Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider the problem of optimization of contributions of a financial planner such as a working individual towards a financial goal such as retirement. The objective of the planner is to find an o...

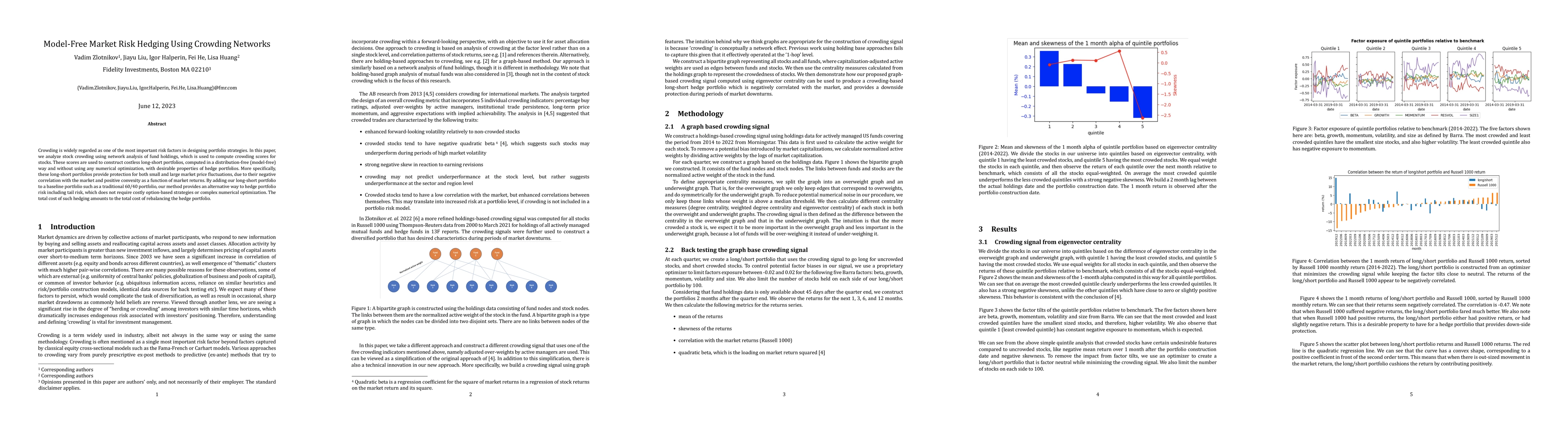

Crowding is widely regarded as one of the most important risk factors in designing portfolio strategies. In this paper, we analyze stock crowding using network analysis of fund holdings, which is us...

This paper presents an analytically tractable and practically-oriented model of non-linear dynamics of a multi-asset market in the limit of a large number of assets. The asset price dynamics are dri...

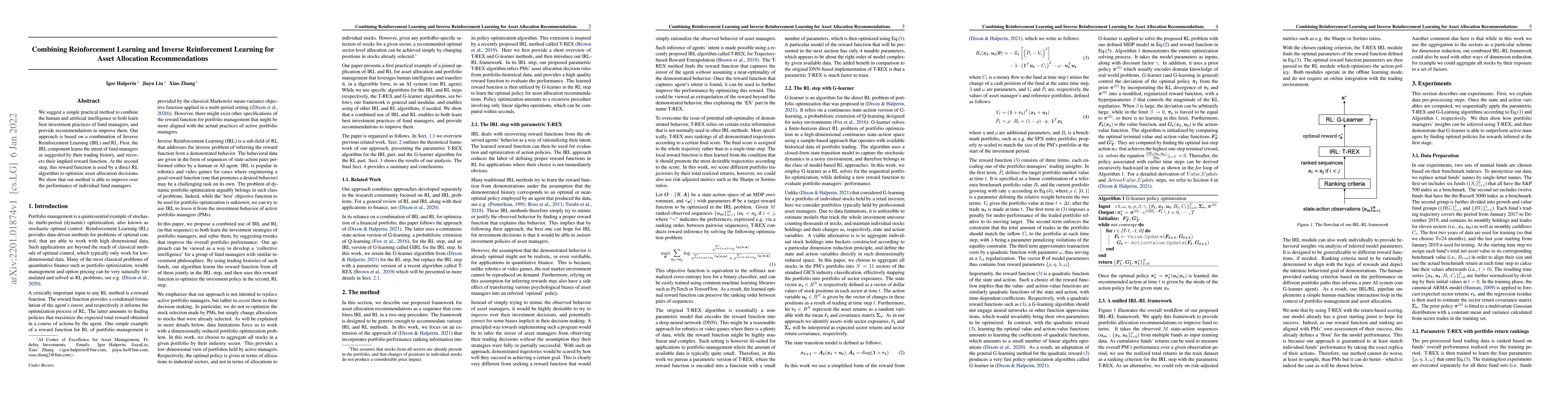

We suggest a simple practical method to combine the human and artificial intelligence to both learn best investment practices of fund managers, and provide recommendations to improve them. Our appro...

