Academic Profile

Statistics

Similar Authors

Papers on arXiv

Lead time data is compositional data found frequently in the hospitality industry. Hospitality businesses earn fees each day, however these fees cannot be recognized until later. For business purpos...

Short-term shifts in booking behaviors can disrupt forecasting in the travel and hospitality industry, especially during global crises. Traditional metrics like average or median lead times often over...

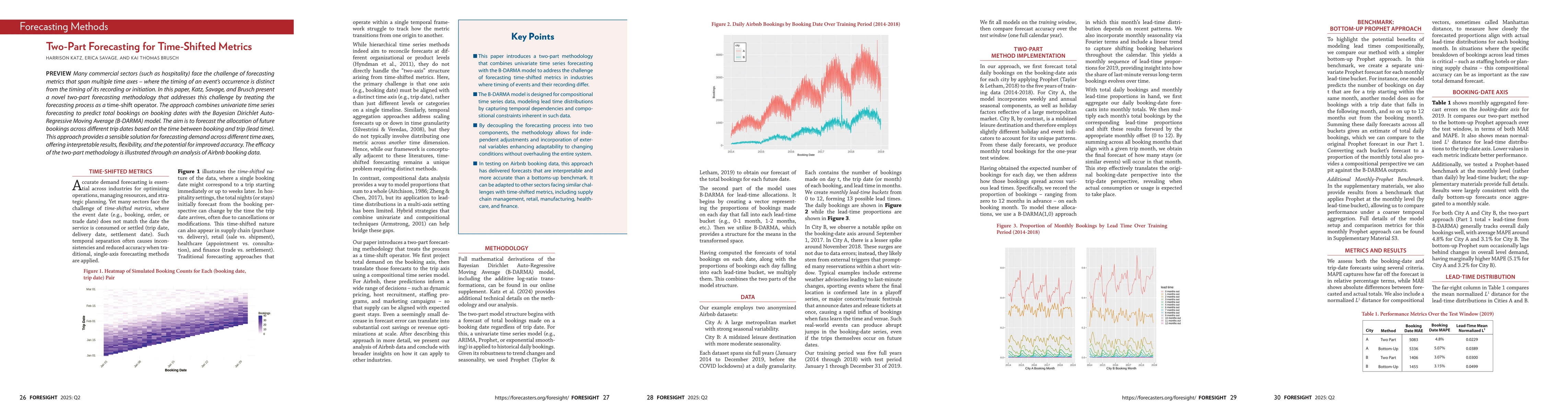

Katz, Savage, and Brusch propose a two-part forecasting method for sectors where event timing differs from recording time. They treat forecasting as a time-shift operation, using univariate time serie...

High-dimensional vector autoregressive (VAR) models offer a versatile framework for multivariate time series analysis, yet face critical challenges from over-parameterization and uncertain lag order. ...

Prior choice can strongly influence Bayesian Dirichlet ARMA (B-DARMA) inference for compositional time-series. Using simulations with (i) correct lag order, (ii) overfitting, and (iii) underfitting, w...

Accurate forecasts of the US renewable-generation mix are critical for planning transmission upgrades, sizing storage, and setting balancing-market rules. We present a Bayesian Dirichlet ARMA (BDARMA)...

We analyze daily Airbnb service-fee shares across eleven settlement currencies, a compositional series that shows bursts of volatility after shocks such as the COVID-19 pandemic. Standard Dirichlet ti...

Using every U.S. Airbnb reservation created from 1 January 2019 through 31 December 2024, weighted by nights booked, we document a lasting shift toward longer stays after the COVID 19 shock. Mean nigh...

Observation-driven Dirichlet models for compositional time series often use the additive log-ratio (ALR) link and include a moving-average (MA) term built from ALR residuals. In the standard B--DARMA ...

This commentary translates the central ideas in Lead times in flux into a practice ready handbook in R. The original article measures change in the full distribution of booking lead times with a norma...

Compositional time series, vectors of proportions summing to unity observed over time, frequently exhibit structural breaks due to external shocks, policy changes, or market disruptions. Standard meth...

Understanding how the composition of guest origin markets evolves over time is critical for destination marketing organizations, hospitality businesses, and tourism planners. We develop and apply Baye...

Tourism demand forecasting is methodologically mature, but it typically treats accommodation supply as fixed or exogenous. In platform-mediated short-term rentals, supply is elastic, decision-driven, ...

Model retraining is usually treated as an ongoing maintenance task. But as Harrison Katz now argues, retraining can be better understood as approximate Bayesian inference under computational constrain...

Forecasters often choose retraining schedules by convention rather than by an explicit decision rule. This paper gives that decision a posterior-space language. We define learning debt as the divergen...

Forecasting systems are commonly refreshed at every review period, and that refresh usually bundles two distinct operations: estimating parameters and selecting the model form. Recent evidence suggest...