Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper introduces and studies factor risk measures. While risk measures only rely on the distribution of a loss random variable, in many cases risk needs to be measured relative to some major fa...

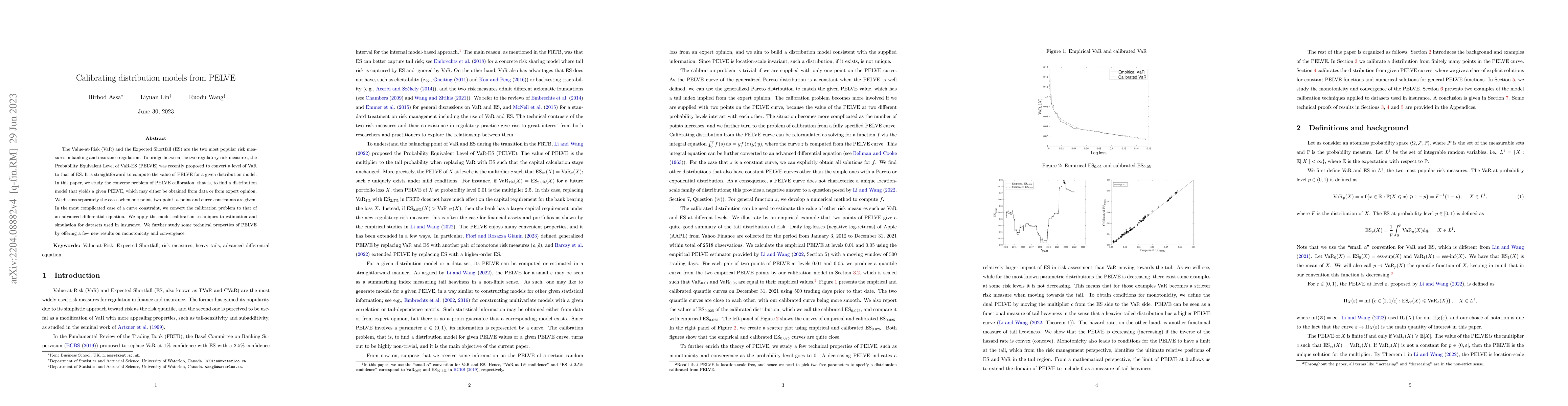

The Value-at-Risk (VaR) and the Expected Shortfall (ES) are the two most popular risk measures in banking and insurance regulation. To bridge between the two regulatory risk measures, the Probabilit...

Risk governance is not only about identifying and measuring adverse states of the world. It also asks when an institution is entitled to rely on a risk claim. This paper introduces modal epistemic too...