Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper we study the problem of optimally paying out dividends from an insurance portfolio, when the criterion is to maximize the expected discounted dividends over the lifetime of the company...

Hybrid stochastic differential equations are a useful tool to model continuously varying stochastic systems which are modulated by a random environment that may depend on the system state itself. In...

In this paper we address the problem of optimal dividend payout strategies from a surplus process governed by Brownian motion with drift under a drawdown constraint, i.e. the dividend rate can never...

The resource-consuming mining of blocks on a blockchain equipped with a proof of work consensus protocol bears the risk of ruin, namely when the operational costs for the mining exceed the received ...

We consider estimation of the extreme value index and extreme quantiles for heavy-tailed data that are right-censored. We study a general procedure of removing low importance observations in tail es...

Products between phase-type distributed random variables and any independent, positive and continuous random variable are studied. Their asymptotic properties are established, and an expectation-max...

We study the problem of optimal dividend payout from a surplus process governed by Brownian motion with drift under the additional constraint of ratcheting, i.e. the dividend rate can never decrease...

In this paper we investigate the flexibility of matrix distributions for the modeling of mortality. Starting from a simple Gompertz law, we show how the introduction of matrix-valued parameters via ...

Mining blocks on a blockchain equipped with a proof of work consensus protocol is well-known to be resource-consuming. A miner bears the operational cost, mainly electricity consumption and IT gear,...

In various applications of heavy-tail modelling, the assumed Pareto behavior is tempered ultimately in the range of the largest data. In insurance applications, claim payments are influenced by clai...

We extend the Kulkarni class of multivariate phase--type distributions in a natural time--fractional way to construct a new class of multivariate distributions with heavy-tailed Mittag-Leffler(ML)-d...

We extend the construction principle of multivariate phase-type distributions to establish an analytically tractable class of heavy-tailed multivariate random variables whose marginal distributions ...

We address a long-standing open problem in risk theory, namely the optimal strategy to pay out dividends from an insurance surplus process, if the dividend rate can never be decreased. The optimalit...

We study tail estimation in Pareto-like settings for datasets with a high percentage of randomly right-censored data, and where some expert information on the tail index is available for the censore...

In this paper we define the class of matrix Mittag-Leffler distributions and study some of its properties. We show that it can be interpreted as a particular case of an inhomogeneous phase-type dist...

We consider removing lower order statistics from the classical Hill estimator in extreme value statistics, and compensating for it by rescaling the remaining terms. Trajectories of these trimmed sta...

We study optimal dividend strategies for an insurance company facing natural catastrophe claims, anticipating the arrival of a climate tipping point after which the claim intensity and/or the claim si...

Mining blocks in a blockchain using the \textit{Proof-of-Work} consensus protocol involves significant risk, as network participants face continuous operational costs while earning infrequent capital ...

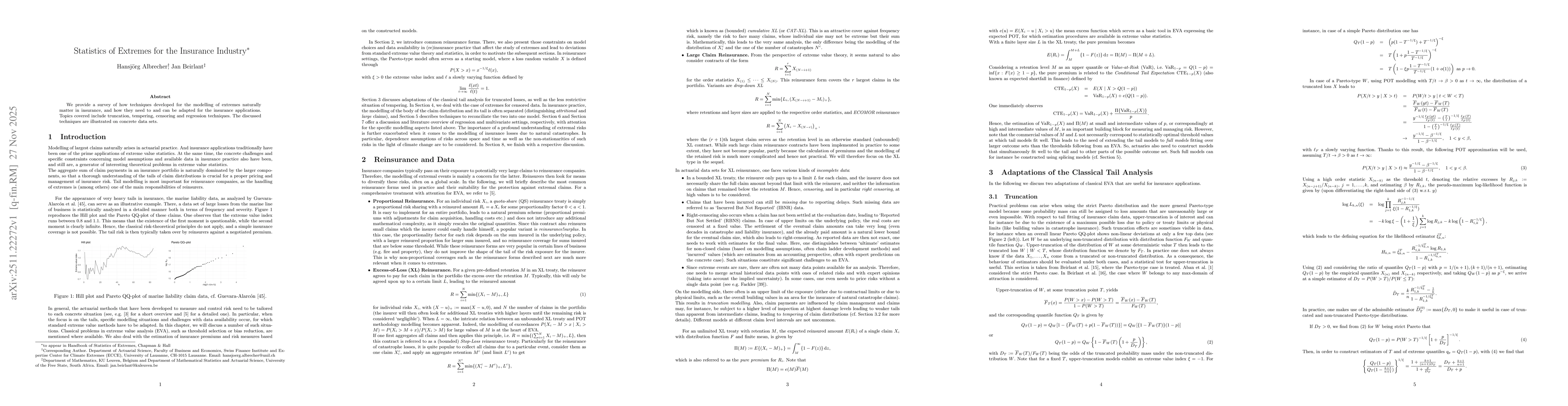

We provide a survey of how techniques developed for the modelling of extremes naturally matter in insurance, and how they need to and can be adapted for the insurance applications. Topics covered incl...

Achieving net-zero carbon emissions requires a transformation of energy systems, industrial processes, and consumption patterns. In particular, a transition towards that goal involves a gradual reduct...