Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a novel multivariate GARCH model with flexible convolution-t distributions that is applicable in high-dimensional systems. The model is called Cluster GARCH because it can accommodate c...

We introduce a new class of multivariate heavy-tailed distributions that are convolutions of heterogeneous multivariate t-distributions. Unlike commonly used heavy-tailed distributions, the multivar...

Time-varying volatility is an inherent feature of most economic time-series, which causes standard correlation estimators to be inconsistent. The quadrant correlation estimator is consistent but ver...

The Clustered Factor (CF) model induces a block structure on the correlation matrix and is commonly used to parameterize correlation matrices. Our results reveal that the CF model imposes superfluou...

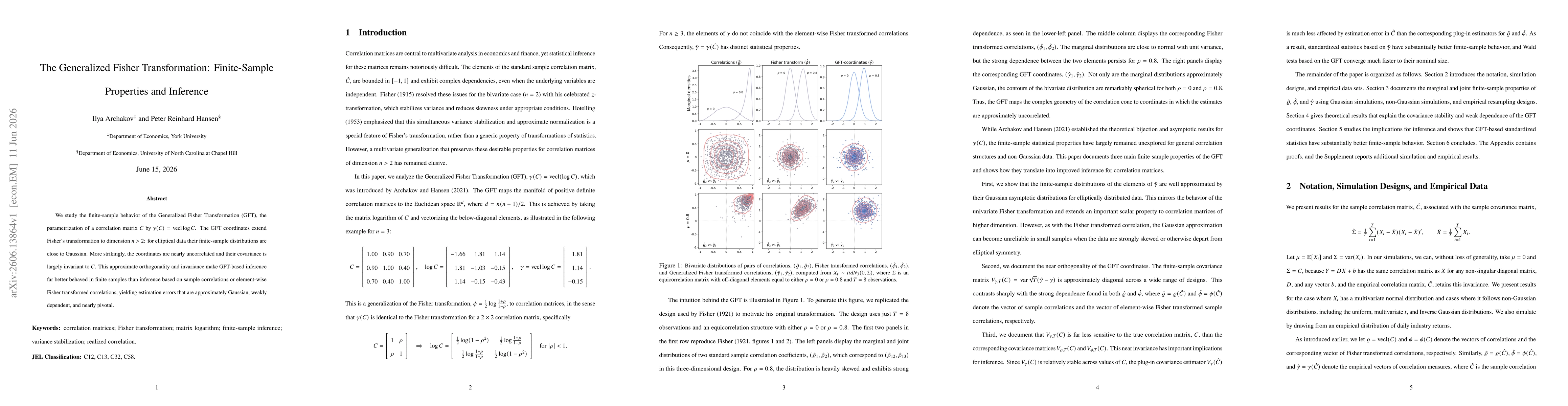

We propose a new method for generating random correlation matrices that makes it simple to control both location and dispersion. The method is based on a vector parameterization, gamma = g(C), which...

We introduce a novel pricing kernel with time-varying variance risk aversion that yields closed-form expressions for the VIX. We also obtain closed-form expressions for option prices with a novel ap...

We introduce a new volatility model for option pricing that combines Markov switching with the Realized GARCH framework. This leads to a novel pricing kernel with a state-dependent variance risk pre...

We show that the Realized GARCH model yields close-form expression for both the Volatility Index (VIX) and the volatility risk premium (VRP). The Realized GARCH model is driven by two shocks, a retu...

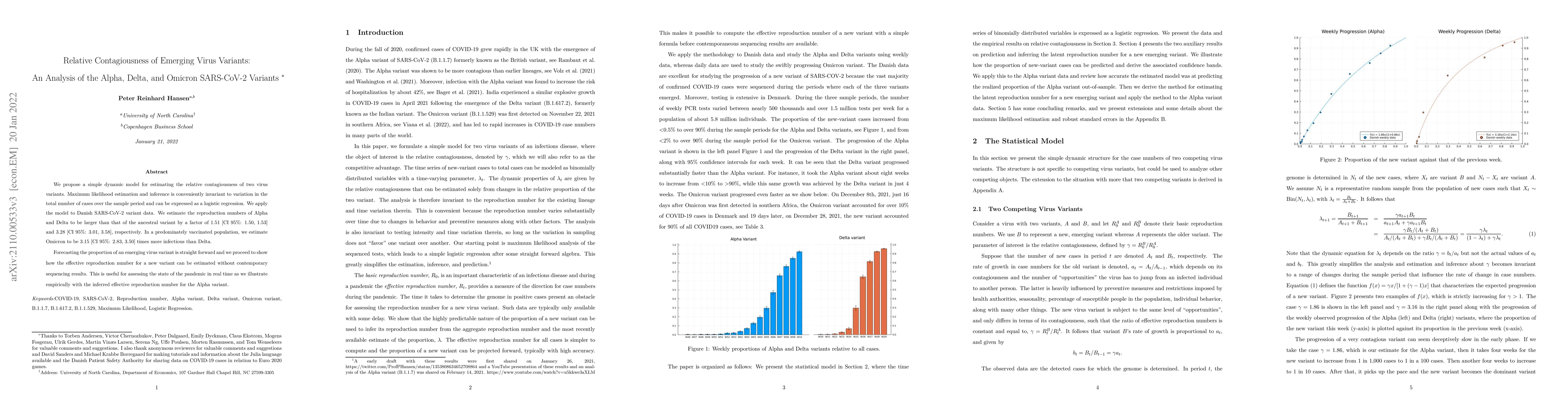

We propose a simple dynamic model for estimating the relative contagiousness of two virus variants. Maximum likelihood estimation and inference is conveniently invariant to variation in the total nu...

