Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we present a probabilistic numerical algorithm combining dynamic programming, Monte Carlo simulations and local basis regressions to solve non-stationary optimal multiple switching pr...

We propose a probabilistic numerical algorithm to solve Backward Stochastic Differential Equations (BSDEs) with nonnegative jumps, a class of BSDEs introduced in [9] for representing fully nonlinear...

We propose a comprehensive framework for policy gradient methods tailored to continuous time reinforcement learning. This is based on the connection between stochastic control problems and randomise...

We develop a new policy gradient and actor-critic algorithm for solving mean-field control problems within a continuous time reinforcement learning setting. Our approach leverages a gradient-based r...

We study binary opinion formation in a large population where individuals are influenced by the opinions of other individuals. The population is characterised by the existence of (i) communities whe...

We propose a novel generative model for time series based on Schr{\"o}dinger bridge (SB) approach. This consists in the entropic interpolation via optimal transport between a reference probability m...

We study policy gradient for mean-field control in continuous time in a reinforcement learning setting. By considering randomised policies with entropy regularisation, we derive a gradient expectati...

This paper is devoted to the numerical resolution of McKean-Vlasov control problems via the class of mean-field neural networks introduced in our companion paper [25] in order to learn the solution ...

We study the machine learning task for models with operators mapping between the Wasserstein space of probability measures and a space of functions, like e.g. in mean-field games/control problems. T...

We investigate propagation of chaos for mean field Markov Decision Process with common noise (CMKV-MDP), and when the optimization is performed over randomized open-loop controls on infinite horizon...

We propose machine learning methods for solving fully nonlinear partial differential equations (PDEs) with convex Hamiltonian. Our algorithms are conducted in two steps. First the PDE is rewritten i...

We consider the control of McKean-Vlasov dynamics (or mean-field control) with probabilistic state constraints. We rely on a level-set approach which provides a representation of the constrained pro...

With the emergence of new online channels and information technology, digital advertising tends to substitute more and more to traditional advertising by offering the opportunity to companies to tar...

We study the Bellman equation in the Wasserstein space arising in the study of mean field control problems, namely stochastic optimal control problems for McKean-Vlasov diffusion processes.Using the...

Machine learning methods for solving nonlinear partial differential equations (PDEs) are hot topical issues, and different algorithms proposed in the literature show efficient numerical approximatio...

We prove a rate of convergence for the $N$-particle approximation of a second-order partial differential equation in the space of probability measures, like the Master equation or Bellman equation o...

We study the optimal control of path-dependent McKean-Vlasov equations valued in Hilbert spaces motivated by non Markovian mean-field models driven by stochastic PDEs. We first establish the well-po...

We formulate an equilibrium model of intraday trading in electricity markets. Agents face balancing constraints between their customers consumption plus intraday sales and their production plus intr...

This paper studies a variation of the continuous-time mean-variance portfolio selection where a tracking-error penalization is added to the mean-variance criterion. The tracking error term penalizes...

We propose new machine learning schemes for solving high dimensional nonlinear partial differential equations (PDEs). Relying on the classical backward stochastic differential equation (BSDE) repres...

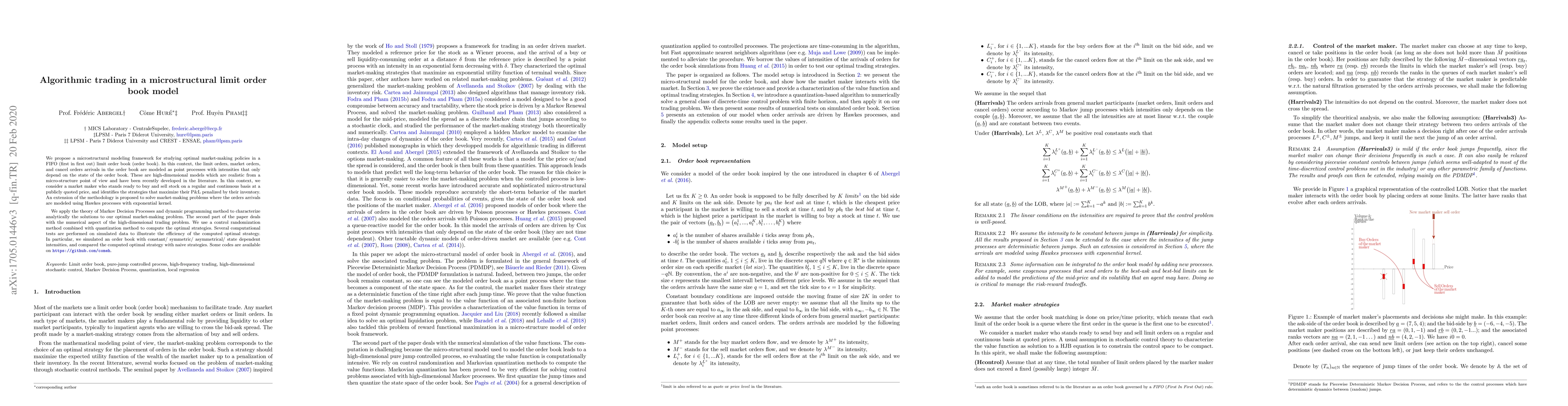

We propose a microstructural modeling framework for studying optimal market making policies in a FIFO (first in first out) limit order book (LOB). In this context, the limit orders, market orders, a...

