Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a novel multivariate GARCH model with flexible convolution-t distributions that is applicable in high-dimensional systems. The model is called Cluster GARCH because it can accommodate c...

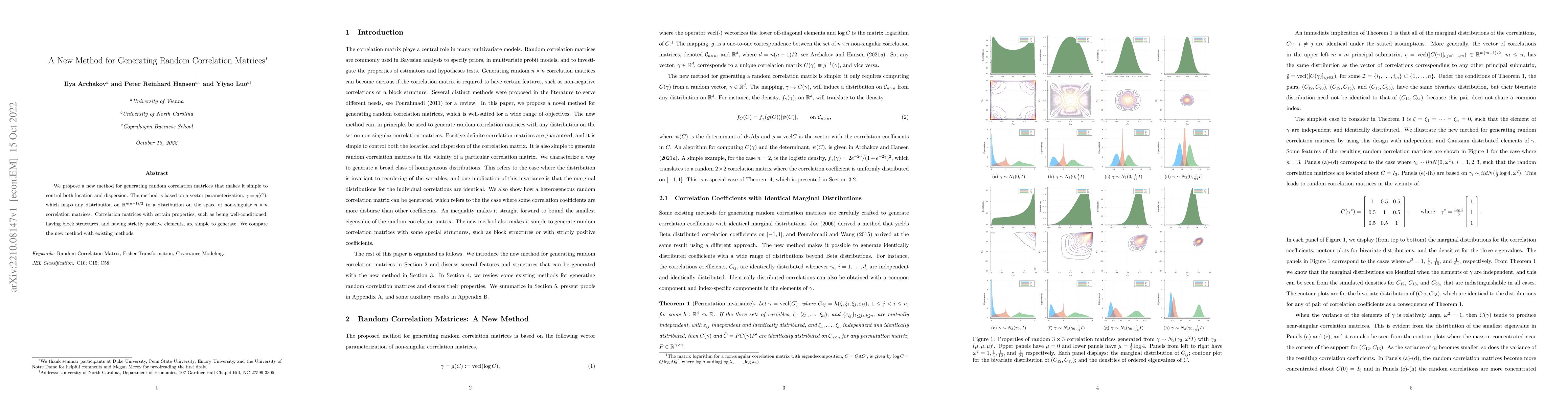

We propose a new method for generating random correlation matrices that makes it simple to control both location and dispersion. The method is based on a vector parameterization, gamma = g(C), which...

We propose a novel class of multivariate GARCH models that utilize realized measures of volatilities and correlations. The central component is an unconstrained vector parametrization of the conditi...

We obtain a canonical representation for block matrices. The representation facilitates simple computation of the determinant, the matrix inverse, and other powers of a block matrix, as well as the ...

We introduce a novel parametrization of the correlation matrix. The reparametrization facilitates modeling of correlation and covariance matrices by an unrestricted vector, where positive definitene...

We construct and analyze an estimator of association between random variables based on their similarity in both direction and magnitude. Under special conditions, the proposed measure becomes a robust...

We study the finite-sample behavior of the Generalized Fisher Transformation (GFT), the parametrization of a correlation matrix $C$ by $γ(C)=\operatorname{vecl}\log C$. The GFT coordinates extend Fish...