicausal transport, involving several filtered processes among which causality constraints are imposed. Subsequently, we co...

We investigate duality and existence of dual optimizers for several adapted optimal transport problems under minimal assumptions. This includes the causal and bicausal transport, the barycenter prob...

Random variables $X^i$, $i=1,2$ are 'probabilistically equivalent' if they have the same law. Moreover, in any class of equivalent random variables it is easy to select canonical representatives. ...

A basic and natural coupling between two probabilities on $\mathbb R^N$ is given by the Knothe-Rosenblatt coupling. It represents a multiperiod extension of the quantile coupling and is simple to ca...

The Bass local volatility model introduced by Backhoff-Veraguas--Beiglb\"ock--Huesmann--K\"allblad is a Markov model perfectly calibrated to vanilla options at finitely many maturities, that approxi...

Optimal transport (OT) barycenters are a mathematically grounded way of averaging probability distributions while capturing their geometric properties. In short, the barycenter task is to take the a...

While many questions in robust finance can be posed in the martingale optimal transport framework or its weak extension, others like the subreplication price of VIX futures, the robust pricing of Am...

Adapted or causal transport theory aims to extend classical optimal transport from probability measures to stochastic processes. On a technical level, the novelty is to restrict to couplings which a...

We present a multidimensional extension of Kellerer's theorem on the existence of mimicking Markov martingales for peacocks, a term derived from the French for stochastic processes increasing in con...

In this paper we provide a quantitative analysis to the concept of arbitrage, that allows to deal with model uncertainty without imposing the no-arbitrage condition. In markets that admit ``small ar...

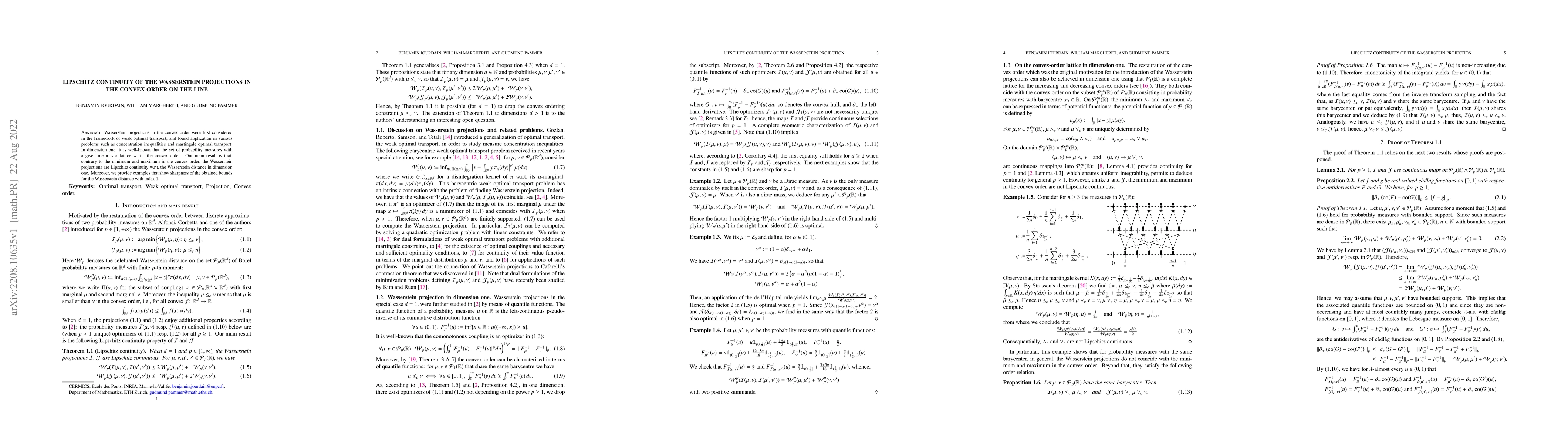

Wasserstein projections in the convex order were first considered in the framework of weak optimal transport, and found application in various problems such as concentration inequalities and marting...

We provide a short proof of the intriguing characterisation of the convex order given by Wiesel and Zhang.

The adapted weak topology is an extension of the weak topology for stochastic processes designed to adequately capture properties of underlying filtrations. With the recent work of Bart--Beiglb\"ock...

