Academic Profile

Statistics

Similar Authors

Papers on arXiv

Prediction and quantification of future volatility and returns play an important role in financial modelling, both in portfolio optimization and risk management. Natural language processing today al...

This manuscript introduces the hype-adjusted probability measure developed in the context of a new Natural Language Processing (NLP) approach for market forecasting. A novel sentiment score equation i...

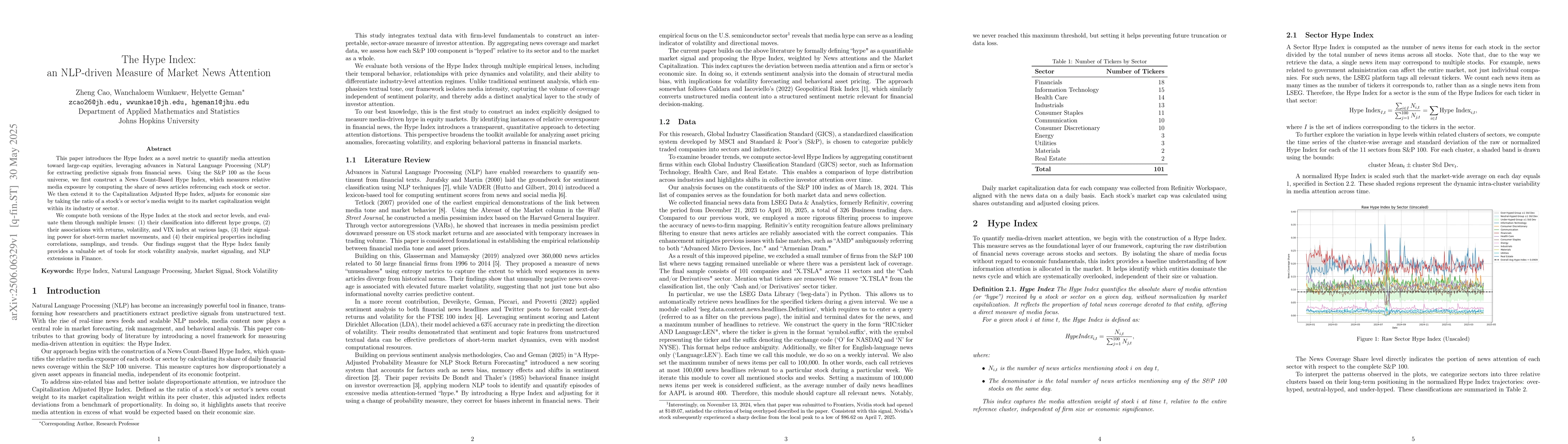

This paper introduces the Hype Index as a novel metric to quantify media attention toward large-cap equities, leveraging advances in Natural Language Processing (NLP) for extracting predictive signals...

We propose a novel model, the Hyped Log-Periodic Power Law Model (HLPPL), to the problem of quantifying and detecting financial bubbles, an ever-fascinating one for academics and practitioners alike. ...