Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper expands traditional stochastic volatility models by allowing for time-varying skewness without imposing it. While dynamic asymmetry may capture the likely direction of future asset return...

There has been increased research interest in the subfield of sparse Bayesian factor analysis with shrinkage priors, which achieve additional sparsity beyond the natural parsimonity of factor models...

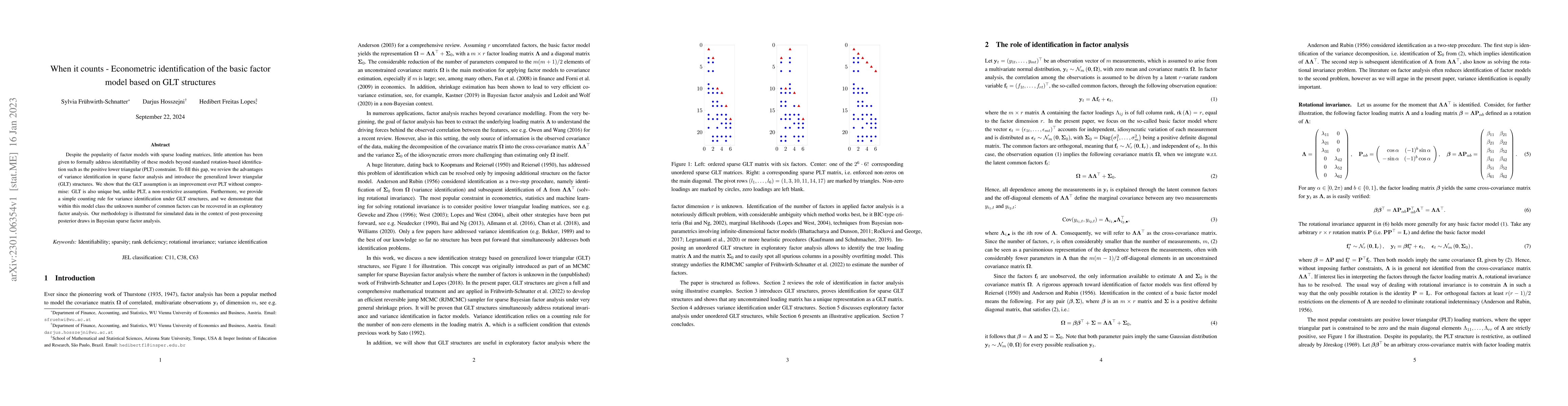

Despite the popularity of factor models with sparse loading matrices, little attention has been given to formally address identifiability of these models beyond standard rotation-based identificatio...

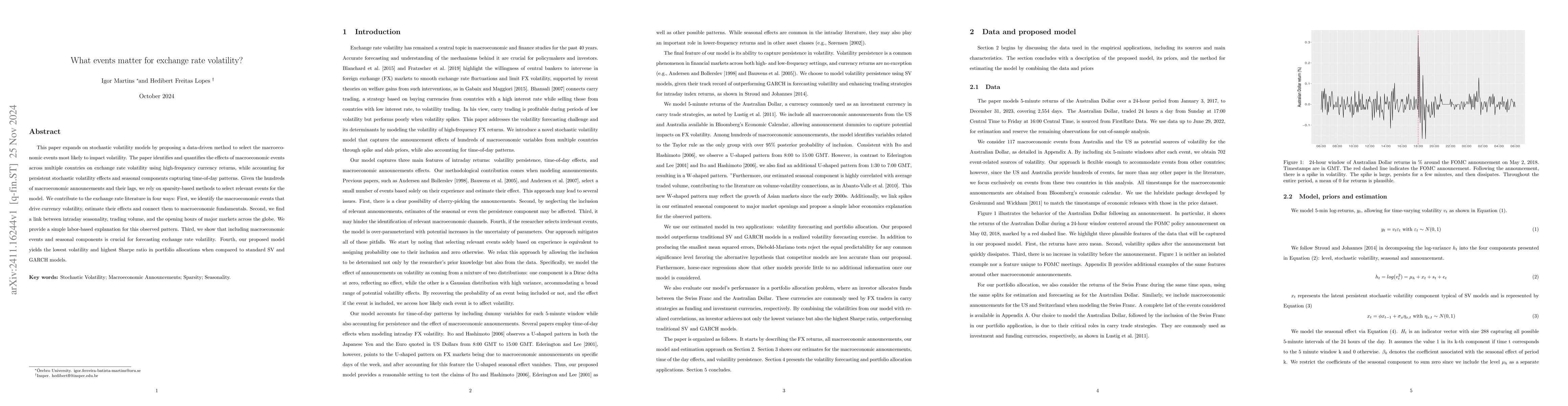

This paper expands on stochastic volatility models by proposing a data-driven method to select the macroeconomic events most likely to impact volatility. The paper identifies and quantifies the effect...