We consider reinforcement learning (RL) methods for finding optimal policies in linear quadratic (LQ) mean field control (MFC) problems over an infinite horizon in continuous time, with common noise a...

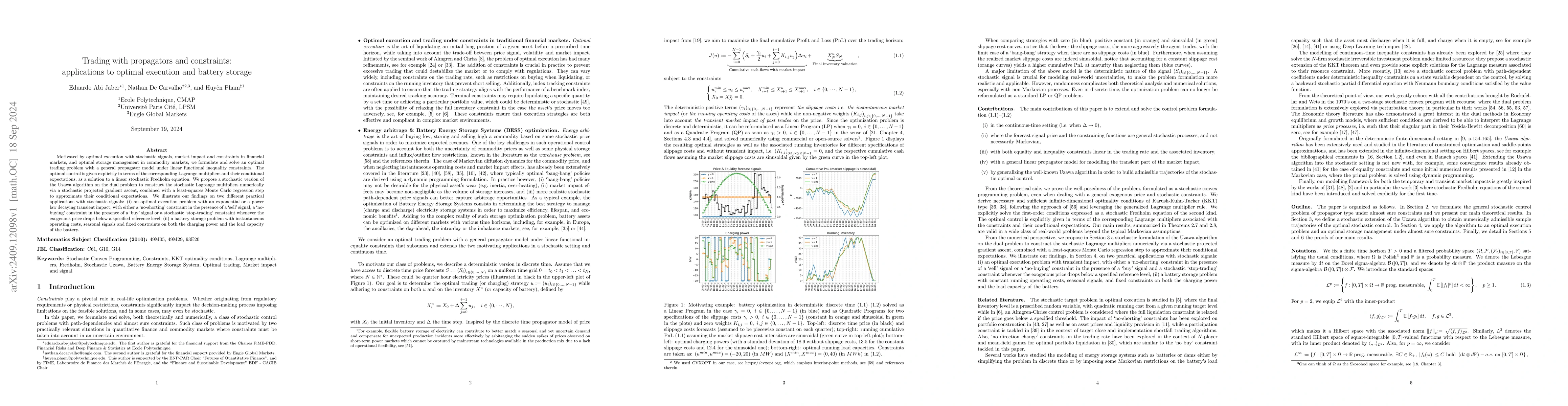

Motivated by optimal execution with stochastic signals, market impact and constraints in financial markets, and optimal storage management in commodity markets, we formulate and solve an optimal tradi...

We study the optimal control of mean-field systems with heterogeneous and asymmetric interactions. This leads to considering a family of controlled Brownian diffusion processes with dynamics depending...

We study mean-field control (MFC) problems with common noise using the control randomisation framework, where we substitute the control process with an independent Poisson point process, controlling i...

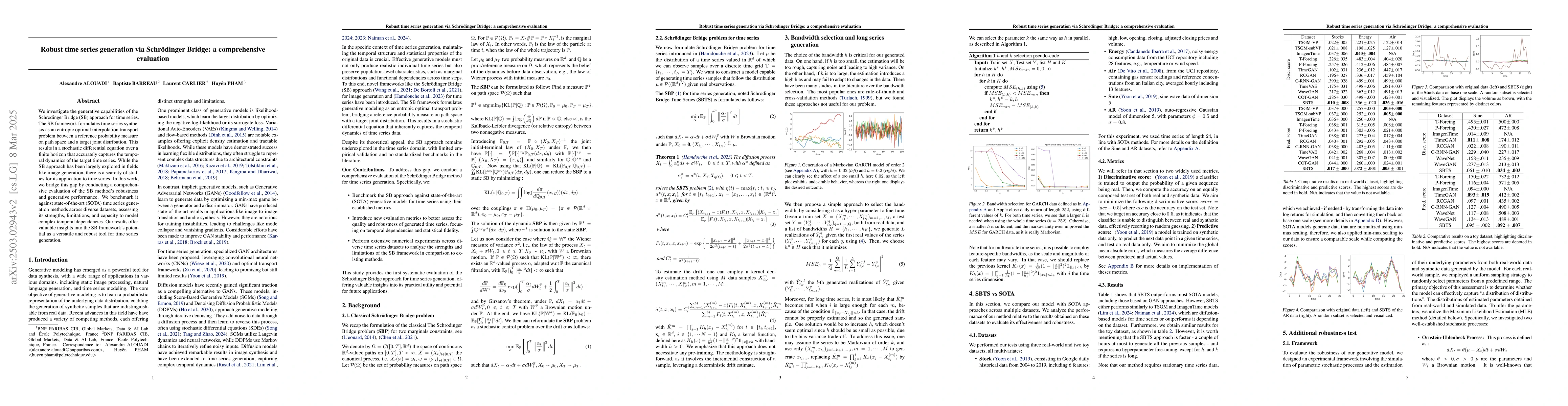

We investigate the generative capabilities of the Schr\"odinger Bridge (SB) approach for time series. The SB framework formulates time series synthesis as an entropic optimal interpolation transport p...

