Academic Profile

Statistics

Similar Authors

Papers on arXiv

Expected values weighted by the inverse of a multivariate density or, equivalently, Lebesgue integrals of regression functions with multivariate regressors occur in various areas of applications, incl...

We show that established performance metrics in binary classification, such as the F-score, the Jaccard similarity coefficient or Matthews' correlation coefficient (MCC), are not robust to class imb...

We derive optimal rates of convergence in the supremum norm for estimating the H\"older-smooth mean function of a stochastic process which is repeatedly and discretely observed with additional error...

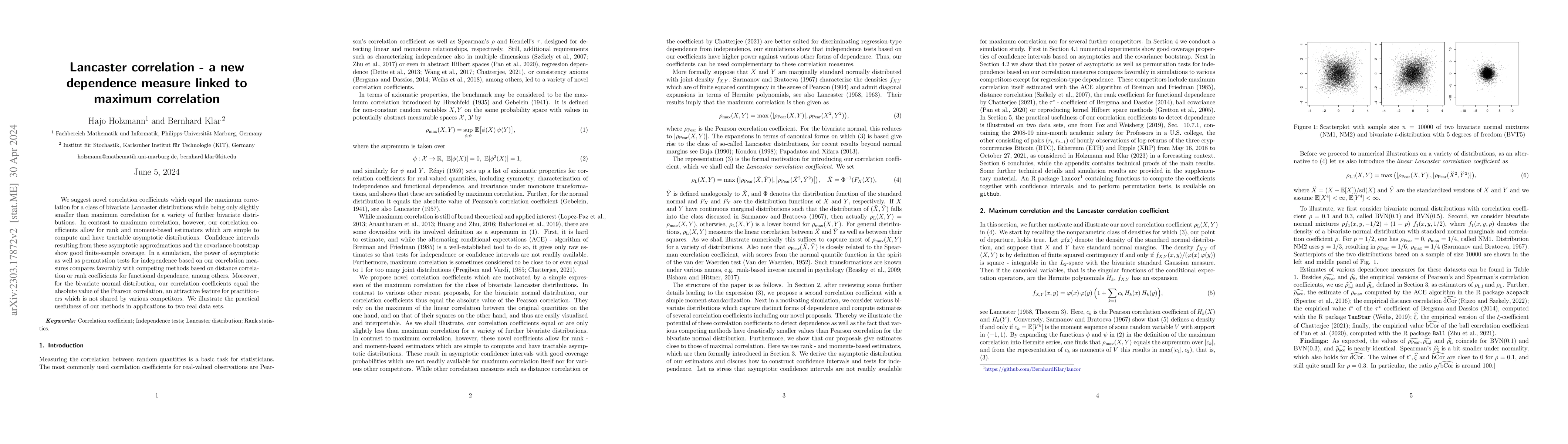

We suggest novel correlation coefficients which equal the maximum correlation for a class of bivariate Lancaster distributions while being only slightly smaller than maximum correlation for a variet...

The ideal probabilistic forecast for a random variable $Y$ based on an information set $\mathcal{F}$ is the conditional distribution of $Y$ given $\mathcal{F}$. In the context of point forecasts aim...