This paper addresses distributional offline continuous-time reinforcement learning (DOCTR-L) with stochastic policies for high-dimensional optimal control. A soft distributional version of the class...

This paper presents a tractable model of non-linear dynamics of market returns using a Langevin approach. Due to non-linearity of an interaction potential, the model admits regimes of both small and...

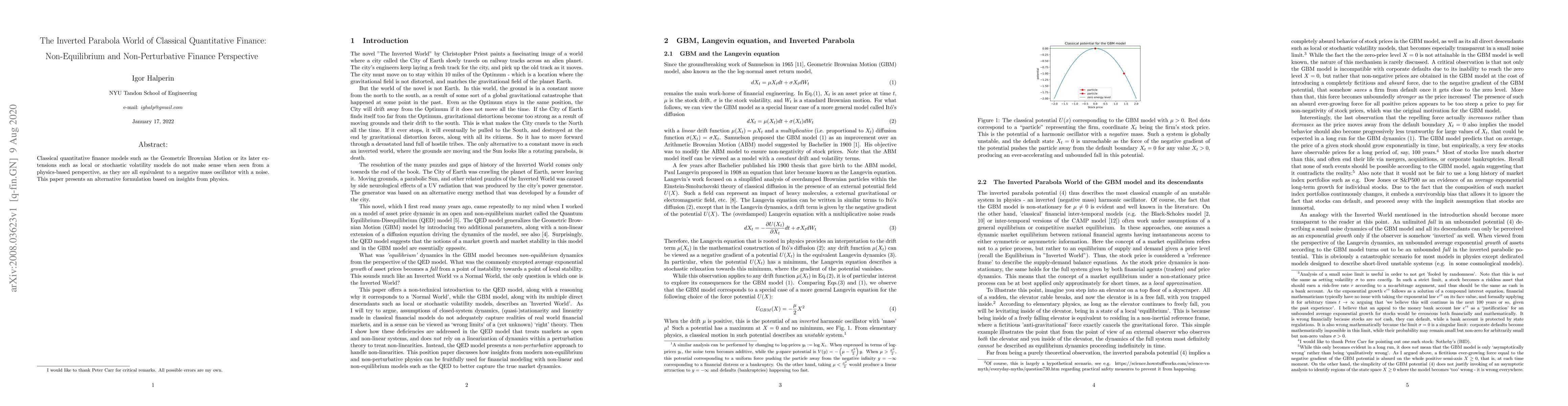

Classical quantitative finance models such as the Geometric Brownian Motion or its later extensions such as local or stochastic volatility models do not make sense when seen from a physics-based per...

We present a reinforcement learning approach to goal based wealth management problems such as optimization of retirement plans or target dated funds. In such problems, an investor seeks to achieve a...

This paper presents a discrete-time option pricing model that is rooted in Reinforcement Learning (RL), and more specifically in the famous Q-Learning method of RL. We construct a risk-adjusted Mark...

We present CAISSON, a novel hierarchical approach to Retrieval-Augmented Generation (RAG) that transforms traditional single-vector search into a multi-view clustering framework. At its core, CAISSON ...

The Marketron model, introduced by [Halperin, Itkin, 2025], describes price formation in inelastic markets as the nonlinear diffusion of a quasiparticle (the marketron) in a multidimensional space com...

The proliferation of Large Language Models (LLMs) is challenged by hallucinations, critical failure modes where models generate non-factual, nonsensical or unfaithful text. This paper introduces Seman...

This work builds upon the long-standing conjecture that linear diffusion models are inadequate for complex market dynamics. Specifically, it provides experimental validation for the author's prior arg...

Large Language Models (LLMs) are prone to critical failure modes, including \textit{intrinsic faithfulness hallucinations} (also known as confabulations), where a response deviates semantically from t...

Evaluating faithfulness of Large Language Models (LLMs) to a given task is a complex challenge. We propose two new unsupervised metrics for faithfulness evaluation using insights from information theo...

This work presents a reconstructed English edition of the seminal humor anthology \textbf{Physicists Joke} (\textbf{Fiziki Shutyat}), originally published in the USSR in 1966. While the Soviet edition...

We study Langevin dynamics of $N$ Brownian particles on compact two-dimensional Riemannian manifolds, interacting through pairwise potentials linear in geodesic distance with quenched random couplings...

We introduce the Frustrated Distance Matrix (FDM) model, a dynamic extension of the static distance-matrix ensemble on S^2 analyzed by Bogomolny, Bohigas, and Schmit (BBS). Its entries are pairwise ge...

We develop a statistical field theory that describes the large-N limit of a system of Brownian particles with quenched random pairwise interactions on a compact two-dimensional Riemannian manifold. Th...

Bogomolny, Bohigas and Schmit (BBS) found that the spectrum of the pairwise distance matrix on N points sampled from a smooth d-dimensional manifold encodes a signature of the underlying geometry. We ...

Observable Matrix Dynamics (OMD) is a diagnostic framework that probes the dynamics of high-dimensional internal representations of inputs by a neural network via a fixed-size $N \times N$ distance ma...