Academic Profile

Statistics

Similar Authors

Papers on arXiv

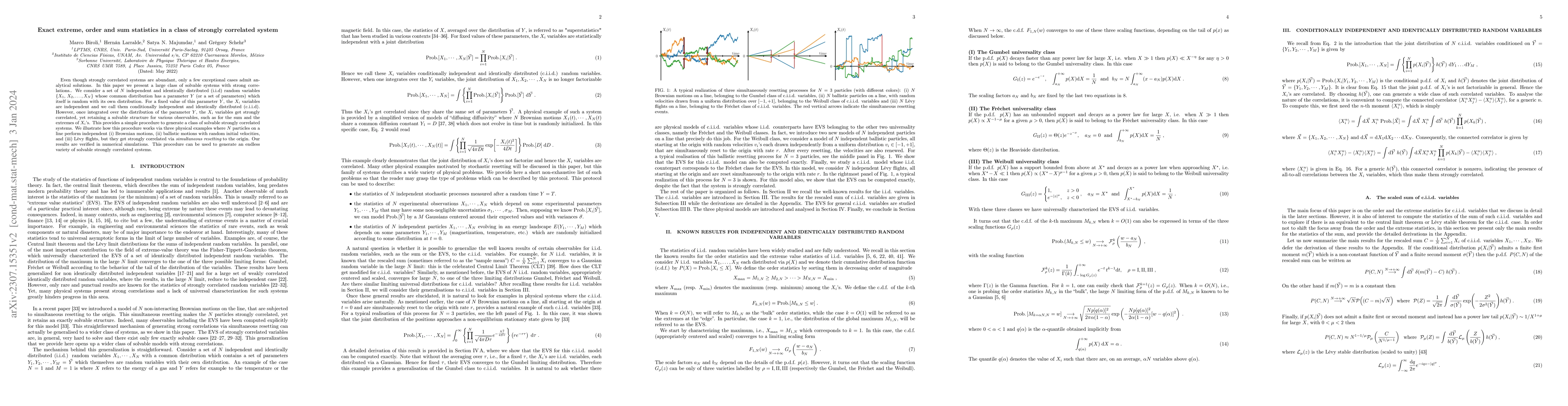

Even though strongly correlated systems are abundant, only a few exceptional cases admit analytical solutions. In this paper we present a large class of solvable systems with strong correlations.. W...

There are several definitions of energy density in quantum mechanics. These yield expressions that differ locally, but all satisfy a continuity equation and integrate to the value of the expected en...

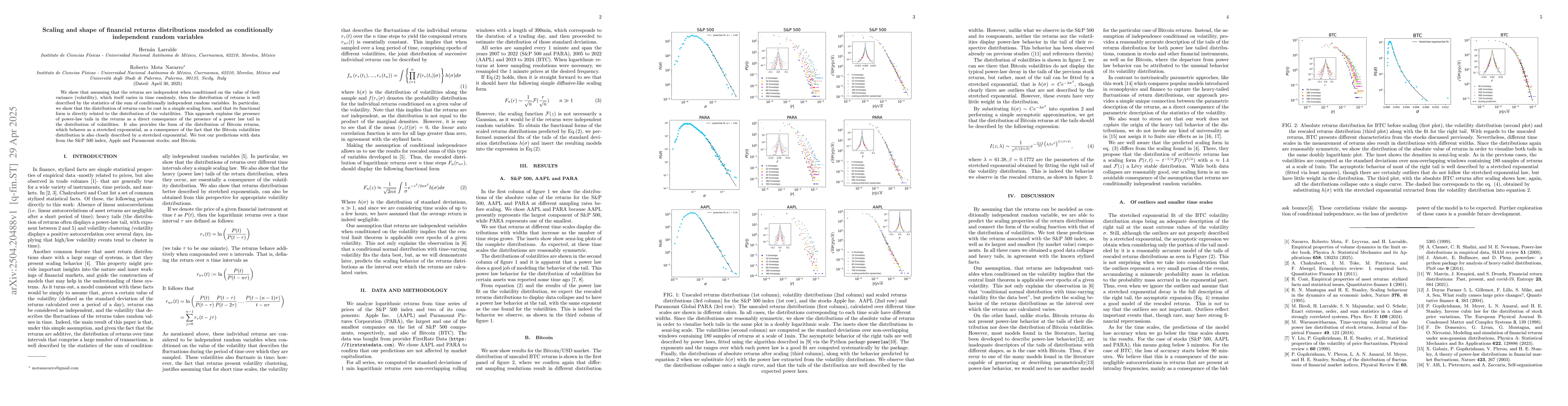

The study of order volumes in financial markets has shown that these display several non-trivial statistical properties. Most studies have been focused on the bulk properties of volume of incoming o...

We study, analytically and numerically, a simple $\mathcal{PT}$-symmetric tight-binding ring with an onsite energy $a$ at the gain and loss sites. We show that if $a\neq 0$, the system generically e...

We study the spectrum, eigenstates and transport properties of a simple $\mathcal{P}\mathcal{T}$-symmetric model consisting in a finite, complex, square well potential with a delta potential at the or...

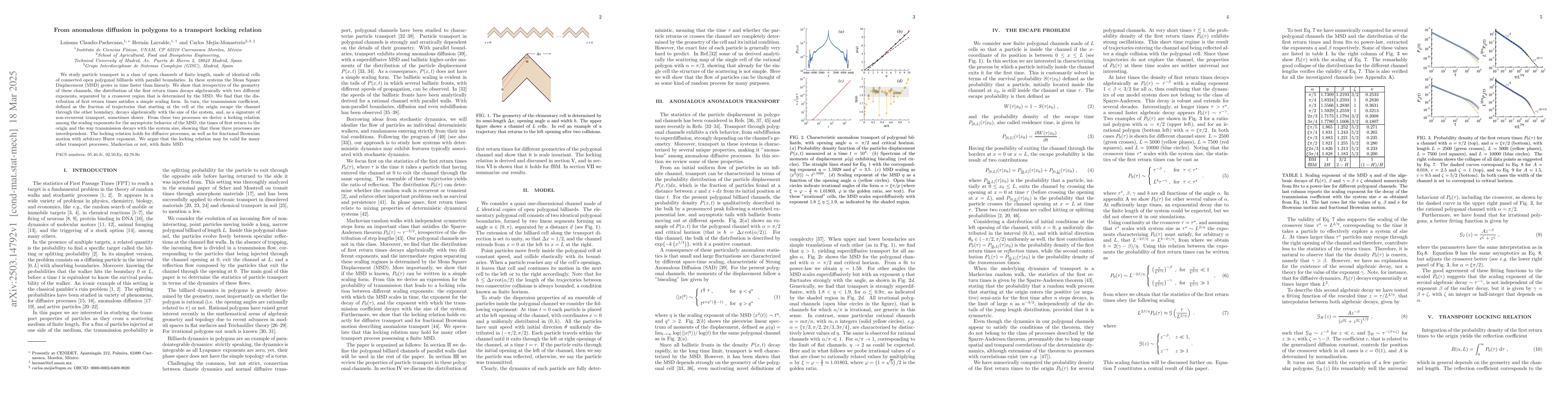

We study particle transport in a class of open channels of finite length, made of identical cells of connected open polygonal billiards with parallel boundaries. In these systems the Mean Square Displ...

We show that assuming that the returns are independent when conditioned on the value of their variance (volatility), which itself varies in time randomly, then the distribution of returns is well desc...

We study the phenomenon of quantum backflow in tight-binding systems with complex couplings, considering different boundary conditions and lattice sizes. Backflow is an intrinsically non-classical eff...