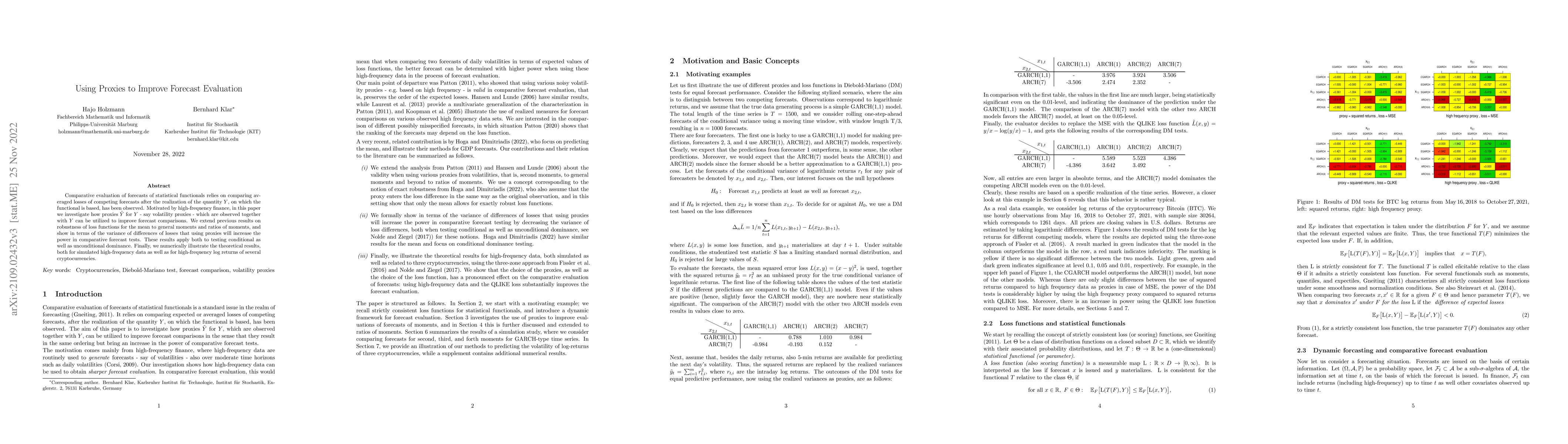

Comparative evaluation of forecasts of statistical functionals relies on comparing averaged losses of competing forecasts after the realization of the quantity $Y$, on which the functional is based,...

We consider linear random coefficient regression models, where the regressors are allowed to have a finite support. First, we investigate identifiability, and show that the means and the variances a...

A current strand of research in high-dimensional statistics deals with robustifying the available methodology with respect to deviations from the pervasive light-tail assumptions. In this paper we c...

In various applications of regression analysis, in addition to errors in the dependent observations also errors in the predictor variables play a substantial role and need to be incorporated in the ...

We construct new testing procedures for spherical and elliptical symmetry based on the characterization that a random vector $X$ with finite mean has a spherical distribution if and only if $\Ex[u^\...

We obtain minimax-optimal convergence rates in the supremum norm, including infor-mation-theoretic lower bounds, for estimating the covariance kernel of a stochastic process which is repeatedly observ...

In this paper, in a multivariate setting we derive near optimal rates of convergence in the minimax sense for estimating partial derivatives of the mean function for functional data observed under a f...

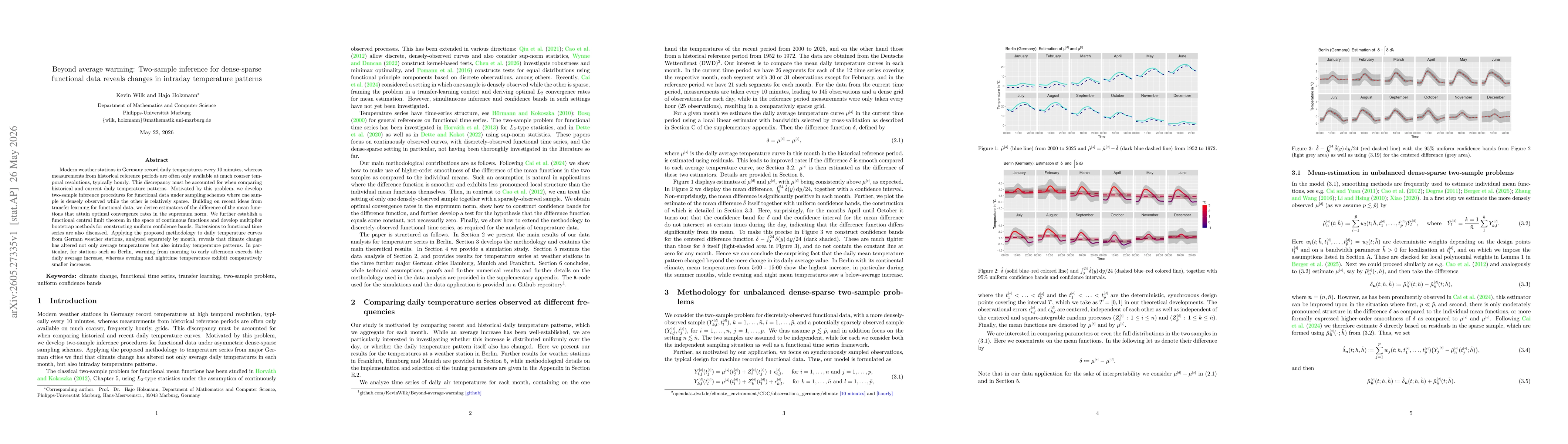

Modern weather stations in Germany record daily temperatures every 10 minutes, whereas measurements from historical reference periods are often only available at much coarser temporal resolutions, typ...

In genome wide association studies (GWASs) based on a case-control design, single nucleotide polymorphisms (SNPs) are typically evaluated for an association test and a Hardy-Weinberg equilibrium (HWE)...

We show that $L_2$-perturbation theory can be used to transfer rates of convergence in the supremum norm as well as weak convergence in the space of continuous functions from covariance kernel estimat...