Academic Profile

Statistics

Similar Authors

Papers on arXiv

In a continuous-time economy, this study formulates the Epstein-Zin (EZ) preference for the discounted dividend (or cash payouts) of stockholders as an EZ singular control utility. We show that such...

This paper studies robust time-inconsistent (TIC) linear-quadratic stochastic control problems, formulated by stochastic differential games. By a spike variation approach, we derive sufficient condi...

This study investigates an optimal consumption--investment problem in which the unobserved stock trend is modulated by a hidden Markov chain that represents different economic regimes. In the classi...

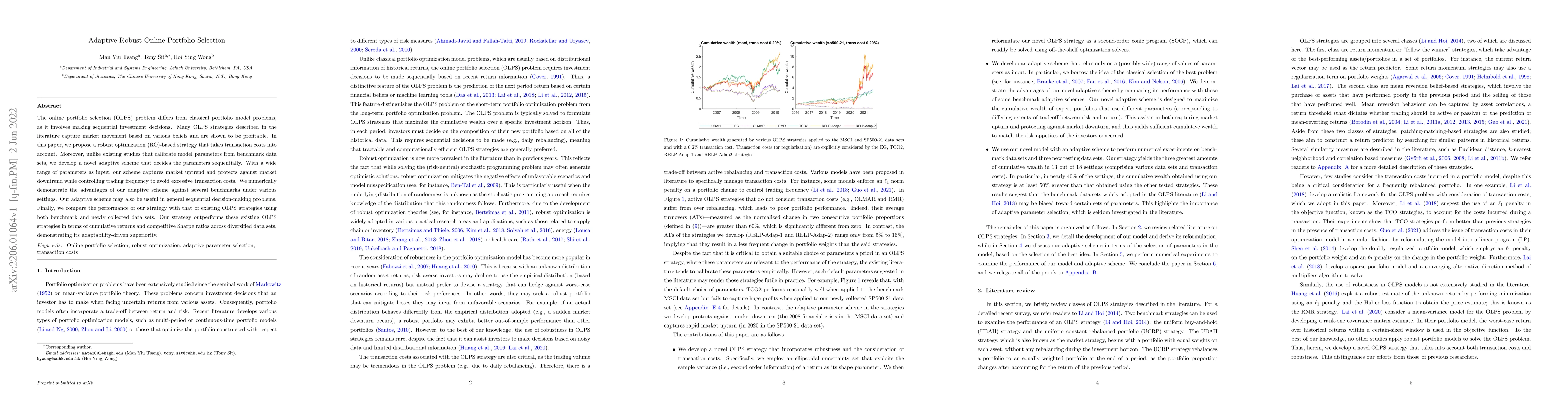

The online portfolio selection (OLPS) problem differs from classical portfolio model problems, as it involves making sequential investment decisions. Many OLPS strategies described in the literature...

Any firm whose business strategy has an exposure constraint that limits its potential gain naturally considers expansion, as this can increase its exposure. We model business expansion as an enlarge...

This paper investigates the time-consistent mean-variance reinsurance-investment (RI) problem faced by life insurers. Inspired by recent findings that mortality rates exhibit long-range dependence (...

Social distancing has been the only effective way to contain the spread of an infectious disease prior to the availability of the pharmaceutical treatment. It can lower the infection rate of the dis...

While abundant empirical studies support the long-range dependence (LRD) of mortality rates, the corresponding impact on mortality securities are largely unknown due to the lack of appropriate tract...

In this paper, we consider equilibrium strategies under Volterra processes and time-inconsistent preferences embracing mean-variance portfolio selection (MVP). Using a functional It\^o calculus appr...

This paper investigates Merton's portfolio problem in a rough stochastic environment described by Volterra Heston model. The model has a non-Markovian and non-semimartingale structure. By considerin...

Motivated by empirical evidence for rough volatility models, this paper investigates continuous-time mean-variance (MV) portfolio selection under the Volterra Heston model. Due to the non-Markovian ...

Empirical studies with publicly available life tables identify long-range dependence (LRD) in national mortality data. Although the longevity market is supposed to benchmark against the national force...

We propose and analyze a continuous-time robust reinforcement learning framework for optimal stopping problems under ambiguity. In this framework, an agent chooses a stopping rule motivated by two obj...

Using a martingale representation, we introduce a novel deep-learning approach, which we call DeepMartingale, to study the duality of discrete-monitoring optimal stopping problems in continuous time. ...

Contextual stochastic optimization is an advanced methodology to model uncertainty in the presence of contextual information during decision planning processes. Although classical methodologies focus ...

We study finite-horizon optimal switching with discrete intervention dates on a general filtration, allowing continuous-time observations between decision dates, and develop a deep-learning-based dual...