Academic Profile

Statistics

Similar Authors

Papers on arXiv

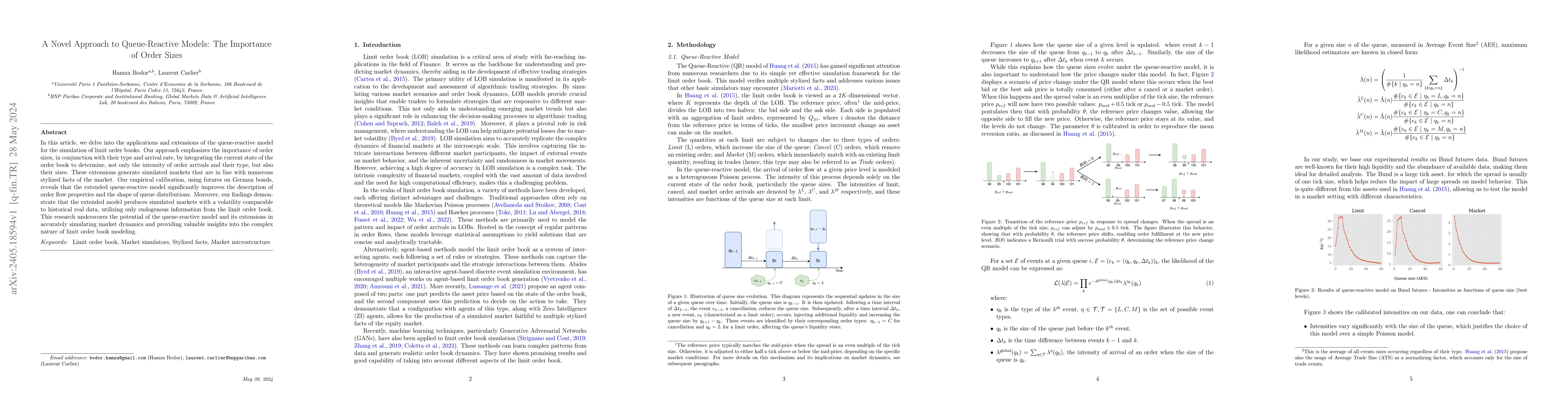

In this article, we delve into the applications and extensions of the queue-reactive model for the simulation of limit order books. Our approach emphasizes the importance of order sizes, in conjunct...

This paper presents an in-depth analysis of stylized facts in the context of futures on German bonds. The study examines four futures contracts on German bonds: Schatz, Bobl, Bund and Buxl, using ti...

Key Performance Indicators (KPI), which are essentially time series data, have been widely used to indicate the performance of telecom networks. Based on the given KPIs, a large set of anomaly detec...

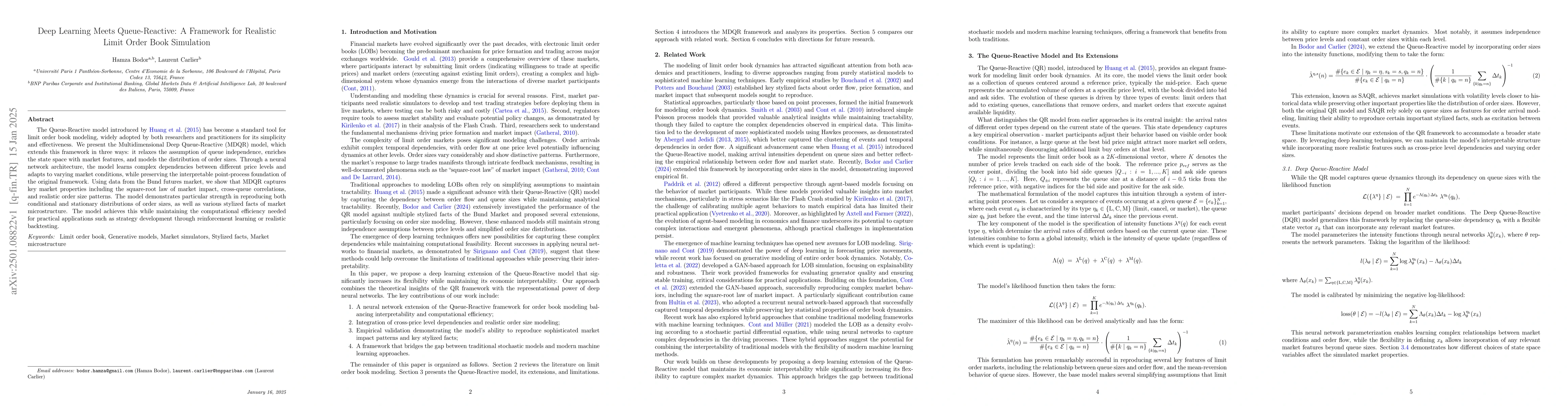

The Queue-Reactive model introduced by Huang et al. (2015) has become a standard tool for limit order book modeling, widely adopted by both researchers and practitioners for its simplicity and effecti...

This paper addresses the trade-off between internalisation and externalisation in the management of stochastic trade flows. We consider agents who must absorb flows and manage risk by deciding whether...