Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study the analytical properties of a one-side order book model in which the flows of limit and market orders are Poisson processes and the distribution of lifetimes of cancelled orders is exponen...

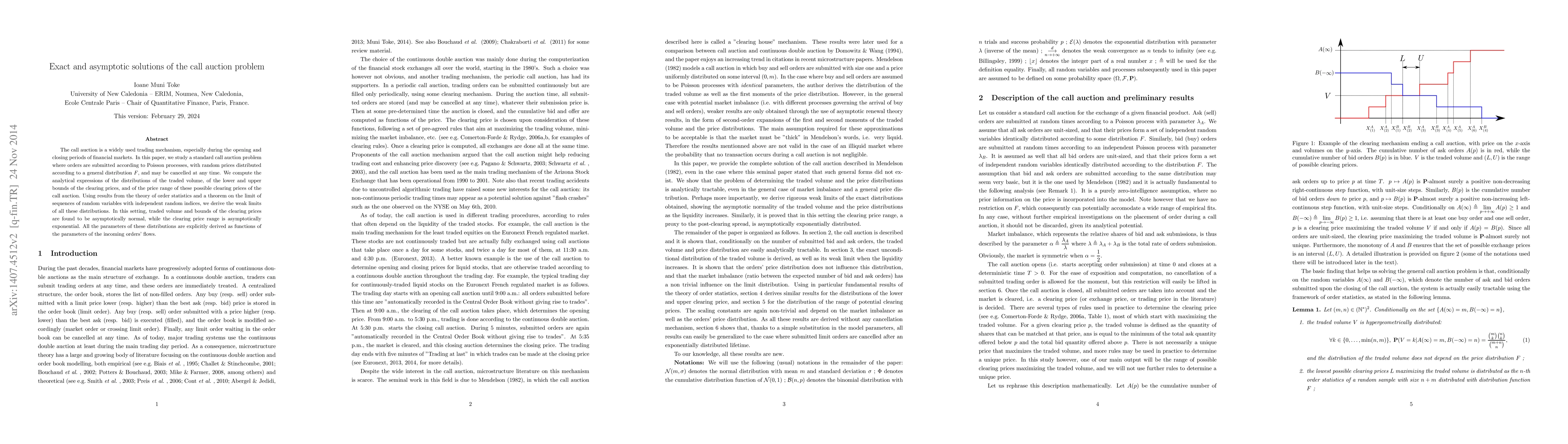

The call auction is a widely used trading mechanism, especially during the opening and closing periods of financial markets. In this paper, we study a standard call auction problem where orders are ...

In this paper, we develop a Markovian model that deals with the volume offered at the best quote of an electronic order book. The volume of the first limit is a stochastic process whose paths are pe...

We propose a parametric model for the simulation of limit order books. We assume that limit orders, market orders and cancellations are submitted according to point processes with state-dependent in...

In this work we investigate tick-by-tick data provided by the TRTH database for several stocks on three different exchanges (Paris - Euronext, London and Frankfurt - Deutsche B\"orse) and on a 5-yea...

We propose a novel approach to marked Hawkes kernel inference which we name the moment-based neural Hawkes estimation method. Hawkes processes are fully characterized by their first and second order...

Equity auctions display several distinctive characteristics in contrast to continuous trading. As the auction time approaches, the rate of events accelerates causing a substantial liquidity buildup ...

Using high-quality data, we report several statistical regularities of equity auctions in the Paris stock exchange. First, the average order book density is linear around the auction price at the ti...

A point process model for order flows in limit order books is proposed, in which the conditional intensity is the product of a Hawkes component and a state-dependent factor. In the LOB context, stat...

This paper extends the analysis of Muni Toke and Yoshida (2020) to the case of marked point processes. We consider multiple marked point processes with intensities defined by three multiplicative co...

Decentralized lending protocols within the decentralized finance ecosystem enable the lending and borrowing of crypto-assets without relying on traditional intermediaries. Interest rates in these prot...

This work focuses on a self-exciting point process defined by a Hawkes-like intensity and a switching mechanism based on a hidden Markov chain. Previous works in such a setting assume constant intensi...

We investigate applications of deep neural networks to a point process having an intensity with mixing covariates processes as input. Our generic model includes Cox-type models and marked point proces...

We study the optimal liquidation of a large position on Uniswap v2 and Uniswap v3 in discrete time. The instantaneous price impact is derived from the AMM pricing rule. Transient impact is modeled to ...