Academic Profile

Statistics

Similar Authors

Papers on arXiv

Diffusion-based generative models have emerged as powerful tools in the realm of generative modeling. Despite extensive research on denoising across various timesteps and noise levels, a conflict pers...

Self-supervised contrastive learning (CL) has achieved state-of-the-art performance in representation learning by minimizing the distance between positive pairs while maximizing that of negative ones....

In this study, we discuss a machine learning technique to price exotic options with two underlying assets based on a non-Gaussian Levy process model. We introduce a new multivariate Levy process mod...

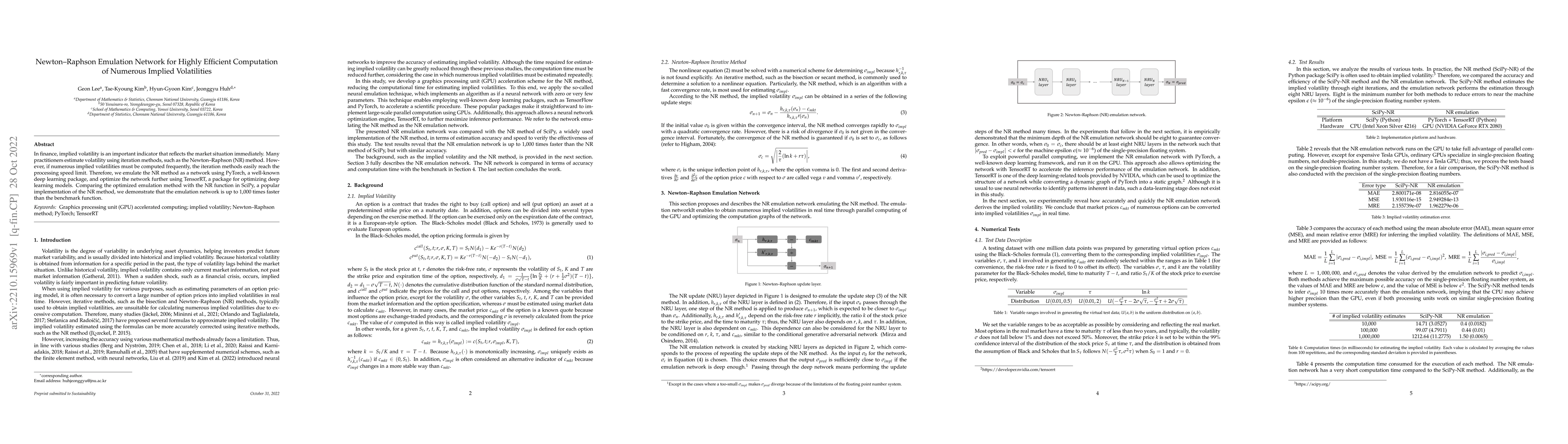

In finance, implied volatility is an important indicator that reflects the market situation immediately. Many practitioners estimate volatility using iteration methods, such as the Newton--Raphson (...

This paper presents the use of Kolmogorov-Arnold Networks (KANs) for forecasting the CBOE Volatility Index (VIX). Unlike traditional MLP-based neural networks that are often criticized for their black...

Probabilistic forecasting is crucial in multivariate financial time-series for constructing efficient portfolios that account for complex cross-sectional dependencies. In this paper, we propose Diffol...

This paper introduces MarketGAN, a factor-based generative framework for high-dimensional asset return generation under severe data scarcity. We embed an explicit asset-pricing factor structure as an ...