Academic Profile

Statistics

Similar Authors

Papers on arXiv

In a continuous-time Kyle setting, we prove global existence of an equilibrium when the insider faces a terminal trading constraint. We prove that our equilibrium model produces output consistent wi...

The domain structure in in-plane magnetized Fe/Ni/W(110) films is investigated using spin-polarized low-energy electron microscopy. A novel transition of the domain wall shape from a zigzag-like pat...

Language understanding must identify the logical connections between events in a discourse, but core events are often unstated due to their commonsense nature. This paper fills in these missing even...

Preconditions provide a form of logical connection between events that explains why some events occur together and information that is complementary to the more widely studied relations such as caus...

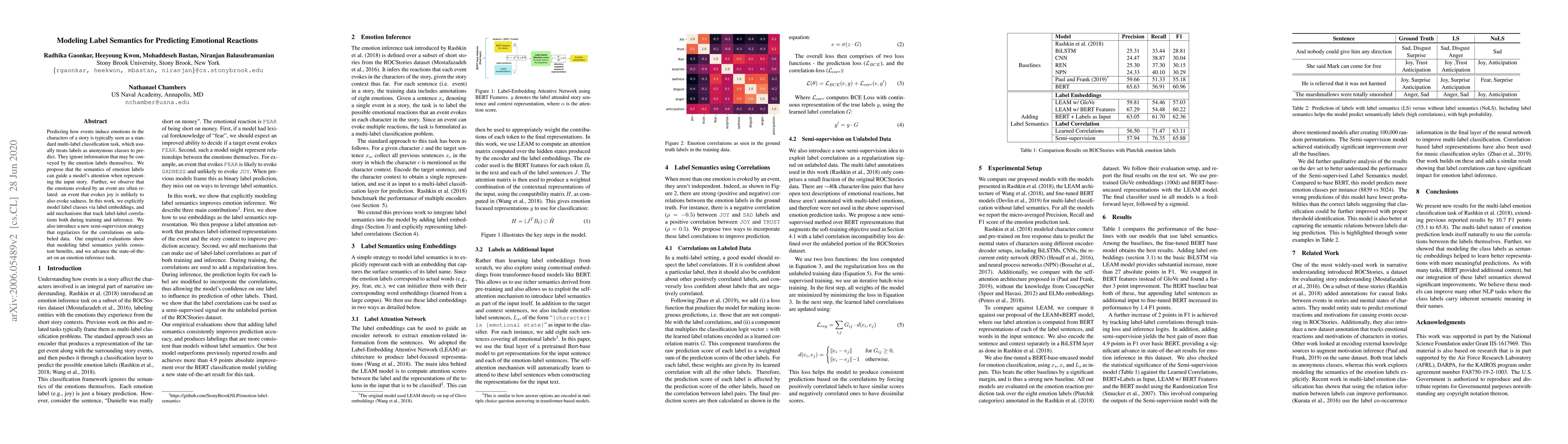

Predicting how events induce emotions in the characters of a story is typically seen as a standard multi-label classification task, which usually treats labels as anonymous classes to predict. They ...

