Academic Profile

Statistics

Similar Authors

Papers on arXiv

We prove a comparison result for viscosity solutions of second order parabolic partial differential equations in the Wasserstein space. The comparison is valid for semisolutions that are Lipschitz c...

We solve a generalized Kyle model type problem using Monge-Kantorovich duality and backward stochastic partial differential equations. First, we show that the the generalized Kyle model with dynam...

In this note, we provide a smooth variational principle on Wasserstein space by constructing a smooth gauge-type function using the sliced Wasserstein distance. This function is a crucial tool for o...

In this paper, we study a learning problem in which a forecaster only observes partial information. By properly rescaling the problem, we heuristically derive a limiting PDE on Wasserstein space whi...

We construct an equilibrium for the continuous time Kyle's model with stochastic liquidity, a general distribution of the fundamental price, and correlated stock and volatility dynamics. For distrib...

We study the continuous time Kyle-Back model with a risk averse informed trader.We show that in a market with multiple assets and non-Gaussian prices an equilibrium exists. The equilibrium is constr...

We study the problem of prediction with expert advice with adversarial corruption where the adversary can at most corrupt one expert. Using tools from viscosity theory, we characterize the long-time...

We show that the problem of existence of equilibrium in Kyle's continuous time insider trading model can be tackled by considering a forward-backward system coupled via an optimal transport type con...

We establish connections between optimal transport theory and the dynamic version of the Kyle model, including new characterizations of informed trading profits via conjugate duality and Monge-Kanto...

We explicitly solve the nonlinear PDE that is the continuous limit of dynamic programming of \emph{expert prediction problem} in finite horizon setting with $N=4$ experts. The \emph{expert predictio...

We study a continuous-time version of the intermediation model of Grossman and Miller (1988). To wit, we solve for the competitive equilibrium prices at which liquidity takers' demands are absorbed ...

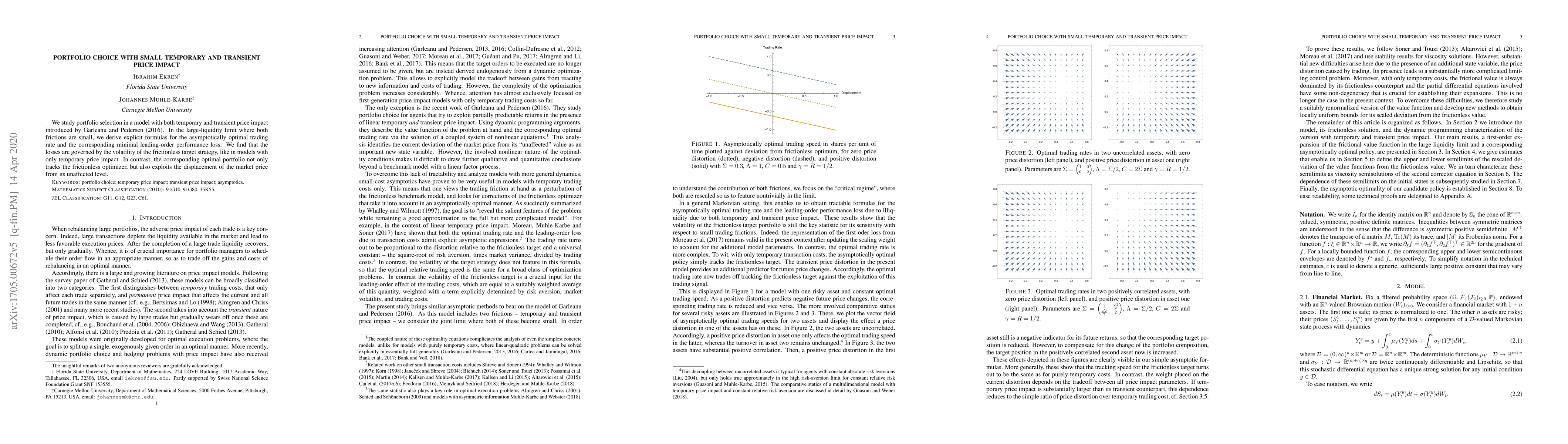

We study portfolio selection in a model with both temporary and transient price impact introduced by Garleanu and Pedersen (2016). In the large-liquidity limit where both frictions are small, we der...

Dynamic Stackelberg games are a broad class of two-player games in which the leader acts first, and the follower chooses a response strategy to the leader's strategy. Unfortunately, only stylized Stac...

In this paper we study a principal-agent problem in continuous time with multiple lump-sum payments (contracts) paid at different deterministic times. We reduce the non-zero sum Stackelberg game betwe...

In this paper, we consider a general partially observed diffusion model with periodic coefficients and with non-degenerate diffusion component. The coefficients of such a model depend on an unknown (s...

In this paper, we provide a convergence rate for particle approximations of a class of second-order PDEs on Wasserstein space. We show that, up to some error term, the infinite-dimensional inf(sup)-co...

In this paper, we show that the value functions of mean field control problems with common noise are the unique viscosity solutions to fully second-order Hamilton-Jacobi-Bellman equations, in a Cranda...

We investigate a Kyle model under Gaussian assumptions where a risk-averse informed trader has imperfect information on the fundamental price of an asset. We show that an equilibrium can be constructe...

We study the uniform-in-time weak propagation of chaos for the consensus-based optimization (CBO) method on a bounded searching domain. We apply the methodology for studying long-time behaviors of int...

In this paper, we prove a comparison result for semi-continuous viscosity solutions of a class of second-order PDEs in the Wasserstein space. This allows us to remove the Lipschitz continuity assumpti...

We study a principal-agent model involving a large population of heterogeneously interacting agents. By extending the existing methods, we find the optimal contracts assuming a continuum of agents, an...

We study a continuous time contracting model in which a principal hires a risk averse agent to manage a project over a finite horizon and provides sequential payments whose timing is endogenously dete...

We establish a comparison principle for viscosity solutions of a class of nonlinear partial differential equations posed on the space of nonnegative finite measures, thereby extending recent results f...

We study the large-population convergence of a consensus-based algorithm for the saddle point problem proposed by ArXiv: 2212.12334, establishing the uniform-in-time propagation of chaos using a coupl...

We study a principal-agent problem with adverse selection, where the principal does not know the agent's true cost but must design a contract to optimize a specific criterion. Unlike standard screenin...

We study causal optimal transport in continuous time, with Markovian cost, between a finite-state Markov source and a diffusion target. By replacing the source with its conditional law given the obser...

We prove a comparison principle for a class of second-order Hamilton--Jacobi--Bellman equations on the Wasserstein space whose second-order term is generated by a general common-noise Hessian. The mai...

We study a homogenization problem for first-order Hamilton-Jacobi equations in the Wasserstein space with a convex Hamiltonian. We show that the solution $U^\varepsilon$, which is the value function o...