Academic Profile

Statistics

Similar Authors

Papers on arXiv

We regard the optimal reinsurance problem as an iterated optimal transport problem between a (known) initial and an (unknown) resulting risk exposure of the insurer. We also provide conditions that ...

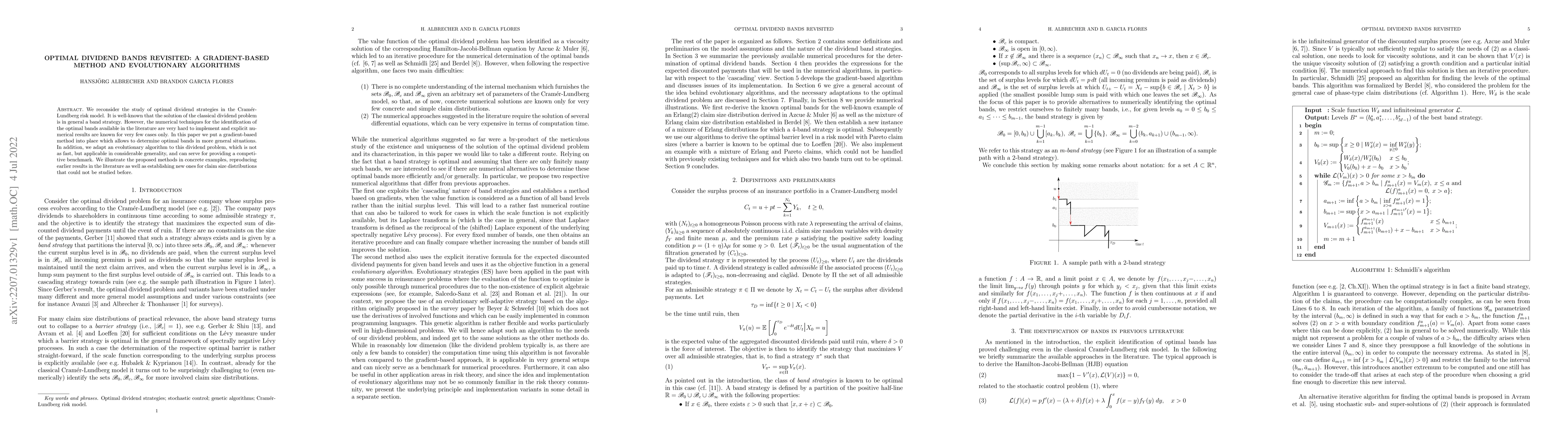

We reconsider the study of optimal dividend strategies in the Cram\'er-Lundberg risk model. It is well-known that the solution of the classical dividend problem is in general a band strategy. Howeve...

The statistical censoring setup is extended to the situation when random measures can be assigned to the realization of datapoints, leading to a new way of incorporating expert information into the ...

We consider the classical Cram\'er-Lundberg risk model with claim sizes that are mixtures of phase-type and subexponential variables. Exploiting a specific geometric compound representation, we prop...

We extend the construction principle of phase-type (PH) distributions to allow for inhomogeneous transition rates and show that this naturally leads to direct probabilistic descriptions of certain t...

This paper explores the optimal policy for using an allocated carbon emission budget over time with the objective to maximize profit, by explicitly taking into account present-biased preferences of de...

Cost-of-capital valuation is a well-established approach to the valuation of liabilities and is one of the cornerstones of current regulatory frameworks for the insurance industry. Standard cost-of-ca...