We study recurrent patterns in volatility and volume for major cryptocurrencies, Bitcoin and Ether, using data from two centralized exchanges (Coinbase Pro and Binance) and a decentralized exchange ...

We propose a novel class of multivariate GARCH models that utilize realized measures of volatilities and correlations. The central component is an unconstrained vector parametrization of the conditi...

We obtain a canonical representation for block matrices. The representation facilitates simple computation of the determinant, the matrix inverse, and other powers of a block matrix, as well as the ...

We introduce a novel parametrization of the correlation matrix. The reparametrization facilitates modeling of correlation and covariance matrices by an unrestricted vector, where positive definitene...

We introduce a novel method for obtaining a wide variety of moments of a random variable with a well-defined moment-generating function (MGF). We derive new expressions for fractional moments and frac...

We introduce a new dynamic factor correlation model with a novel variation-free parametrization of factor loadings. The model is applicable to high dimensions and can accommodate time-varying correlat...

We derive an integral expression $G(z)$ for the reciprocal gamma function, $1/\Gamma(z)=G(z)/\pi$, that is valid for all $z\in\mathbb{C}$, without the need for analytic continuation. The same integral...

We take a new perspective on identification in structural dynamic models: rather than imposing restrictions, we optimize an objective. This provides new theoretical insights into traditional Cholesky ...

We present a unified integral framework based on the Fourier-Laplace transform evaluated along a vertical line in the complex plane. By identifying the moment-generating function (MGF) of a random var...

The convolution of a Gaussian and a Cauchy distribution, known as the Voigt distribution, is widely used in spectroscopy and provides a natural framework for modeling heavy-tailed measurement noise. W...

Score-driven models update time-varying parameters using conditional likelihood scores. This paper gives a Bayesian interpretation based on Tweedie's formula. In Gaussian signal extraction, Tweedie's ...

We study the finite-sample behavior of the Generalized Fisher Transformation (GFT), the parametrization of a correlation matrix $C$ by $γ(C)=\operatorname{vecl}\log C$. The GFT coordinates extend Fish...

We propose the Split-Session Cluster GARCH model for heavy-tailed multivariate dependence among asset returns decomposed into overnight and intraday components. The model uses convolution-$t$ distribu...

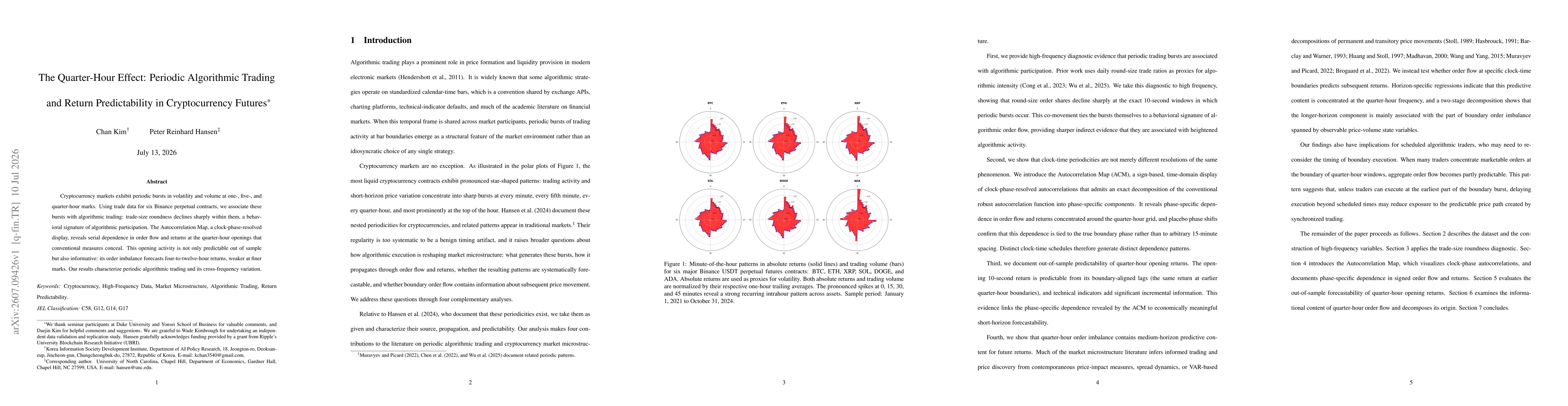

Cryptocurrency markets exhibit periodic bursts in volatility and volume at one-, five-, and quarter-hour marks. Using trade data for six Binance perpetual contracts, we associate these bursts with alg...