Adapted optimal transport (AOT) problems are optimal transport problems for distributions of a time series where couplings are constrained to have a temporal causal structure. In this paper, we deve...

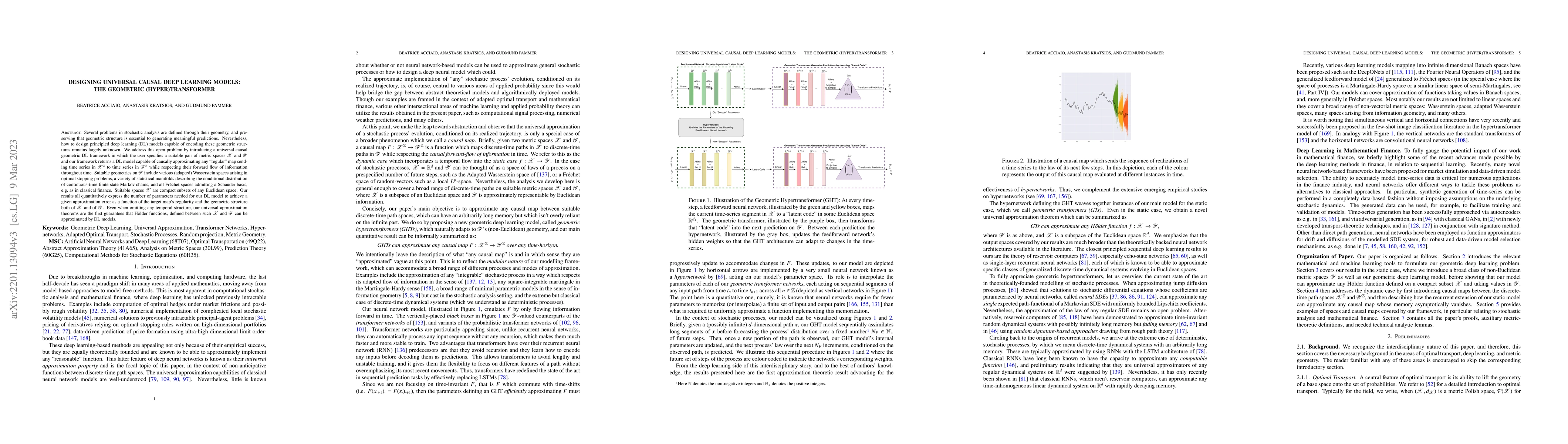

Several problems in stochastic analysis are defined through their geometry, and preserving that geometric structure is essential to generating meaningful predictions. Nevertheless, how to design pri...

Hamza-Klebaner posed the problem of constructing martingales with Brownian marginals that differ from Brownian motion, so called fake Brownian motions. Besides its theoretical appeal, the problem re...

While many questions in (robust) finance can be posed in the martingale optimal transport (MOT) framework, others require to consider also non-linear cost functionals. Following the terminology of G...

Famously mathematical finance was started by Bachelier in his 1900 PhD thesis where - among many other achievements - he also provides a formal derivation of the Kolmogorov forward equation. This fo...

Wasserstein distance induces a natural Riemannian structure for the probabilities on the Euclidean space. This insight of classical transport theory is fundamental for tremendous applications in var...

Our main result is to establish stability of martingale couplings: suppose that $\pi$ is a martingale coupling with marginals $\mu, \nu$. Then, given approximating marginal measures $\tilde \mu \app...

We consider a model-independent pricing problem in a fixed-income market and show that it leads to a weak optimal transport problem as introduced by Gozlan et al. We use this to characterize the ext...

Motivated by applications to geometric inequalities, Gozlan, Roberto, Samson, and Tetali introduced a transport problem for `weak' cost functionals. Basic results of optimal transport theory can be ...

Under mild regularity assumptions, the transport problem is stable in the following sense: if a sequence of optimal transport plans $\pi_1, \pi_2, \ldots$ converges weakly to a transport plan $\pi$,...

The optimal weak transport problem has recently been introduced by Gozlan et.\ al. We provide general existence and duality results for these problems on arbitrary Polish spaces, as well as a necess...

Given $\mu$ and $\nu$, probability measures on $\mathbb R^d$ in convex order, a Bass martingale is arguably the most natural martingale starting with law $\mu$ and finishing with law $\nu$. Indeed, th...

