Academic Profile

Statistics

Similar Authors

Papers on arXiv

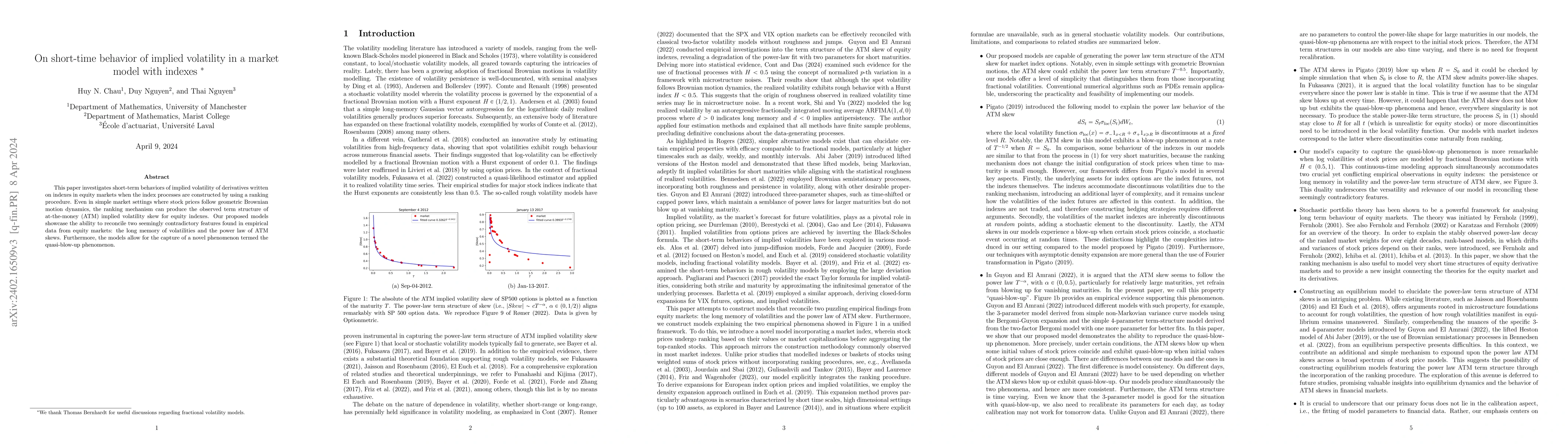

This paper investigates short-term behaviors of implied volatility of derivatives written on indexes in equity markets when the index processes are constructed by using a ranking procedure. Even in ...

We formulate a superhedging theorem in the presence of transaction costs and model uncertainty. Asset prices are assumed continuous and uncertainty is modelled in a parametric setting. Our proof rel...

This paper is devoted to a study of robust fundamental theorems of asset pricing in discrete time and finite horizon settings. Uncertainty is modelled by a (possibly uncountable) family of price pro...

Stochastic Gradient Hamiltonian Monte Carlo (SGHMC) is a momentum version of stochastic gradient descent with properly injected Gaussian noise to find a global minimum. In this paper, non-asymptotic...

In the context of a general semimartingale model of a complete market, we aim at answering the following question: How much is an investor willing to pay for learning some inside information that al...

In this paper, a new approach for solving the problems of pricing and hedging derivatives is introduced in a general frictionless market setting. The method is applicable even in cases where an equiva...