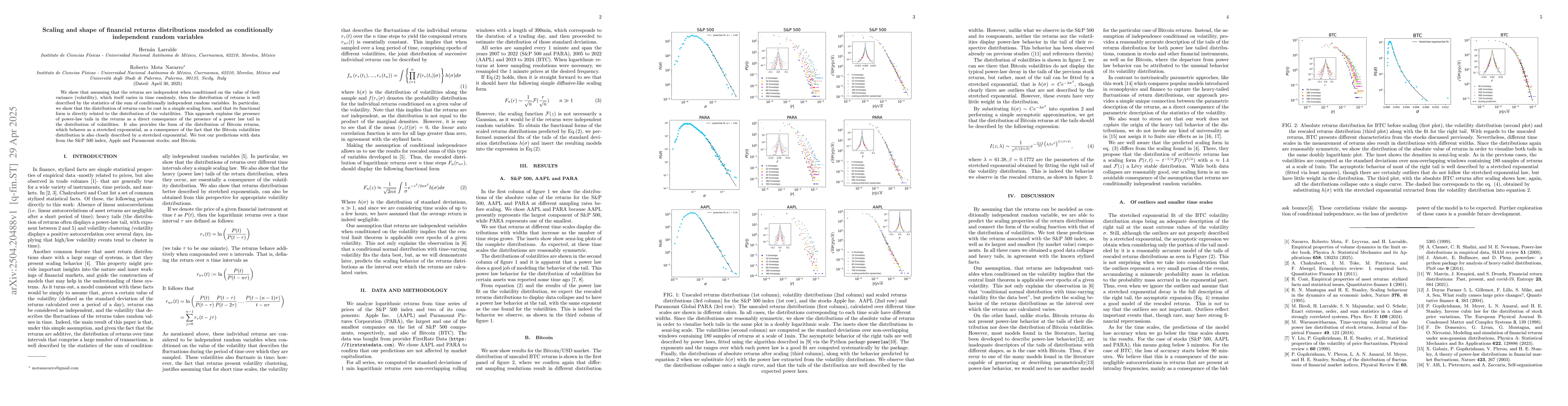

We show that assuming that the returns are independent when conditioned on

the value of their variance (volatility), which itself varies in time randomly,

then the distribution of returns is well described by the statistics of the sum

of conditionally independent random variables. In particular, we show that the

distribution of returns can be cast in a simple scaling form, and that its

functional form is directly related to the distribution of the volatilities.

This approach explains the presence of power-law tails in the returns as a

direct consequence of the presence of a power law tail in the distribution of

volatilities. It also provides the form of the distribution of Bitcoin returns,

which behaves as a stretched exponential, as a consequence of the fact that the

Bitcoin volatilities distribution is also closely described by a stretched

exponential. We test our predictions with data from the S\&P 500 index, Apple

and Paramount stocks; and Bitcoin.

Discussion 0