01

MethodologyHow they did it

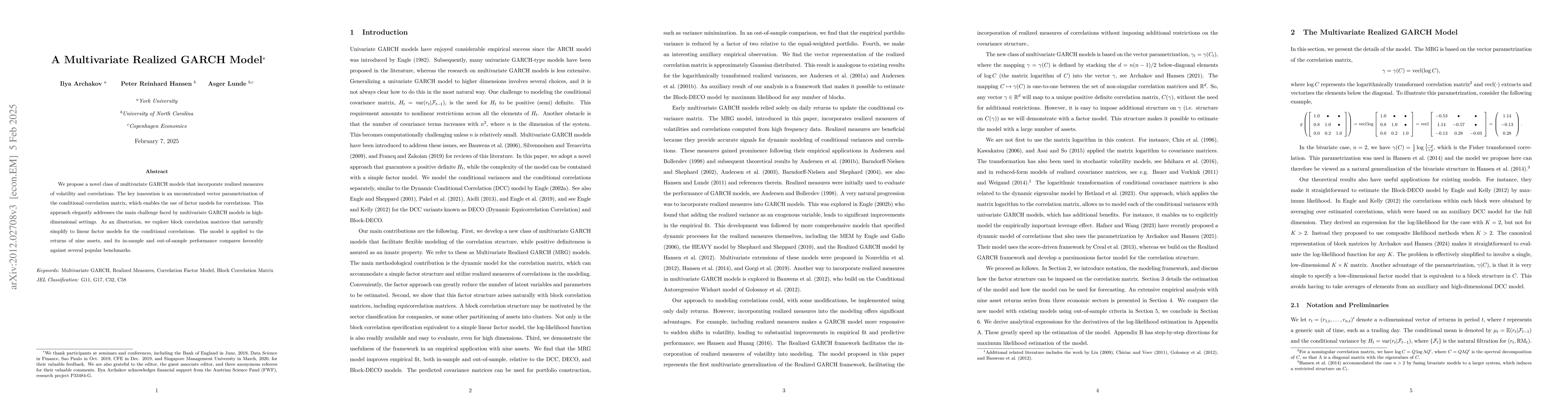

The paper introduces a novel multivariate GARCH model that utilizes realized measures of volatilities and correlations, offering an unconstrained vector parametrization of the conditional correlation matrix to facilitate factor models for correlations, addressing the primary challenge in high-dimensional settings.

Discussion 0