We study the linear-quadratic control problem for a class of non-exchangeable mean-field systems, which model large populations of heterogeneous interacting agents. We explicitly characterize the opti...

We study the Pontryagin maximum principle by deriving necessary and sufficient conditions for a class of optimal control problems arising in non exchangeable mean field systems, where agents interact ...

We study a class of mean-field control problems under partial observation. The controlled dynamics are of McKean-Vlasov type and are subject to regime switching driven by a hidden Markov chain. The ob...

We study model-free policy learning for discrete-time mean-field control (MFC) problems with finite state space and compact action space. In contrast to the extensive literature on value-based methods...

This short paper announces the main results of \cite{SBB2026}, where the Schrödinger--Bass Bridge (SBB) problem is introduced and studied in full generality. Here we provide a direct PDE derivation of...

The Schrodinger Bridge and Bass (SBB) formulation, which jointly controls drift and volatility, is an established extension of the classical Schrodinger Bridge (SB). Building on this framework, we int...

We study generative modeling for time series using entropic optimal transport and the Schrödinger bridge (SB) framework, with a focus on applications in finance and energy modeling. Extending the diff...

We study infinite-horizon Markov Decision Processes (MDPs) with a continuum of heterogeneous agents interacting through a common noise, without assuming exchangeability. We introduce the framework of ...

We study the approximation of operators acting on probability measures on a product space with prescribed marginal. Let $I$ be a label space endowed with a reference measure $λ$, and define $\cal M_λ$...

We study a semimartingale optimal transport problem interpolating between the Schrödinger bridge and the stretched Brownian motion associated with the Bass solution of the Skorokhod embedding problem....

We study the problem of generating synthetic time series that reproduce both marginal distributions and temporal dynamics, a central challenge in financial machine learning. Existing approaches typica...

This paper establishes a rigorous connection between regularized discrete-time reinforcement learning (RL) and continuous-time stochastic optimal control. Specifically, classical RL algorithms are typ...

We study nonparametric estimation of Schrödinger bridge (SB) drifts from i.i.d.\ data observed on a single time interval. Starting from the conditional-ratio form of the Schrödinger bridge time-series...

We propose a generative framework for learning stochastic dynamics from endpoint and intermediate distributional observations. The method formulates generation as a McKean-Vlasov control problem in wh...

High-dimensional partial differential equations (PDEs) with unknown coefficients arise widely in scientific machine learning, including continuous-time reinforcement learning, yet solving them efficie...

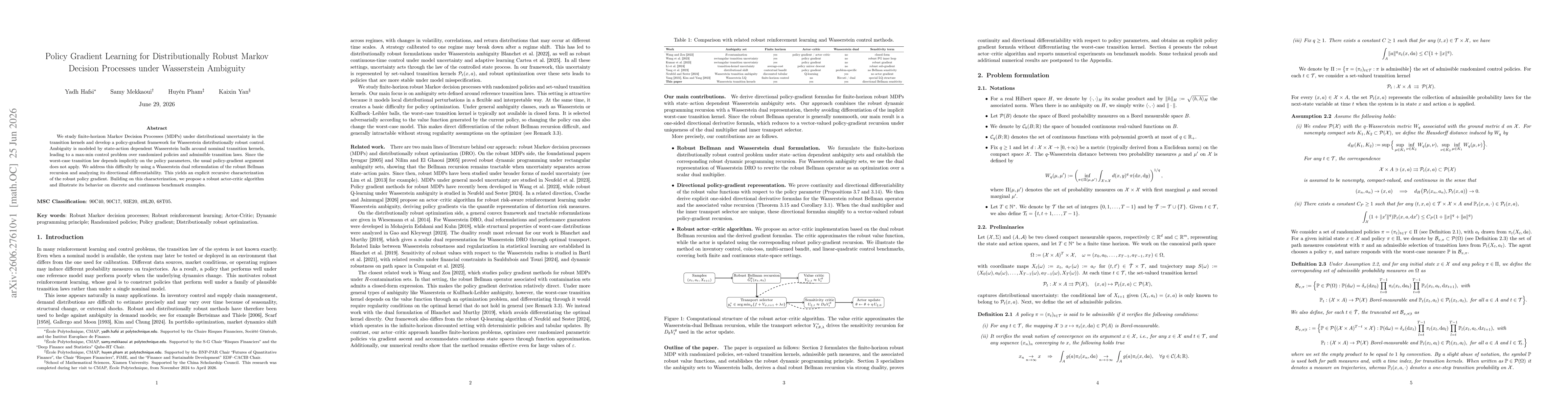

We study finite-horizon Markov Decision Processes (MDPs) under distributional uncertainty in the transition kernels and develop a policy-gradient framework for Wasserstein distributionally robust cont...