The adapted Wasserstein distance is a metric for quantifying distributional uncertainty and assessing the sensitivity of stochastic optimization problems on time series data. A computationally efficie...

Researchers from different areas have independently defined extensions of the usual weak convergence of laws of stochastic processes with the goal of adequately accounting for the flow of information....

The fundamental theorem of classical optimal transport establishes strong duality and characterizes optimizers through a complementary slackness condition. Milestones such as Brenier's theorem and the...

The adapted Wasserstein ($AW$) distance refines the classical Wasserstein ($W$) distance by incorporating the temporal structure of stochastic processes. This makes the $AW$-distance well-suited as a ...

We study absolutely continuous curves in the adapted Wasserstein space of filtered processes. We provide a probabilistic representation of such curves as flows of adapted processes on a common filtere...

Brenier's fundamental theorem characterizes optimal transport plans for measures $\mu, \nu$ on $\mathbb{R}^d$ and quadratic distance costs in terms of gradients of convex functions. In particular it g...

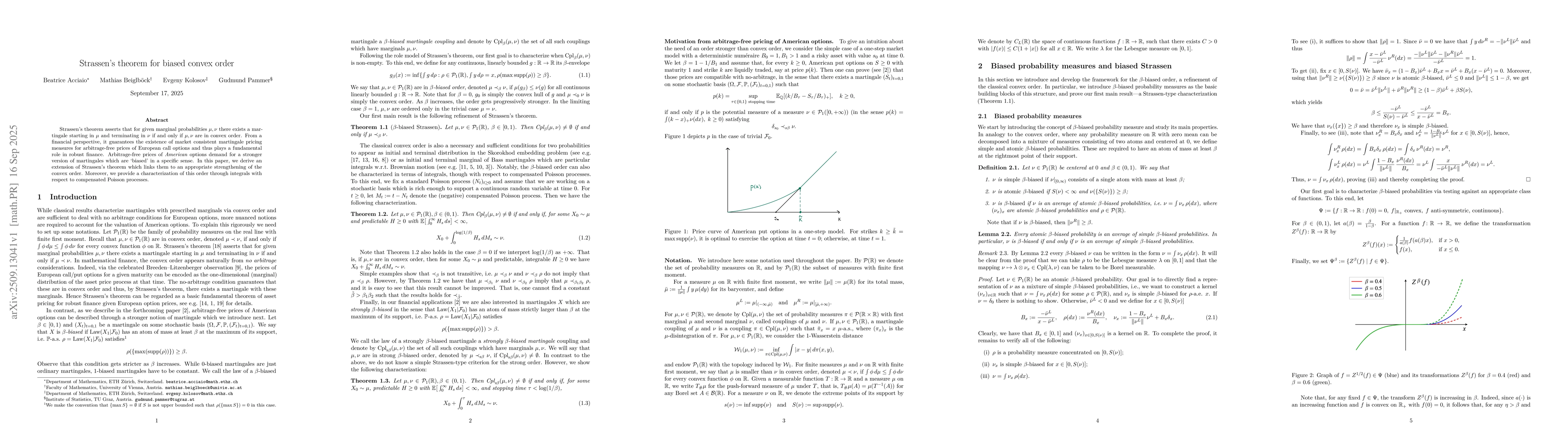

Strassen's theorem asserts that for given marginal probabilities $\mu,\nu$ there exists a martingale starting in $\mu$ and terminating in $\nu$ if and only if $\mu,\nu$ are in convex order. From a fin...

This paper studies the inverse problem of flow matching (FM) between distributions with finite exponential moment, a problem motivated by modern generative AI applications such as the distillation of ...

We formulate a dynamic reinsurance problem in which the insurer seeks to control the terminal distribution of its surplus while minimizing the L2-norm of the ceded risk. Using techniques from martinga...

The adapted Bures--Wasserstein space consists of Gaussian processes endowed with the adapted Wasserstein distance. It can be viewed as the analogue of the classical Bures--Wasserstein space in optimal...

We propose a mathematical framework to explain implicit regularization from early stopping during the training of overparametrized neural networks. In the mean-field limit, the parameter distribution ...

We study the Schrödinger-Bass problem, a one-parameter family of semimartingale optimal transport problems indexed by $β>0$, whose limiting regimes interpolate between the classical Schrödinger bridge...