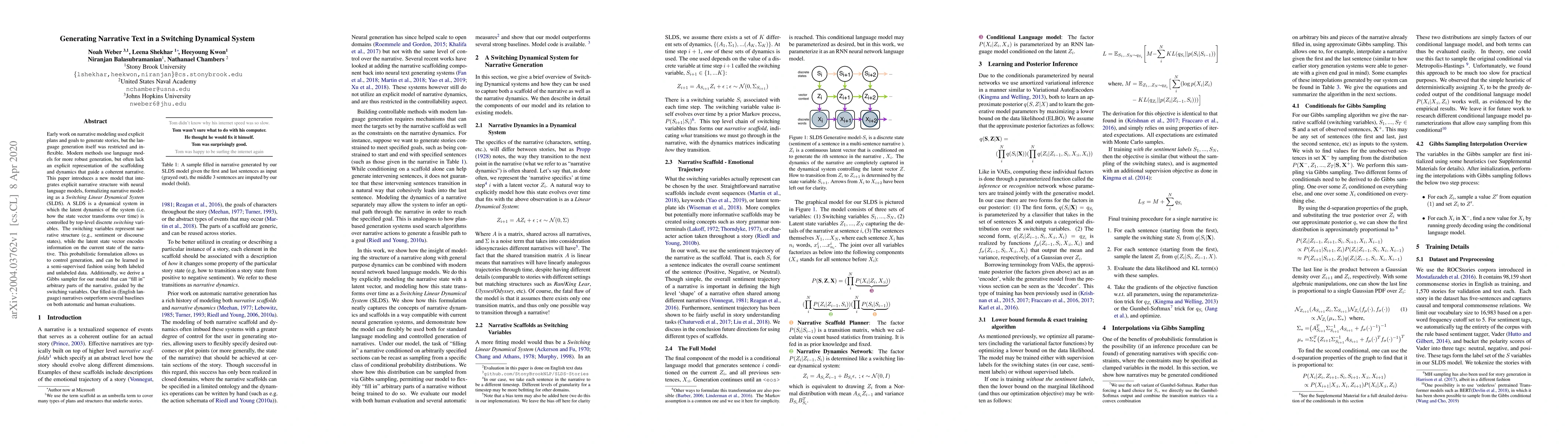

Early work on narrative modeling used explicit plans and goals to generate stories, but the language generation itself was restricted and inflexible. Modern methods use language models for more robu...

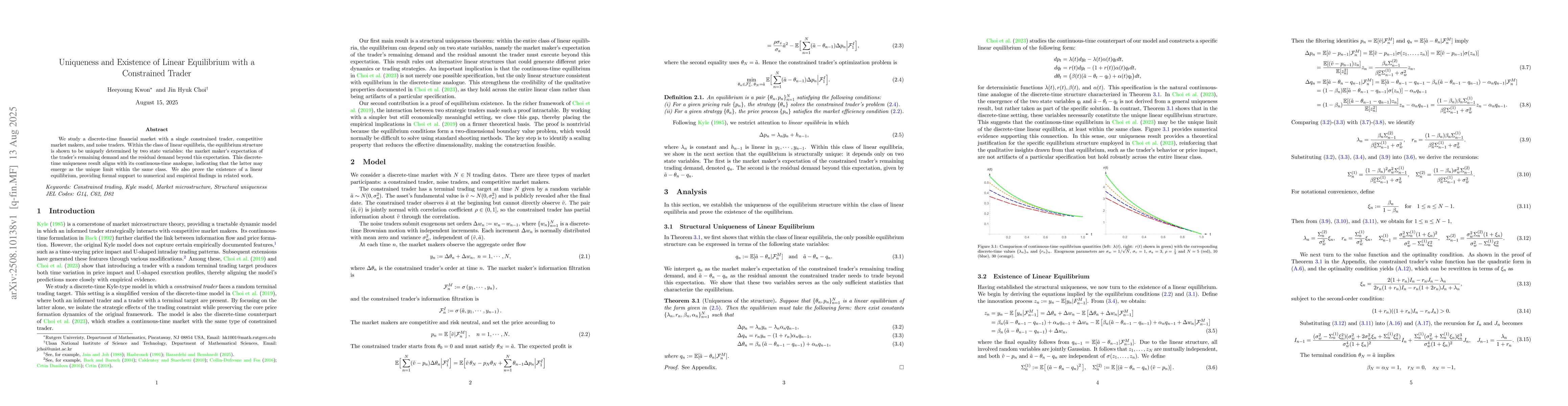

We study a discrete-time financial market with a single constrained trader, competitive market makers, and noise traders. Within the class of linear equilibria, the equilibrium structure is shown to b...

We extend the limited participation model in Basak and Cuoco (1998) to allow for traders with different time-preference coefficients but identical constant relative risk-aversion coefficients. Our mai...